Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

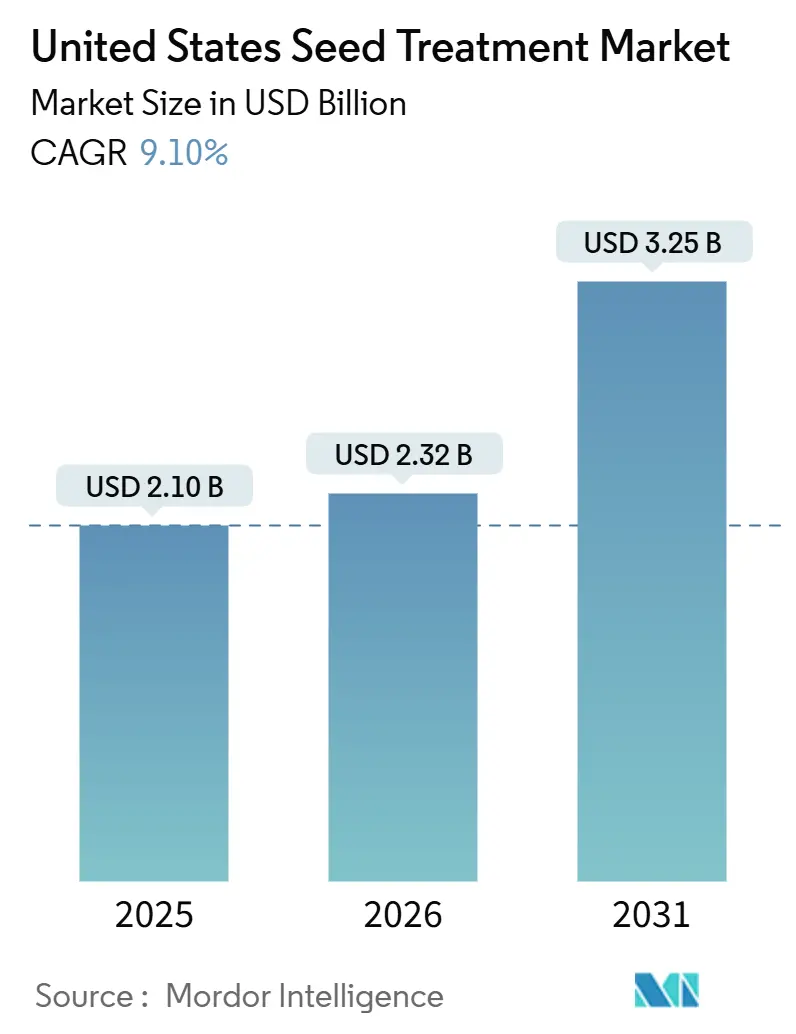

| Base Year Market Size (2025) | USD 2.10 Billion |

| Market Size (2025) | USD 2.32 Billion |

| Market Size (2030) | USD 3.25 Billion |

| Growth Rate (2026 - 2031) | 9.10% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Seed Treatment Market Analysis by Mordor Intelligence

The United States seed treatment market size was valued at USD 2.10 billion in 2025 and estimated to grow from USD 2.32 billion in 2026 to reach USD 3.25 billion by 2031, at a CAGR of 9.10% during the forecast period (2026-2031). Strengthening the Environmental Protection Agency's oversight of broadcast pesticides, expanding pathogen resistance, and rising demand for regenerative agriculture tools are prompting growers to shift crop protection budgets toward seed-applied solutions. Fungicides retained the leading revenue position, while Pythium and Rhizoctonia remained prevalent across the Corn Belt. Regulatory moves such as Vermont’s Act 182 and California’s neonicotinoid controls are nudging formulators toward non-neonic insecticides and microplastic-free coatings, and farm-level economics are accelerating investments in on-farm treating equipment that let growers bypass commodity discounts. Bayer AG, Syngenta AG, Corteva, Inc., BASF SE, UPL Limited. jointly hold a significant share of revenue, and mobile treater manufacturers are opening alternative routes to market.

Key Report Takeaways

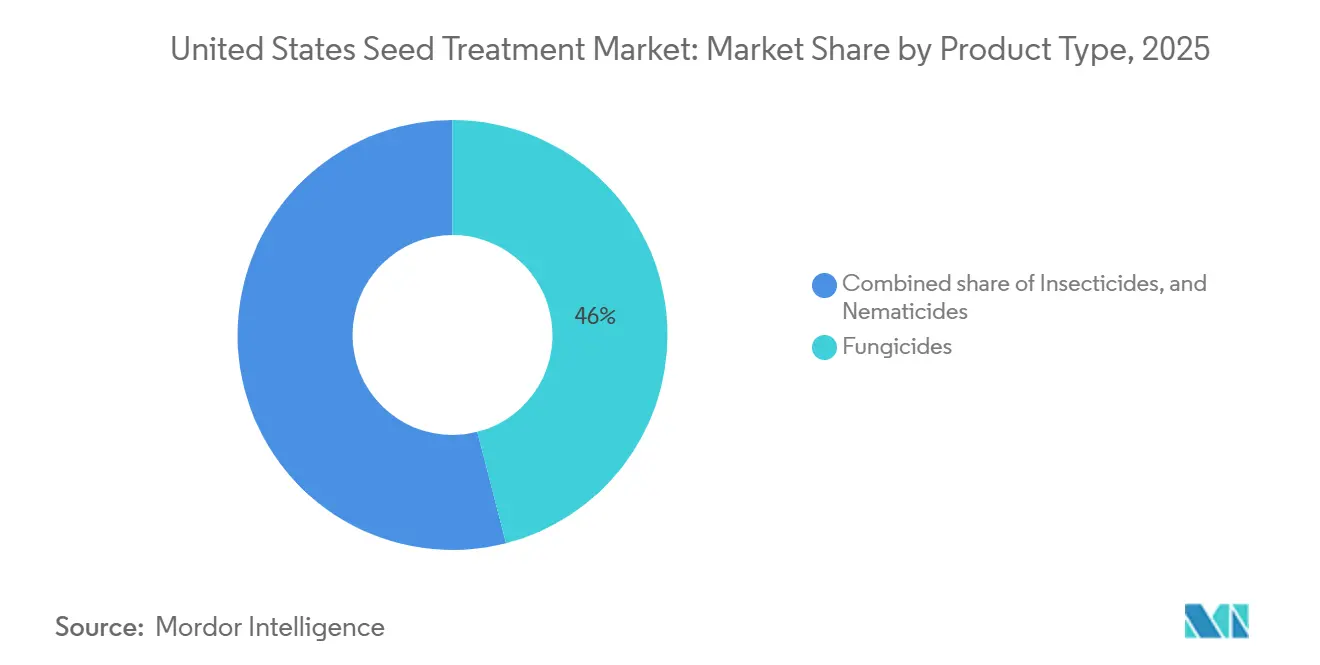

- By product type, fungicides hold the largest position, accounting for 46% of the United States seed treatment market size in 2025, while insecticides are the fastest-growing segment, projected to grow at a 13.5% CAGR through 2026-2031.

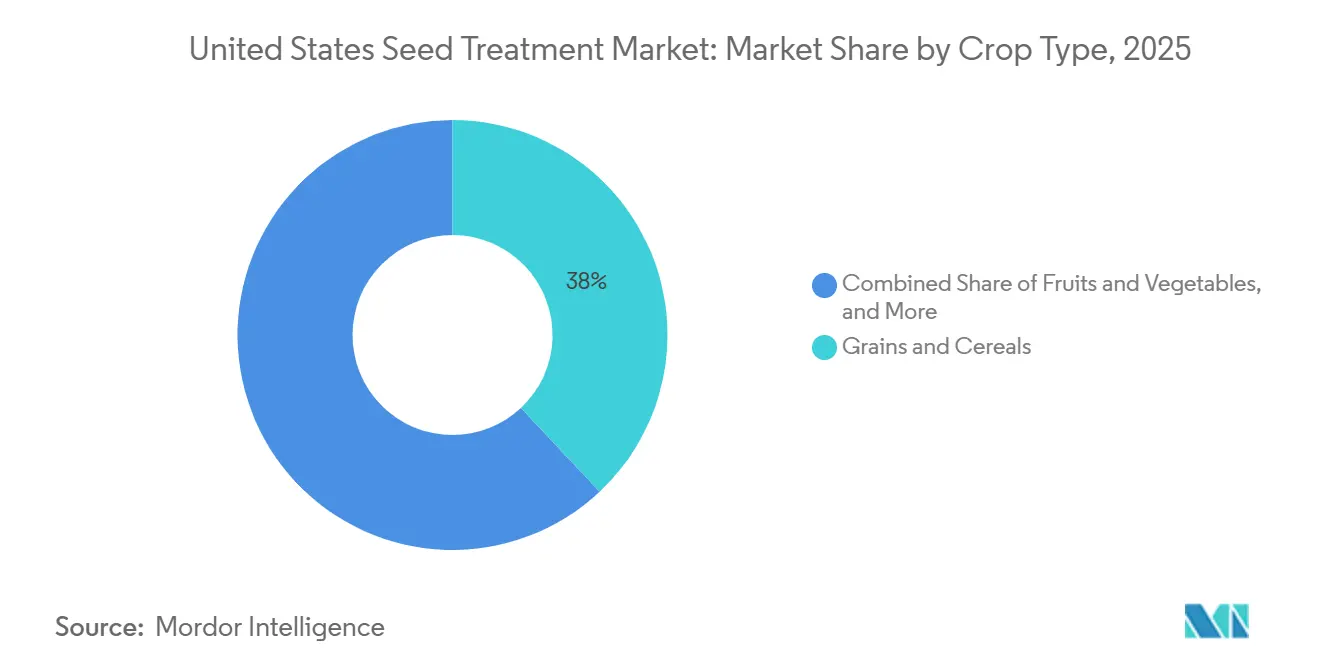

- By crop type, grains and cereals commanded the largest segment, 38% of the United States seed treatment market size in 2025, whereas oilseeds and pulses are the fastest-growing segment, forecast to grow at a 9.4% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Seed Treatment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory pressure on conventional pesticides | +1.8% | Corn Belt and Delta states | Medium term (2-4 years) |

| Urgency in resistance management to combat pests and diseases | +1.5% | No-till soybean and continuous corn zones | Long term (≥ 4 years) |

| Shift to polymer encapsulation for reduced dust-off | +1.2% | Early adoption in polymer encapsulation for reduced dust-off | Long term (≥ 4 years) |

| Carbon-credit monetization for treated cover crops | +0.6% | Midwest and Plains states | Medium term (2-4 years) |

| Increasing demand for on-farm seed treating to enhance crop yields | +0.9% | Mid-sized farms nationwide | Short term (≤ 2 years) |

| Adoption of digital prescription planting for precision agriculture | +1.1% | Precision-ag adopter regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Regulatory Pressure on Conventional Pesticides

The Environmental Protection Agency updated occupational exposure assessments for clothianidin, imidacloprid, and thiamethoxam in July 2024, intensifying compliance burdens for foliar neonicotinoids and steering growers toward seed-applied alternatives[1]Source: Environmental Protection Agency, “Neonicotinoid Pesticides,” EPA.gov. Anticipated 2025 label amendments are likely to mandate wider buffers and stricter personal protective equipment for broadcast sprays, reinforcing the perception that seed placement is the regulatory path of least resistance. Extended Endangered Species Act consultations have already lengthened herbicide approvals, signaling similar hurdles for new foliar insecticides. Seed formulators exploit a shorter re-registration window by reformulating existing actives into seed-specific packages, giving them a faster route to market. As a result, companies investing in dedicated seed formulation platforms capture both time-to-market advantage and stewardship goodwill with growers who prefer products that require fewer handler precautions.

Carbon-Credit Monetization for Treated Cover-Crop Seeds

Cover-crop adoption is subsidized through carbon markets that pay farmers for sequestering soil carbon, yet protocols rarely account for seed treatment inputs. The Natural Resources Conservation Service expanded dynamic soil property monitoring, paving the way for methodologies to quantify the biomass acceleration delivered by treated seed. Empirical studies linking treated cover-crop emergence to verified carbon gains are still absent, so revenue upside is hypothetical. Early adopters self-fund seed treatment to stabilize stands in narrow autumn planting windows, betting on future credibility. Once registries such as Verra publish seed-inclusive carbon rules, formulators can bundle treatments with project enrollment, but until then, the driver remains modest in scope.

Increasing Demand for On-Farm Seed Treating to Enhance Crop Yields

Demand for on-farm seed treating is a significant driver of the United States seed treatment market, as farmers increasingly seek flexibility, cost control, and field-level customization. Rather than relying solely on pre-treated commercial seeds, growers use on-farm equipment to apply fungicides and insecticides just before planting. This approach allows them to adjust treatment rates based on local soil conditions, pest pressures, and crop rotation strategies, reducing waste and improving efficiency. A Midwestern corn farmer dealing with variable soil moisture might apply fungicide seed treatments only to fields susceptible to damping-off disease, rather than treating all seeds uniformly. This targeted method not only reduces input costs but also supports sustainability goals by minimizing chemical overuse.

Adoption of Digital Prescription Planting for Precision Agriculture

Digital prescription planting is further driving market growth by integrating data-driven decision-making into seed treatment and planting processes. Precision agriculture tools, such as GPS mapping, soil data analytics, and variable rate technology, enable farmers to create “prescriptions” that determine how seeds and treatments are applied across different field zones. These prescriptions optimize plant population, hybrid selection, and seed treatment intensity based on yield potential and environmental conditions. For instance, a farmer using digital platforms like Climate FieldView might increase insecticide seed treatment rates in zones with a history of pest infestations while reducing them in low-risk areas. This precision approach not only enhances yield potential but also improves return on investment, making advanced seed treatment solutions more appealing and contributing to overall market growth.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Impact of large grower consolidation on the agricultural market | -0.8% | Great Plains and Delta | Short term (≤ 2 years) |

| Lag in Environmental Protection Agency (EPA) approvals for new actives | -0.7% | Nationwide | Long term (≥ 4 years) |

| Emerging state-level restrictions on neonics and their impact | -0.9% | Northeast corridor | Medium term (2-4 years) |

| Addressing the perception gap compared to fully organic farming systems | -0.4% | Organic-transition acres and specialty crop zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Emerging State-Level Restrictions on Neonics and Their Impact

Vermont’s Act 182 bans neonic-treated soybean and cereal seed from January 2029, and similar proposals are pending in the New York and Connecticut legislatures[2]Source: Vermont General Assembly, “Act 182,” Vermont.gov. Suppliers answer with actives such as Syngenta’s PLINAZOLIN, first commercialized in Canadian cereals, and Corteva’s LumiGEN recipes that rely on non-neonic insecticides. Portfolio fragmentation complicates logistics but creates an opening for agile formulators that secure early registrations of alternative chemistries. The market implications of state-level neonicotinoid (neonics) restrictions suggest a fragmented United States seed treatment market divided into regulatory zones. This will require formulators to manage multiple product portfolios, complicating supply chain logistics. It also presents opportunities for companies that invest early in non-neonic alternatives and secure regulatory approvals ahead of competitors.

Addressing the Perception Gap Compared to Fully Organic Farming Systems

The National Organic Program permits treated seed only when organic seed is unavailable, and the National Organic Standards Board is debating tighter residue-testing requirements. Organic growers worry that even biological treatments may jeopardize certification. Suppliers attempting to penetrate this segment need fully certified production lines and must document value beyond compliance. They must address growers' concerns regarding the long-term viability of organic-certified inputs. Until yield gains are replicated, organic skepticism will cap demand.

Segment Analysis

By Product Type: Insecticides Momentum Builds Amid Fungicide Dominance

Fungicides hold the largest position, accounting for 46% of the United States seed treatment market share in 2025, helping growers combat Fusarium, Pythium, and Rhizoctonia. This dominance is attributed to their essential role in protecting seeds and seedlings from soil-borne and early-season diseases such as damping-off, root rot, and seed decay. Their widespread use ensures strong crop establishment and uniform germination, particularly in crops like corn, soybeans, and wheat. Soybean growers frequently use fungicide seed treatments to protect against pathogens such as Pythium and Rhizoctonia, which can significantly reduce stand counts if left unmanaged. This consistent and preventive protection has made fungicides a critical input for farmers across various growing regions.

Insecticides are the fastest-growing segment, projected to grow at a 13.5% CAGR through 2026-2031, whose growth is driven by increasing pest pressures, concerns over resistance, and the need for early-stage crop protection. Pests such as wireworms, seedcorn maggots, and aphids continue to threaten yields, prompting farmers to adopt insecticide seed treatments as a proactive measure. The adoption of integrated pest management and precision agriculture practices is promoting the targeted use of insecticides based on field-specific risks. Corn farmers in areas prone to early-season pest infestations may choose insecticide-treated seeds to prevent stand loss and avoid replanting costs, thereby fueling the rapid expansion of this segment.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Crop Type: Oilseeds Accelerate as Grains Hold Volume

Grains and cereals commanded the largest segment, 38% of the United States seed treatment market size in 2025, primarily due to their extensive cultivation area and the critical need to protect high-volume staple crops such as corn, wheat, and rice. Seed treatments are widely used in this segment to mitigate early-stage diseases and pests, ensuring uniform germination and robust crop establishment, both of which are vital for maximizing yields. Corn growers, in particular, often use fungicide and insecticide seed treatments to combat soil-borne pathogens and pests such as wireworms, reducing the risk of replanting and enhancing overall productivity. The consistent, large-scale demand for these crops continues to solidify this segment's dominance.

Oilseeds and pulses are the fastest-growing segment, forecast to grow at a 9.4% CAGR through 2026-2031, driven by rising demand for plant-based proteins and edible oils, as well as sustainable crop rotations. Farmers are increasingly incorporating soybeans, canola, and lentils into their rotations, thereby increasing demand for specialized seed treatments for these crops. Furthermore, chemical seed treatments and inoculants are gaining popularity in this segment to improve nitrogen fixation and soil health. According to the United States Department of Agriculture, corn acreage is projected to decline from 92.0 million acres in 2025 to 88.5 million acres by 2034, while soybean acreage is projected to rise from 85.0 million acres to 86.5 million acres[3]Source: United States Department of Agriculture, “USDA Agricultural Projections to 2034,” USDA.gov. This shift suggests that oilseeds and pulses will likely represent a growing share of the total treated seed volume as growers move away from continuous corn cultivation to address pest and disease management challenges.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Midwestern states form the heartland of treated seed demand because they plant more than 100 million combined acres of corn and soybeans. Fusarium and soybean cyst nematode prevalence keeps multi-mode fungicide and nematicide stacks indispensable. Internal Syngenta trials across Iowa, Illinois, and Indiana confirmed Victrato raised soybean yields by 3 bushels where nematode populations were moderate to high.

Delta growers, especially in Arkansas and Mississippi, battle reniform nematode and sudden death syndrome. In 2024, products like Victrato outperformed legacy treatments by 7.9 bushels in red crown rot plots in Illinois and Kentucky, demonstrating that disease complexes are migrating north. The Great Plains experience acreage diversification as wheat and sorghum rotations integrate pulses and soybeans, encouraging experimentation with set treatments.

The Northeast corridor witnesses regulatory divergence following Vermont’s Act 182. Formulators targeting this sub-region must craft non-neonic insecticide portfolios and adjust supply chains. California’s specialty crop sector continues to absorb seed treatment technology for vegetables and fruits, albeit under stringent state pesticide laws that, for now, exempt seed coatings. The growing consolidation of retailers across regions is impacting distribution strategies and promoting the adoption of integrated seed-plus-trait packages. Additionally, digital agronomy platforms are influencing adoption trends by offering localized insights on disease pressure and validating the return on investment for advanced seed treatments.

Competitive Landscape

Market concentration remains high, with the top five companies, including Bayer AG, Syngenta AG, Corteva, Inc., BASF SE, and UPL Limited, holding a significant share of global revenue. Competitive intensity is increasing as pesticide specialists and on-farm equipment vendors challenge incumbents by offering customized formulations and direct-to-grower sales models that bypass traditional seed-company markups. Opportunities are emerging in areas such as microplastic-free polymer coatings, non-neonicotinoid insecticides, and variable-rate seed treatment prescriptions linked to digital planting platforms.

Strategically, incumbents must defend their market share by acquiring pesticide companies, developing microplastic-free formulations, and enhancing digital delivery platforms. Meanwhile, disruptors can capture niche segments by offering specialized products and services that address unmet needs, transition acres, carbon credit-enrolled fields, and regions adopting precision agriculture. Technology is being leveraged to gain market share through digital prescription planning, which integrates soil maps and yield data to create variable-rate seed treatment prescriptions. This includes on-farm treating equipment with electronic controls and remote monitoring, as well as innovations in formulations.

Regulatory expertise is a key differentiator for market leaders. Microbial production facilities must meet dual compliance standards from the Environmental Protection Agency (EPA) and the Food and Drug Administration (FDA), a challenge that many start-ups address by partnering with established players. In emerging markets, domestic firms benefit from faster local approvals and cost advantages, prompting global companies to localize production or acquire regional competitors. Vertical integration into polymer manufacturing helps mitigate supply risks and capture additional margins as advanced coatings gain wider adoption in the seed treatment market.

United States Seed Treatment Industry Leaders

Bayer AG

Syngenta AG

BASF SE

UPL Limited

Corteva, Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Syngenta AG introduced its latest Seedcare innovation, Victrato seed treatment, which has been registered by the United States Environmental Protection Agency for use on soybeans and cotton. This treatment provides robust protection against plant-parasitic nematodes and diseases in a single molecule.

- September 2024: Corteva, Inc. introduced Lumiante fungicide seed treatment in the United States. This product targets Phytophthora and Pythium, two early-season soybean diseases that reduce yield potential, offering soybean growers an additional tool to combat these fungal diseases.

United States Seed Treatment Market Report Scope

Seed treatment is the process of treating seeds with chemical methods before planting. It is an eco-friendly approach that uses a small amount of insecticides and fungicides. Conventional agrochemicals have been widely used in seed treatment for many years to protect seeds against various stresses in the seedbed. The United States Seed Treatment Market Report is Segmented by Product Type (Fungicide, Insecticide, and Nematicide), by Crop Type (Commercial Crops, Fruits and Vegetables, Grains and Cereals, Pulses and Oilseeds, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Insecticides |

| Fungicides |

| Nematicides |

| Combination Products |

By Crop Type

| Grains and Cereals |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Commercial Crops |

| Turf and Ornamentals |

| By Product Type | Insecticides |

| Fungicides | |

| Nematicides | |

| Combination Products | |

| By Crop Type | Grains and Cereals |

| Oilseeds and Pulses | |

| Fruits and Vegetables | |

| Commercial Crops | |

| Turf and Ornamentals |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the United States seed treatment market in 2031?

United States seed treatment market is forecast to reach USD 3.25 billion by 2031.

Which product type currently leads sales?

Fungicides held the largest share at 46% in 2025.

How will Vermont's Act 182 affect insecticide formulations?

The 2029 ban on neonic-treated soybean and cereal seed pushes suppliers to develop non-neonic insecticide alternatives.

What advantage does on-farm seed treating provide?

It lets growers avoid commodity discounts on pre-treated seed, saving per-acre costs and enabling variable-rate prescriptions.