Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

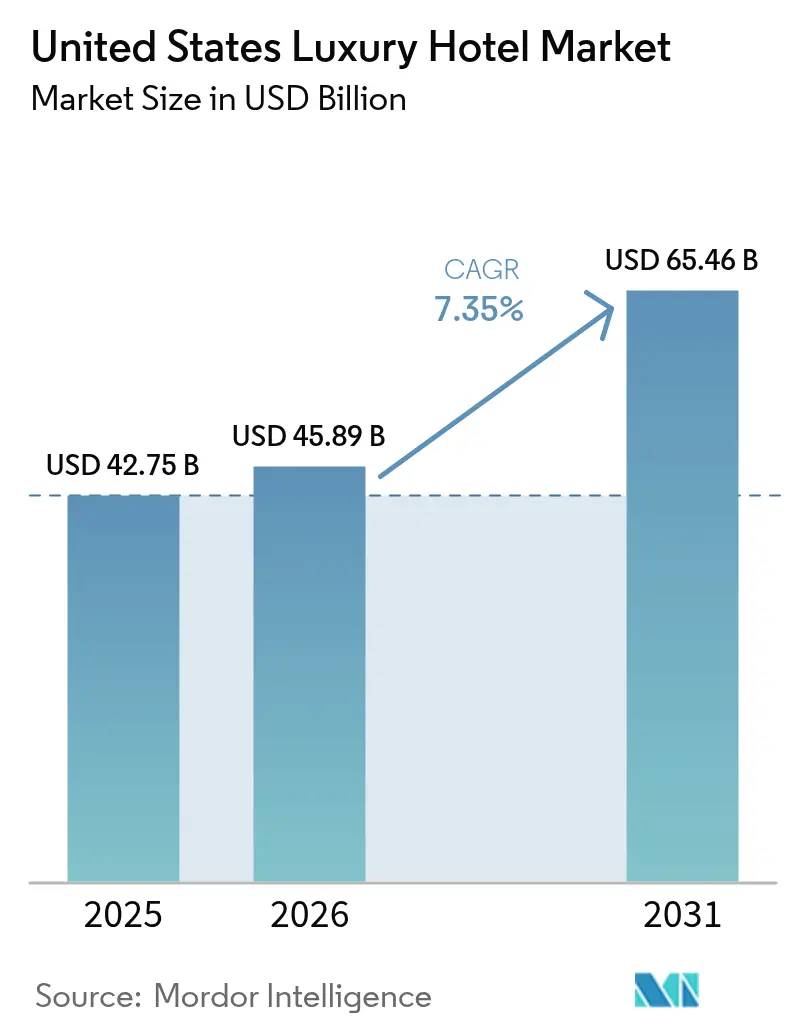

| Base Year Market Size (2025) | USD 42.75 Billion |

| Market Size (2026) | USD 45.89 Billion |

| Market Size (2031) | USD 65.46 Billion |

| Growth Rate (2026 - 2031) | 7.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Luxury Hotel Market Analysis by Mordor Intelligence

The United States luxury hotel market size was USD 45.89 billion in 2026, up from USD 42.75 billion in 2025, and it is projected to reach USD 65.46 billion by 2031 at a 7.35% CAGR. This growth pace surpassed the broader United States hotel sector, where RevPAR growth across all categories averaged 0.5% in 2025[1]• Source: IDeaS Revenue Solutions, “Revenue Reactions: U.S. Hotel Occupancy and RevPAR Declined in 2025,” ideas.com. Share gains from direct digital bookings, asset-light expansion strategies, and brand-led mixed-use projects have improved yield resilience across cycles within the United States luxury hotel market. Corporate travelers blending business and leisure have extended average stays and lifted ancillary revenue, supporting premium pricing within the United States luxury hotel market. Regionally, the South led in 2025, while the West is the fastest-growing region into 2031, a pattern that informs brand development and capital allocation in the United States luxury hotel market.

Key Report Takeaways

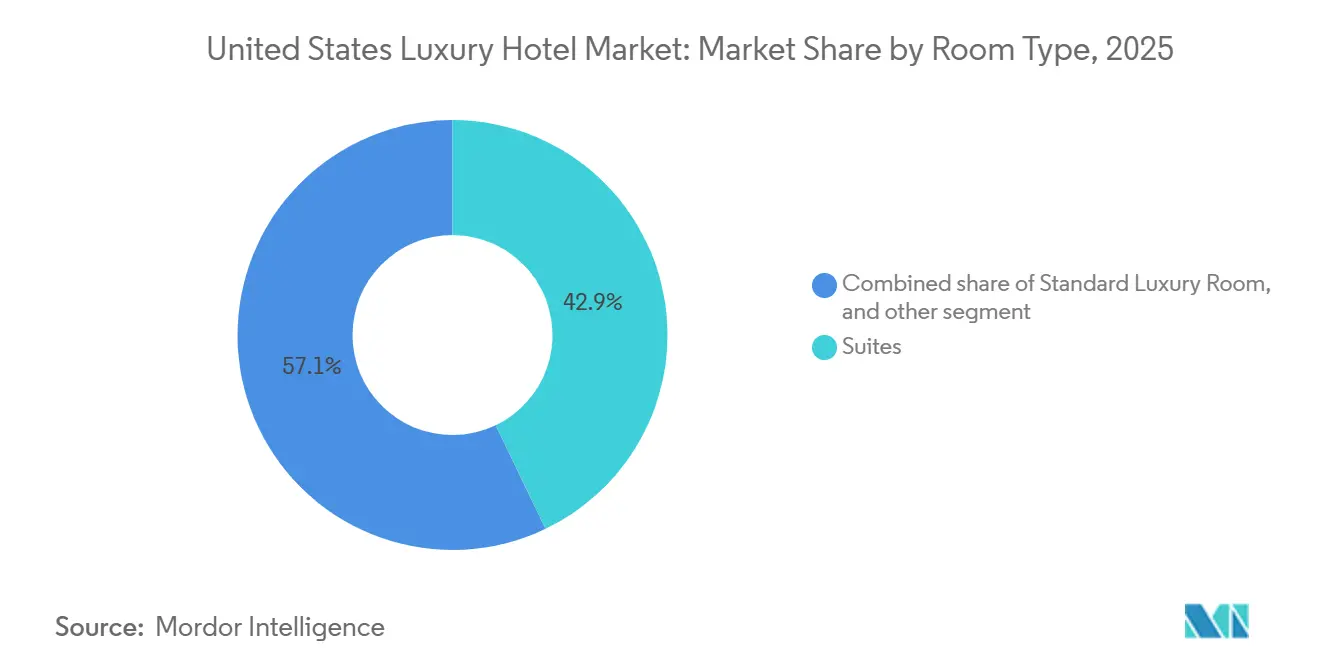

- By room type, suites captured 42.88% of United States luxury hotel market share in 2025; villas and bungalows are projected to expand at a 7.42% CAGR through 2031.

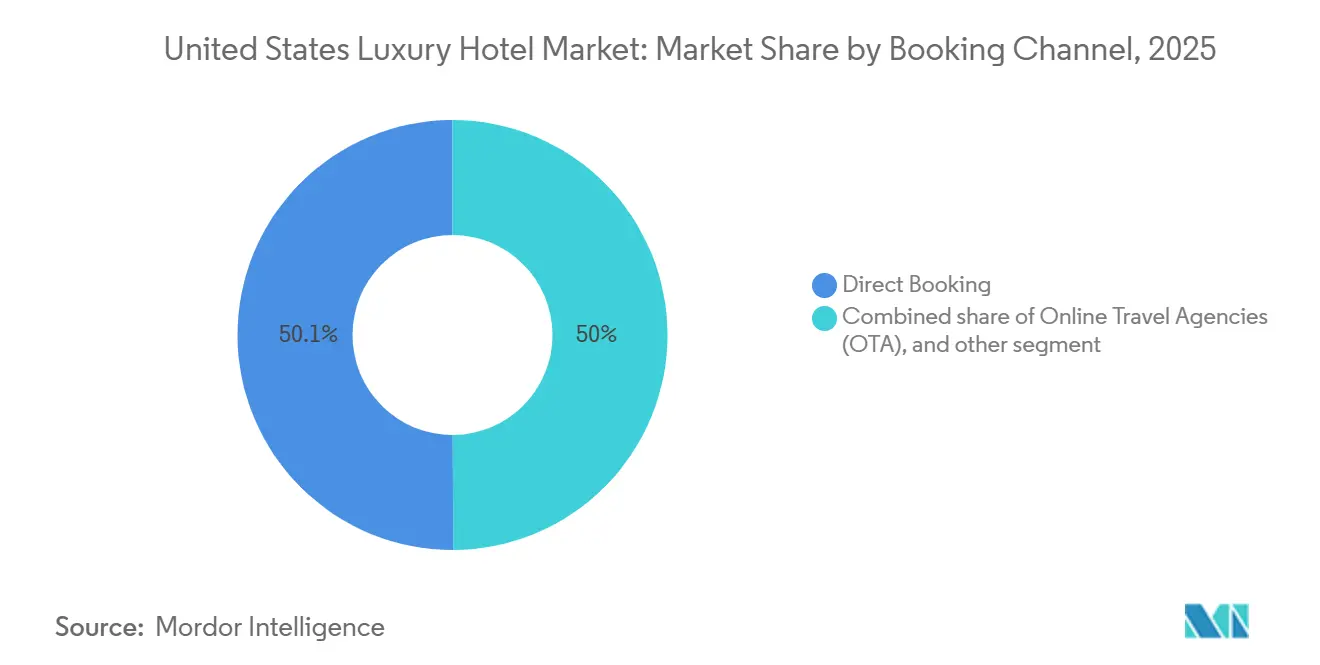

- By booking channel, direct booking accounted for 50.05% of the United States luxury hotel market size in 2025 and are advancing at a 10.14% CAGR to 2031.

- By service type, resorts held 35.66% of United States luxury hotel market share in 2025; suite hotels represent the fastest-growing service category with an 8.10% CAGR to 2031.

- By geography, the South commanded 31.55% of United States luxury hotel market share in 2025; the West is forecast to grow at a 7.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Luxury Hotel Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Experiential luxury demand surges, driven by rising wealth among UHNW individuals and millennials | +1.8% | Global, with concentration in major US gateway cities and resort destinations | Medium term (2-4 years) |

| Inbound travel to US gateway cities rebounds, supported by eased visa restrictions | +0.9% | National, with early gains in New York, Los Angeles, Miami | Short term (≤ 2 years) |

| Corporate "bleisure" policies lead to an uptick in long-stay luxury room bookings | +1.5% | National, particularly strong in urban and resort hybrid markets | Medium term (2-4 years) |

| Direct digital bookings reduce distribution costs | +1.2% | National, strongest among tech-forward brands | Long term (≥ 4 years) |

| Mixed-use hotel-residence projects contribute to the stabilization of RevPAR | +1.0% | Asia-Pacific core, spill-over to coastal US metros | Long term (≥ 4 years) |

| LEED-certified assets buoyed by ESG incentives enjoy higher ADR premiums | +0.9% | National, with accelerated adoption in California, New York | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Experiential luxury demand surges, driven by rising wealth among UHNW individuals and millennials

Affluent travelers in 2026 continue to prioritize high-quality experiences that combine wellness, privacy, and personalization, which sustains premium pricing across the United States luxury hotel market. Brand portfolios that curate bespoke wellness and culinary programs have seen a stronger rate integrity because high-spend guests value distinct experiences over standardized services within the United States luxury hotel market. Younger affluent cohorts define luxury around comfort, design, and access to wellness rather than legacy status, which is reshaping product mix and amenity design for new-builds and renovations in the United States luxury hotel market. Operators that combine discrete service with privacy-forward room categories secure longer stays and steadier repeat visitation from these guests. Portfolio expansion focused on conversions and signings adds supply that targets this preference shift while keeping capital intensity in check across the United States luxury hotel market.

Corporate "bleisure" policies lead to an uptick in long-stay luxury room bookings

Bleisure adoption has become a structural driver, with 62% of United States business travelers blending leisure in 2024 and 42% adding personal days, which lengthens stay patterns and boosts ancillary revenue for luxury properties positioned to serve both needs. Hotels report a high propensity for guests to extend at the same property during bleisure trips, and a large share of these travelers used the same hotel for added nights in 2025, reinforcing loyalty and direct engagement. Extended-stay performance has remained healthier than broader categories, supported by corporate accounts and longer booking windows through late 2024, which favors upscale suite products. The result is steadier weekday occupancy, two extra nights per trip on average in many corporate use cases, and stronger spend across dining, spa, and on-property experiences at higher-tier hotels. These dynamics give the United States luxury hotel market better demand visibility, which supports revenue management discipline and ADR consistency across the calendar.

Direct digital bookings reduce distribution costs

Direct digital bookings reached 50.05% of reservations in 2025 for luxury hotels and are advancing at a 10.14% CAGR toward 2031, reflecting brand investment in first-party channels that protect margin and deepen guest relationships within the United States luxury hotel market. OTA commissions in the 15% to 25% range make indirect business costlier than direct, and independent studies show direct bookings generate materially higher net revenue per stay for hotels when payment fees are the only deduction[2]• Source: Bowo, “OTAs vs Direct Bookings: How to Take Back Control of Your Hotel Sales,” bowo.fr. Hotel websites produced the highest average booking value at USD 516 in 2025, compared with USD 312 via OTAs, which further encourages brands to scale owned channels in the United States luxury hotel market[3]• Source: SiteMinder, “SiteMinder's Hotel Booking Trends,” siteminder.com. Trade associations project direct digital channels to outpace OTAs by the end of the decade, aided by loyalty programs, best-rate guarantees, and closed-user-group offers that maintain rate parity compliance while lifting conversion. AI chatbots and targeted email remarketing now support 24/7 pre-stay engagement and on-site upsell prompts, which increases guest lifetime value and reduce reliance on intermediaries across the United States luxury hotel market.

Mixed-use hotel-residence projects contribute to the stabilization of RevPAR

Mixed-use models that combine luxury hotels with branded residences and private clubs diversify revenue and smooth volatility in the United States luxury hotel market. Leading brands increased their residential pipelines in 2025 and 2026, adding signings and openings that blend resort-grade amenities with for-sale units and long-stay formats that keep service intensity aligned to demand. Four Seasons operates more than 50 residential properties and is advancing a substantial project pipeline, which reinforces fee-based income while strengthening brand engagement beyond transient stays within the United States luxury hotel market[4]• Source: Four Seasons, “New Openings,” fourseasons.com. These configurations also enable shared back-of-house and amenity investments that enhance guest experience without proportionate cost increases, improving property-level margins. As asset-light growth accelerates, conversions and signings help brands align formats to location demand, which stabilizes RevPAR performance across cycles in the United States luxury hotel market.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-luxury vacation rentals and branded residences intensify competition | -1.1% | National, spill-over to coastal and mountain resort markets | Medium term (2-4 years) |

| Payroll costs surge due to ongoing labor shortages | -1.3% | National, with acute pressure in major metropolitan areas | Short term (≤ 2 years) |

| Climate-driven weather events push insurance premiums higher | -0.8% | National, particularly impacting coastal projects | Long term (≥ 4 years) |

| Domestic travelers feel rate fatigue, grappling with inflation pressures | -0.7% | National, especially in secondary markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ultra-luxury vacation rentals and branded residences intensify competition

Private villas and branded residences offer privacy, space, and dedicated service that appeal to affluent travelers who value seclusion and bespoke experiences, which increases substitution risk at the high end of the United States luxury hotel market. Hotels face intensified competition in coastal and mountain destinations where larger accommodations and private access are viewed as core benefits. Platforms and professional managers support concierge-level service and curated experiences, which narrows service differentiation versus top-tier hotels in these locations. Luxury hotel operators respond by strengthening suite and villa inventory, deepening loyalty benefits, and emphasizing integrated wellness, culinary range, and on-property activities. Brands with owned distribution and high recognition maintain an advantage in trust and standards, but sustained product and service innovation is required to keep pace in the United States luxury hotel market.

Payroll costs surge due to ongoing labor shortages

Labor tightness remained acute into 2026 after a challenging 2024, when 79% of United States hotels reported unfilled positions and payroll expenses increased at a double-digit pace. Higher staffing costs increase operating pressure, especially for luxury properties with service-intensive operating models in major metro markets. Brands have adopted productivity tools, streamlined service models, and targeted incentives to improve retention and control staffing volatility in the United States luxury hotel market. Training, career development, and flexible scheduling have become central to stabilizing labor supply across front-of-house, culinary, and housekeeping roles. As labor markets normalize, hotels that embed technology and process improvements can better protect margins while sustaining brand standards in the United States luxury hotel market.

Segment Analysis

By Room Type: Suites Command Dominance, Villas Gain Momentum

Suites captured 42.88% of the United States luxury hotel market share in 2025, while villas and bungalows are projected to expand at a 7.42% CAGR through 2031, reflecting a dual demand pattern for flexible space and high-privacy stays within the United States luxury hotel market. Suites serve corporate travelers who extend trips, multigenerational families, and couples seeking separate living and sleeping areas, which keeps occupancy steadier across weekdays and weekends. These configurations are aligned to work-from-anywhere lifestyles and offer attractive layouts with living rooms and workspaces that elevate both productivity and comfort in the United States luxury hotel market. Villas and bungalows attract ultra-wealthy travelers who prefer standalone residences, private outdoor areas, and dedicated service teams, which reinforces privacy as a premium feature. Operators have upgraded suites and villa categories to integrate wellness spaces, in-room dining potential, and curated amenities that match longer-stay expectations across the United States luxury hotel market.

Branded examples highlight how premium suite categories anchor positioning and rate on property. The Joseph in Nashville showcases a Presidential Suite with expansive square footage, curated art, and high-spec finishes, which illustrates how luxury rooms evolve into multifunctional sanctuaries suited to work and leisure within the United States luxury hotel industry. At Bellagio in Las Vegas, top-tier suites emphasize entertainment-ready living areas, large bathrooms, and premium bar setups that support hosting and special-occasion travel in the United States luxury hotel industry. As operators manage a mix, suites anchor steady revenue while villa-style options expand the guest base among privacy-seeking UHNW travelers. This balance supports rate integrity and length-of-stay gains within the United States luxury hotel market.

Note: Segment shares of all individual segments available upon report purchase

By Booking Channel: Direct Channels Surge as OTA Reliance Eases

Direct booking accounted for 50.05% of reservations in 2025 and is advancing at a 10.14% CAGR to 2031, signaling a structural shift toward first-party relationships in the United States luxury hotel market. This change reflects brand investments in loyalty, mobile-optimized sites, and personalized offers that reduce third-party costs and raise net revenue in the United States luxury hotel market. Hotel websites also captured the highest booking value in 2025, which improves yield when combined with on-site upsell opportunities. Hotels reinforce this shift by deploying best-rate guarantees, flexible cancellation for members, and tailored perks that protect ADR and drive repeat visits within the United States luxury hotel market.

Economics and technology both favor direct growth. OTA commissions often range from 15% to 25%, while direct channels carry limited payment-processing costs, which raises profitability per stay within the United States luxury hotel market. Trade groups expect direct digital to eclipse aggregated intermediaries over the decade as loyalty value increases and parity rules evolve, which extends brand control of pricing and merchandising in the United States luxury hotel market. AI chatbots, closed-user-group offers, and targeted remarketing improve conversion and upsell capture with minimal friction for guests. Hotels also apply a 40% to 60% direct mix target to improve resilience, which reduces exposure to commission-driven volatility while maintaining OTA presence for discovery within the United States luxury hotel market.

Note: Segment shares of all individual segments available upon report purchase

By Service Type: Resorts Lead Share, Suite Hotels Fuel Growth

Resorts held 35.66% of the value in 2025, and suite hotels are projected to grow at 8.10% through 2031, reflecting strong leisure demand and the expansion of extended-stay use cases in the United States luxury hotel market. Resorts benefit from integrated wellness, outdoor access, and family-friendly amenities that attract high-spend leisure travelers across seasons. Suite hotels align with bleisure and remote-work patterns, offering apartment-style layouts with kitchens and living areas that support longer stays in the United States luxury hotel market. Business and airport hotels remain core to weekday demand in urban and gateway nodes, although their growth pace trails the leading categories. The mix underscores how format choice tracks evolving demand and value perception in the United States luxury hotel industry.

Performance data supports this mix. Chicago set a new annual hotel revenue record in 2025 and lifted room-night demand year over year, demonstrating how flagship urban markets add resilience for higher-tier properties within the United States luxury hotel market. Extended-stay performance outpaced broader categories through late 2024, reinforcing the appeal of suite-configured brands to corporate accounts and longer-stay guests. Resorts with curated wellness, culinary, and nature-linked activities capture stronger ancillary spend and premium rates, which support investment in low-key count luxury properties paired with residential components in the United States luxury hotel market. Together, these patterns show how service types serve complementary roles in driving steady occupancy and rate performance across the cycle in the United States luxury hotel market.

Geography Analysis

The South led the United States luxury hotel market with 31.55% share in 2025, the West is forecast to grow at 7.78% through 2031, the Northeast held 27.75%, and the Midwest posted 8.2%. The South’s leadership reflects year-round leisure in Florida and steady corporate activity in Texas, which combine to stabilize occupancy and lift rate potential. Major air hubs in Atlanta, Dallas, and Miami maintain consistent international and domestic connectivity, which sustains premium demand in key resort and gateway markets within the United States luxury hotel market. The region also benefits from tax-friendly migration that has strengthened luxury demand in coastal and sunbelt destinations. Developers have responded with focused reinvestment in high-yield properties and brand expansions suited to family travel and wellness segments within the United States luxury hotel market. Elevated ADRs in beach markets continue to support product differentiation and strong on-site revenue capture in the South.

The West’s faster pace is supported by technology wealth in California and Washington, strong gateway flows through Los Angeles and San Francisco, and robust lifestyle migration into mountain sub-markets. These factors reinforce steady premium leisure demand and support year-round activity in wine and ski destinations within the United States luxury hotel market. Higher ADR baselines in marquee destinations like Napa and select mountain resorts magnify revenue potential. Operators in the West combine mixed-use development and selective renovations to capture extended-stay and wellness demand patterns. This approach strengthens property-level margins through shared amenity investments and diversified revenue streams within the United States luxury hotel market.

In the Northeast, New York remains a demand anchor, supported by finance, culture, and inbound travel once visa frictions ease. The region’s share in 2025 reflected this concentration, though international headwinds weighed on rate at times for gateway properties within the United States luxury hotel market. Chicago’s outperformance in 2025 with record hotel revenue illustrates how major Midwest cities can exceed national trends when group and leisure strength align. Midwest markets still operate from lower ADR baselines than coastal peers, but steady corporate and convention calendars should keep occupancy resilient. Taken together, regional dynamics suggest a continued tilt toward sunbelt and mountain growth while Northeast gateways regain international momentum in the United States luxury hotel market.

Competitive Landscape

The United States luxury hotel market features a mix of global brand families and high-performing independents, with Marriott International, Hilton, Hyatt, Accor, and IHG active in asset-light growth, conversions, and brand extensions. Independents compete through design, service intimacy, and strong local programming that elevates culinary and wellness experiences. Brand groups continue to optimize distribution by shifting share to direct channels and loyalty ecosystems that reduce costs and lift repeat stays within the United States luxury hotel market. Operators apply revenue management and channel strategies to preserve ADR while targeting longer-stay patterns from bleisure and extended-stay segments. Mixed-use and residential strategies help balance reliance on transient demand with fee-based income and owner-aligned structures in the United States luxury hotel market.

Leading companies executed visible expansion moves in 2025 and 2026 that shape the competitive set. Hilton reported that its luxury and lifestyle brands surpassed 1,000 properties worldwide, with nearly 500 more in development and more than 70 hotels opened in 2025, indicating sustained momentum into 2026 within the United States luxury hotel market. Four Seasons announced over 60 additional projects in planning or development, signaling focused growth across residential and hotel segments that strengthen fee-based revenues and brand reach. Rosewood accelerated its expansion cadence with new openings across regions in 2025, reinforcing brand depth in luxury resort and urban formats in the United States luxury hotel market. These moves point to sustained competition around pipeline activation, residence integration, and high-ADR destination coverage.

Digital distribution and loyalty-led economics remain central to share capture. Brands improve mobile booking journeys and invest in personalized merchandising to grow direct reservations, supported by best-rate guarantees and closed-user-group pricing that lifts conversion within the United States luxury hotel market. Vendors enable on-site chatbots and automated upsell flows that increase total spend without increased staffing burden, which supports margin protection in service-intensive segments. Hotels also deploy SEO and retargeting to convert OTA shoppers who research on aggregators but book direct once the value is clear, which advances first-party data strategies in the United States luxury hotel market. Together, these shifts underpin a more profitable channel mix and tighter guest relationship ownership across top brands and independents.

United States Luxury Hotel Industry Leaders

Marriott International

Hilton Worldwide

Hyatt Hotels Corp.

Four Seasons Hotels & Resorts

Accor SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Hilton's luxury and lifestyle brands reached over 1,000 properties globally, with nearly 500 more in development, adding almost 13,000 new rooms and opening over 70 hotels in 2025, entering five new countries: Thailand, St. Vincent and the Grenadines, Latvia, Guatemala, and Finland, demonstrating sustained global expansion momentum.

- October 2025: AKA by Korman Communities was named the #1 Extended Stay Hotel Brand in the nation by USA TODAY's 10Best Readers' Choice Awards for 2025, recognizing its luxury hotel and furnished apartment brand that redefines extended-stay experiences with residential-style suites, white-glove service, and curated lounges.

- June 2025: Four Seasons announced over 60 additional projects in planning or development, reinforcing its position as a leading luxury brand with aggressive expansion across residential and hotel segments.

- August 2025: Host Hotels & Resorts acquired the 1 Hotel Central Park for USD 265 million, signaling strong institutional investor appetite for prime urban luxury assets in gateway cities despite broader market volatility.

United States Luxury Hotel Market Report Scope

A luxury hotel provides a premium lodging experience, catering predominantly to affluent clientele with a focus on top-tier services and gourmet dining.

The US luxury hotel market is segmented by service type (business hotel, airport hotel, suite hotel, resort and spa, and other service types) and theme (heritage, contemporary, modern, and other themes). The report offers market sizes and forecasts in terms of value (USD) for all the above segments.

By Room Type

| Standard Luxury Room |

| Suites |

| Villas / Bungalows |

| Penthouses & Presidential Suites |

By Booking Channel

| Direct Booking (Brand Website, Call Center) |

| Online Travel Agencies (OTA) |

| Travel Agents / Tour Operators |

| Corporate Contracts |

By Service Type

| Business Hotels |

| Airport Hotels |

| Suite Hotels |

| Resorts |

| Other Service Types |

By Geography

| Northeast |

| Midwest |

| South |

| West |

| By Room Type | Standard Luxury Room |

| Suites | |

| Villas / Bungalows | |

| Penthouses & Presidential Suites | |

| By Booking Channel | Direct Booking (Brand Website, Call Center) |

| Online Travel Agencies (OTA) | |

| Travel Agents / Tour Operators | |

| Corporate Contracts | |

| By Service Type | Business Hotels |

| Airport Hotels | |

| Suite Hotels | |

| Resorts | |

| Other Service Types | |

| By Geography | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

What is the current size and expected growth of the United States luxury hotel market?

The United States luxury hotel market size is USD 45.89 billion in 2026 and is projected to reach USD 65.46 billion by 2031 at a 7.35% CAGR.

Which room types are leading demand in the United States luxury hotel market?

Suites led with 42.88% share in 2025, while villas and bungalows are the fastest growing at a 7.42% CAGR through 2031.

How are booking channels shifting for luxury hotels in the United States?

Direct booking held 50.05% share in 2025 and is advancing at a 10.14% CAGR to 2031, reflecting stronger brand control of guest relationships.

Which region is growing fastest in the United States luxury hotel market?

The West is the fastest-growing region with a projected 7.78% CAGR through 2031, while the South led in 2025 share.

What is driving longer stays in the United States luxury hotel market?

Corporate bleisure policies and extended-stay formats are lifting length of stay and ancillary spend across urban and resort nodes.

How are brands improving profitability in the United States luxury hotel market?

Brands are shifting mix to direct digital channels, deploying AI-enabled merchandising, and expanding mixed-use residences to stabilize RevPAR and fees.

Page last updated on: