Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 36.74 Billion |

| Market Size (2026) | USD 39.54 Billion |

| Market Size (2031) | USD 57.06 Billion |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Travel Retail Market Analysis by Mordor Intelligence

The Asia-Pacific travel retail market is expected to grow from USD 36.74 billion in 2025 to USD 39.54 billion in 2026 and is forecast to reach USD 57.06 billion by 2031 at a 7.62% CAGR over 2026-2031, signaling sustained capacity expansion, premiumization in core categories, and tighter integration of digital pre-order journeys with on-site pickup in high-traffic hubs. China remains the anchor for policy-enabled duty-free growth and cross-border traffic, while India’s airport pipeline and privatization milestones lay the groundwork for the next leg of regional throughput. Japan’s inbound recovery remains resilient on currency dynamics and route additions, enhancing conversion potential for fragrances, cosmetics, and fashion. Operators intensify assortment curation and exclusive launches to capture value-seeking yet brand-conscious travelers, while airports optimize space and tenancy structures to trade up revenue per passenger. Digital wallets and interoperable e-payments reduce friction at the point of sale for international visitors, thereby strengthening conversion for beauty, spirits, and gifts.

Key Report Takeaways

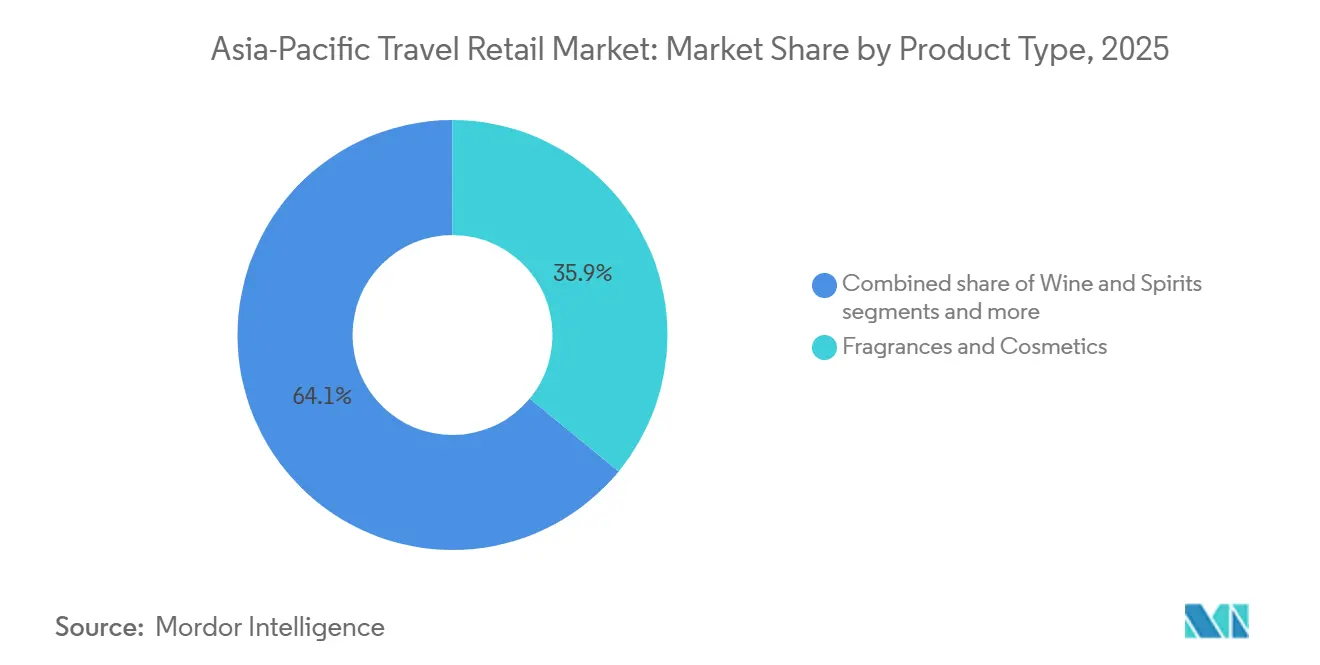

- By product type, fragrances and cosmetics led with 35.94% market share in the Asia-Pacific travel retail market in 2025, while wines and spirits are forecast to expand at a 12.10% CAGR to 2031, positioning beauty for stable repeat buying and whisky-led premiumization for growth.

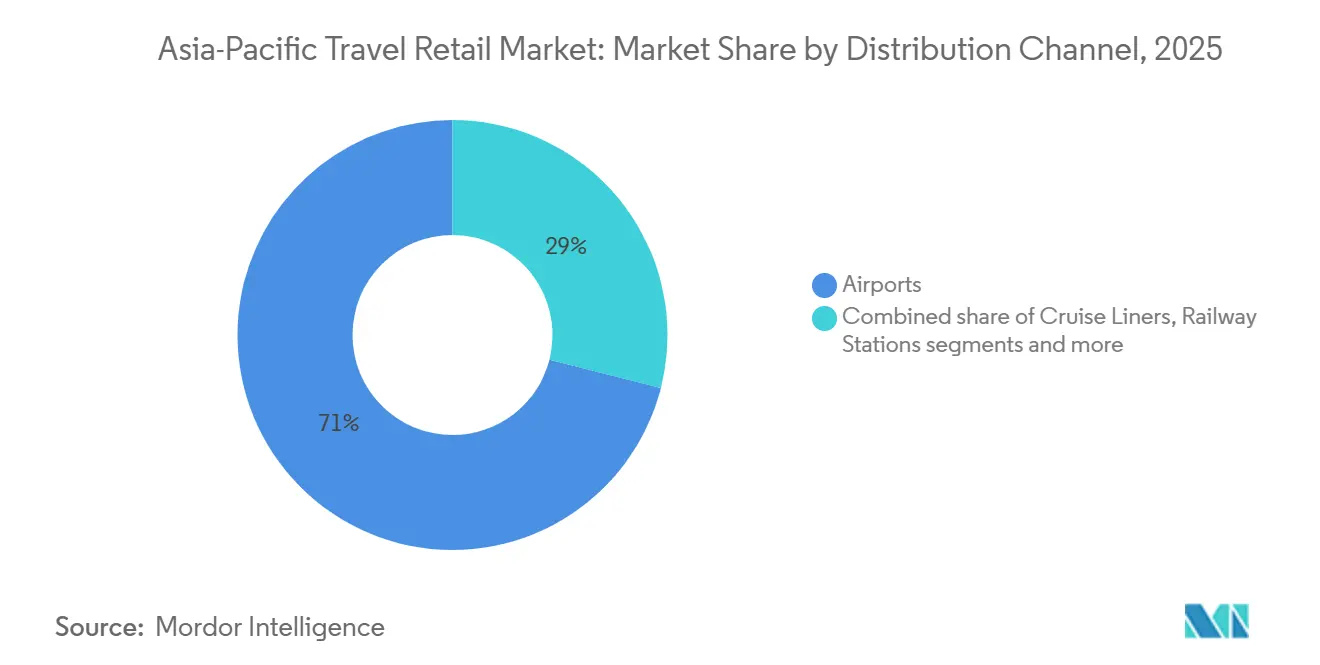

- By distribution channel, airports commanded 71.04% of the Asia-Pacific travel retail market share in 2025, and railway stations are projected to grow at a 14.55% CAGR through 2031, driven by expanding high-speed rail corridors.

- By traveler demographics, leisure travelers accounted for 51.88% of the Asia-Pacific travel retail market share in 2025, and medical and wellness tourists are projected to grow at a 14.05% CAGR through 2031, reflecting aging cohorts and cost-quality arbitrage across select destinations.

- By geography, China held 45.20% of the Asia-Pacific travel retail market share in 2025, driven by policy-enabled offshore duty-free and Tier-1 concessions, while India is the fastest-growing geography at a 12.78% CAGR through 2031, supported by new airports and terminal expansions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Travel Retail Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in Chinese outbound tourism due to visa relaxations | + 1.8% | China's core, spillover to Thailand, Japan, Singapore, Malaysia | Medium term (2-4 years) |

| Low-cost carriers expanding operations at secondary airports | + 1.2% | Southeast Asia core, India tier-2 cities | Medium term (2-4 years) |

| Rising disposable incomes driving luxury demand in Southeast Asia | + 1.4% | ASEAN-6, India urban centers | Long term (≥ 4 years) |

| Major airport and terminal expansions in India and Vietnam | + 2.1% | India, Vietnam, Japan select locations | Long term (≥ 4 years) |

| Pre-order and click-and-collect platforms boosting conversions | + 0.7% | Global, early gains in Singapore, Seoul, Hong Kong | Short term (≤ 2 years) |

| Harmonization of ASEAN duty-free allowances for consistency | + 0.6% | ASEAN-10 member states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increase in Chinese Outbound Tourism Due to Visa Relaxations

China’s border agencies recorded 697 million inbound and outbound crossings in 2025, a 14.2% year-on-year increase, supported by expanded visa-free access for 48 countries and wider application of 240-hour transit policies at 65 entry points, which lifts travel frequency and retail conversion across gateway airports and downtown duty-free stores[1]Editors, “China’s Cross-Border Travel Hits Record in 2025 on Expanded Visa-Free Access,” Xinhua, china.org.cn. Beijing Daxing International Airport carried 5.89 million international passengers in 2025, with continued route additions linking Asia, Europe, and Africa, reinforcing luxury and beauty traffic through Tier-1 concessions [2]Editorial Desk, “Beijing Daxing International Passenger Growth and Route Expansion,” Global Times, globaltimes.cn. Interoperable digital payments have accelerated, with Alipay’s international version connected to 40 overseas e-wallets and 150 million merchants in China by late 2025, lowering friction for foreign shoppers and lifting average basket sizes for key categories like fragrances, cosmetics, and accessories. Japan’s inbound arrivals reached 36.87 million in 2024, aided by yen weakness and connectivity gains, which drove stronger retail traffic for fashion, beauty, and gifts across airports such as Haneda and Kansai. Greater tourism throughput and the return of long-haul itineraries from China also provide a lift to Southeast Asian hubs, including Singapore and Bangkok, where duty-free assortments target both premium and value segments. The Asia-Pacific travel retail market benefits as these traffic corridors stabilize, improving dwell time at hub airports and increasing the share of purchases made through pre-trip discovery and on-site pickup across the region.

Low-Cost Carriers Expanding Operations at Secondary Airports

Asia-Pacific low-cost carrier connectivity expanded in 2025, establishing new traffic flows through secondary airports and raising incidental retail exposure for first-time and budget travelers on short-haul routes. Kuala Lumpur, Incheon, and Manila emerged as leading LCC hubs by network connections, channeling cost-sensitive passengers into airport shops that price for impulse beauty, confectionery, and local gifts. Vietnam revised aircraft import certifications in April 2025 to recognize more jurisdictions, broadening fleet options for local operators and supporting capacity growth tied to duty-free opportunities at current and future airports. Boeing’s outlook for Vietnam as a fast-growing aviation market bolsters the business case for new routes that bring incremental retail traffic into national gateways and planned greenfield airports. Airlines in the Philippines and Japan added efficient narrowbody fleets and new short-haul routes in 2024 and 2025, which encouraged frequent city-break travel and increased transactions in travel-sized beauty, value spirits, and grab-and-go gifts at LCC terminals. As LCC penetration rises in tier-2 cities, the Asia-Pacific travel retail market can deepen its reach with compact assortments, mobile pre-order, and fast checkout formats that suit high-turnover boarding gates.

Rising Disposable Incomes are Driving Luxury Demand in Southeast Asia

Southeast Asia’s macro backdrop improved into 2026 as the Asian Development Bank highlighted steady growth, supported spending, and policy measures that helped lift household consumption in markets such as Indonesia, Malaysia, Singapore, and Vietnam, which support a premium retail mix in airports and downtown duty-free stores. Currency shifts influence outbound destination choices for shoppers from India, Singapore, South Korea, and Taiwan, creating timing windows when luxury purchases and travel retail splurges become more attractive relative to domestic options. Prestige malt whiskies and premium beauty activations have gained traction, with launches that tie to national identity themes and limited editions that drive scarcity and higher average transaction values across flagship terminals. Duty-free operators segment high-net-worth and aspirational customers with curated boutiques, immersive pop-ups, and clienteling to grow basket sizes in spirits, jewelry, fragrances, and watches, while maintaining entry points for value shoppers. As incomes rise, the Asia-Pacific travel retail market can benefit from premiumization within beauty and spirits, as well as experiential formats that reward discovery and pre-booked services. Many airports align with this trajectory by opening larger multi-brand stores, expanding beauty halls, and integrating data-driven personalization that advances cross-selling and loyalty.

Major Airport and Terminal Expansions in India and Vietnam

India’s pipeline features large greenfield builds and major upgrades that add capacity and new retail space, with projects such as Navi Mumbai and Noida International moving toward a multi-phase scale that will multiply passenger throughput and commercial footprints in the coming years. The government approved the expansion of Varanasi’s Lal Bahadur Shastri International Airport to increase capacity and extend the runway, unlocking higher peak-hour flows and additional retail adjacency [3]Press Information Bureau, “Cabinet Approves Development of Lal Bahadur Shastri International Airport,” Government of India, pib.gov.in. Vietnam’s revised National Airport Master Plan targets 33 airports by 2030 and a significant total investment to reach 297 million annual passenger capacity, anchored by Long Thanh International Airport’s multi-phase development. Noi Bai’s Terminal 2 expansion has added capacity, counters, and biometric processes, which support smoother flows and more time for shopping before boarding, while Danang’s new cargo terminal supports broader aviation ecosystem growth. These investments help the Asia-Pacific travel retail market by adding gates, dwell capacity, and more modern commercial environments that fit pre-order pickup, data-led merchandising, and omnichannel loyalty programs.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High concession fees significantly reduce retailer profit margins | - 1.3% | China's core airports, Singapore Changi, Hong Kong, Seoul Incheon | Medium term (2-4 years) |

| Stricter regulations impacting tobacco marketing and advertising | - 0.8% | China, Singapore, Thailand, Malaysia | Medium term (2-4 years) |

| Foreign exchange volatility affects pricing parity in markets | - 0.6% | Japan, Indonesia, India, Australia | Short term (≤ 2 years) |

| Travel-light trend leading to fewer impulse purchase opportunities | - 0.4% | Global, stronger in Japan, South Korea, and Hong Kong | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Concession Fees Significantly Reduce Retailer Profit Margins

Thailand amended duty-free concession conditions across major airports from late 2025, including minimum per-passenger guarantees and revenue-share tiers that heighten fixed-cost exposure for operators, compressing profit buffers during traffic dips. Margin pressure has triggered portfolio resets and selective exits in high-rent locations, as seen in South Korea, where a leading retailer ceded an Incheon concession after persistent losses, signaling stricter hurdle rates for new bids. The concession shift at India’s largest international gateway underscores asset owners’ preference for scaled partners that invest in digital transformation and can absorb operational guarantees. Some portfolios also saw divestments, with profitability falling sharply, prompting strategic sales and consolidations that reshape competitive dynamics and bargaining positions at top-tier hubs. In response, operators are leaning into higher-margin categories, targeted brand partnerships, and omnichannel sales that raise revenue per square foot under fixed-fee regimes. The Asia-Pacific travel retail market will continue to weigh bid competitiveness against fee escalators and seek performance-linked structures that balance risk across cycles.

Stricter Regulations Impacting Tobacco Marketing and Advertising

China’s State Tobacco Monopoly Administration introduced tighter controls, effective January 2026, that prohibit e-cigarette and heated tobacco sales in duty-free channels, require digital traceability, and impose catalogue-based listings and quotas, thereby raising compliance costs and narrowing promotional latitude for nicotine categories. Singapore maintained strict tobacco marketing restrictions during the TFWA Asia Pacific Exhibition and Conference period, with narrow exemptions in restricted-access directories and app environments, underscoring how policy curbs alter retailer strategies and brand visibility. Many operators have shifted focus toward fragrances, cosmetics, wines, and spirits to offset reduced tobacco-led traffic and to support higher-margin growth in premium beauty and prestige malts. Duty-free assortments now place greater emphasis on compliant signage, SKU rationalization, and workforce training to meet audit standards across airports and downtown stores. In the Asia-Pacific travel retail market, these curbs spur innovation across other categories and encourage frictionless digital journeys that deepen engagement in beauty, fashion, and gifts while preserving regulatory integrity in the nicotine segments.

Segment Analysis

By Product Type: Fragrances and Cosmetics Lead as Prestige Spirits Accelerate

Fragrances and cosmetics accounted for 35.94% of regional sales in 2025, giving this category the highest Asia-Pacific travel retail market share and underscoring repeat-purchase behavior that sustains spend across flagship terminals and downtown formats. The Asia-Pacific travel retail market continues to see stable beauty conversion from mature female travelers and younger cohorts drawn to K-beauty, J-beauty, and curated niche brands, which in turn lift loyalty program sign-ups and pre-order baskets. Wines and spirits are projected to grow at a 12.10% CAGR through 2031, with prestige malt whiskies and travel-exclusive launches anchoring premiumization and event-driven activations across core hubs. As airports and operators curate enlarged beauty halls, single-brand boutiques, and experience-led zones, the Asia-Pacific travel retail industry gains more reasons to visit, translating into higher spend per passenger, including through click-and-collect pickup at the gate. Luxury accessories and watches broaden the premium mix with limited-edition offerings and private-client services, while health-forward confectionery selections add gifting options that balance price points and margins.

The Asia-Pacific travel retail market benefits from stronger pipeline coordination with suppliers on exclusive sets, seasonal collections, and hero SKUs that are optimized for conversion in dwell zones. Retailers deploy loyalty ecosystems and interoperable payments to increase conversion rates for foreign visitors who can navigate price comparisons and expect seamless checkout across languages and wallets. Beauty and spirits activations add theater and education, appealing to aspirational shoppers and lifting cross-category baskets in fashion, tech accessories, and gifts. The Asia-Pacific travel retail industry aligns inventory and pre-order visibility to ensure shoppers can secure high-demand items for pickup at departure or arrival, thereby strengthening value perception and mitigating carry-on limits.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Airports Dominate While Rail Gathers Pace

Airports captured 71.04% of regional distribution-channel sales in 2025, reflecting their centrality to core category mix and tenancy footprints that define the Asia-Pacific travel retail market size across national gateways and hub connectors. Railway stations are projected to expand at a 14.55% CAGR through 2031, as high-speed rail corridors extend connectivity and bring domestic travelers to modernized stations with curated retail focused on impulse beauty, local gifts, and travel essentials. Cruise terminals add incremental volume on itineraries centered on Singapore, Hong Kong, and Japan, where passenger growth and new ship deployments support duty-paid assortments of beauty, fashion, and souvenirs. Downtown duty-free formats broaden reach and enable pre-trip booking, curated events, and brand storytelling, which can lift conversion among city visitors who are not origin-destination flyers on a given day. The Asia-Pacific travel retail market continues to balance airport-led dominance with growth in alternative nodes that extend omnichannel paths to purchase and strengthen brand equity across journeys.

As airports upgrade terminals, integrate biometrics, and add self-service points, retailers can deploy pre-order and click-and-collect with more precise pick-up timing that aligns with security and boarding flows. Rail operators and station landlords refine their retail mixes to serve frequent commuters and leisure travelers with fast checkout and curated assortments that fit dwell times between connections. Cruise terminals focus on experiential retail and localized offers that encourage browsing and gifting during embarkation and disembarkation windows, backed by digital engagement before port calls. Downtown stores add flexibility for pre-trip reservations and return pickups, enabling value-conscious shoppers to time their purchases for the best selection and price confidence. By aligning data and inventory visibility, these channels can capture demand across multiple touchpoints and improve retention through loyalty and targeted communications.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Traveler Demographics: Leisure Leads as Medical and Wellness Rises

Leisure travelers accounted for 51.88% of throughput in 2025, driven by trending summer destinations like Tokyo and Osaka, which create steady demand for beauty, fashion accessories, and confectionery at airports and downtown stores across Japan and the wider region. Medical and wellness tourists are projected to grow at a 14.05% CAGR through 2031, adding a high-intent cohort that values curated, health-forward assortments and gifting, thereby elevating the Asia-Pacific travel retail market size across select airports known for such itineraries. Business travelers show a higher inclination toward click-and-collect and pre-order services, which encourages retailers to streamline pickup logistics and use CRM to convert repeat travelers with targeted offers. Visiting friends and relatives flows benefit from visa policy relaxations and transit facilitation in China, which boosts cross-border trips with shopping concentrated in beauty, gifting, and duty-paid value buys. Student travel and multigenerational cruising add further complexity to category planning, with value and premium pathways required for balanced conversion.

Corporate travel budgets continued to normalize in 2025, with rising trip volumes and greater emphasis on purposeful travel that meets commercial objectives and supports managed travel policies, while still allowing leisure extensions in some cases. Younger travelers value experiences, personalization, and sustainability, which encourages retailers to develop provenance storytelling and eco-friendly packaging in beauty and gifting. Currency sensitivity influences itinerary choices and shopping strategies across price-comparison behaviors, which encourages dynamic pricing and clear value communication in stores. As demographic cohorts diversify, the Asia-Pacific travel retail market can optimize conversion by tailoring pre-order journeys, on-site experiences, and localized assortments to traveler intent and trip purpose. Retailers that coordinate with airports and airlines on pre-trip communications and loyalty partnerships see better engagement across leisure, medical, business, and VFR travelers.

Geography Analysis

China held 45.20% of regional value in 2025, making it the largest share of the Asia-Pacific travel retail market and highlighting the pull of Hainan’s offshore duty-free ecosystem and Tier-1 airport concessions in Beijing, Shanghai, Guangzhou, and Shenzhen. Expanded visa-free access and transit policies supported 697 million cross-border trips in 2025, while international passenger flows at Beijing Daxing rose 24.56% to 5.89 million, giving major international brands broader exposure at the gate. Policy steps in late 2025 expanded duty-free product categories and allocated more space to domestic brands, reshaping the mix and supporting the discovery of Chinese heritage lines alongside global prestige assortments. China’s duty-free operators continue to expand membership and digital touchpoints, aligning online reservations with airport pickup for arrivals and departures, which boosts practical conversion for beauty and luxury gifts. The Asia-Pacific travel retail market sees China as a structural demand center, supported by policy initiatives, digital payments, and omnichannel execution for sustained growth.

India is the fastest-growing geography at a 12.78% CAGR through 2031, supported by airport privatization and an ambitious slate of greenfield and brownfield projects that add gates, terminals, and new commercial space, which lifts the Asia-Pacific travel retail market size over the forecast period. Government approvals, such as the Varanasi expansion work to raise annual passenger handling capacity and extend the runway, which improve airline scheduling and retail dwell time. The operator transition at Indira Gandhi International Airport’s duty-free business in July 2025, alongside GMR Airports' increase in its equity stake to 66.93% in December 2025, strengthens integration, assortment, and omnichannel execution capabilities. As throughput rises across Delhi, Hyderabad, Bengaluru, and new nodes like Navi Mumbai and Noida International, the mix of business, VFR, and leisure traffic will expand category opportunities in spirits, beauty, and gifting. The Asia-Pacific travel retail market gains exposure to a broad spending base in India that values both affordability and selective premium trade-ups, which can translate to higher repeat purchases with the right loyalty design.

Japan and Southeast Asia add diversified growth engines that complement China and India and expand the region’s overall retail footprint. Japan’s inbound arrivals reached 36.87 million in 2024, and airport upgrades in 2025, including at Haneda and Fukuoka, expanded store counts and dining options, extending dwell-based shopping opportunities. Avolta’s 2025 entry into Kansai’s F&B concessions underscores ongoing investment by global players in Japan’s premium traveler base, which supports cross-traffic to adjacent retail. Southeast Asia continues to advance long-term capacity plans, with Vietnam’s Long Thanh program and Noi Bai’s Terminal 2 capacity boost providing more gates, more shops, and digital infrastructure for smoother journeys that favor pre-order pickup. Singapore’s leadership in connectivity, interoperable payments, and cruise deployment adds further retail upside across duty-paid and duty-free channels.

Competitive Landscape

The Asia-Pacific travel retail market features several scaled operators with multi-country portfolios, alongside national champions and airport-led JVs that hold specific terminals or channels, creating moderate concentration amid active tender cycles and selective M&A. China Tourism Group Duty Free’s acquisition of DFS’s Hong Kong and Macau businesses in January 2026 consolidates core Greater Bay Area exposure and lays the groundwork for broader cooperation on products, stores, and customer experience. Avolta’s expansion in Japan through Kansai’s F&B contract and continued network investments reflect its commitment to scale in premium hubs, where blended F&B and retail footprints can lift overall spend. Lagardère’s wins in Auckland and a new regional structure in Singapore indicate a focus on Asia-Pacific growth, supply-chain depth, and commercial coordination that can raise offer adaptation and speed to market.

In India, an airport group increased its equity stake in Delhi Duty Free in December 2025, after assuming operations in July 2025, reinforcing a platform approach to terminal retail and potentially supporting improved loyalty, assortments, and digital checkout. Several operators continue to manage portfolio exposure to high fixed-fee concessions, while redirecting capital toward terminals and cities with better fee-to-traffic profiles and strong beauty or spirits potential. Japan’s airport landlords have invested in capacity, retail re-zoning, and omnichannel touchpoints such as e-commerce and lockers, enabling brands and operators to tighten integration of pre-book and pickup journeys, thereby supporting performance in premium categories. As traffic stabilizes, the Asia-Pacific travel retail market rewards players that combine local insight with global brand access, deep CRM capabilities, and flexible store formats across airports, downtown stores, rail, and cruise.

Partnerships with payment providers and airlines extend loyalty reach and reduce checkout friction, which increases conversion for time-pressed business travelers and value-conscious leisure shoppers. Premium spirits suppliers deploy travel-exclusive releases and cultural storytelling to differentiate in a crowded aisle, while beauty brands scale immersive services and skin diagnostics to strengthen repeat purchase cycles. Operators that advance sustainability through packaging, material choices, and local brand curation build trust with younger travelers who weigh environmental factors in their purchase decisions. The Asia-Pacific travel retail market thus favors portfolios that can balance fee structures, invest in omnichannel capabilities, and secure differentiated brand content across multiple traveler cohorts.

Asia-Pacific Travel Retail Industry Leaders

China Duty Free Group (CTGDF)

Dufry AG

Lotte Duty Free

Shilla Duty Free

Avolta AG

DFS Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: China Tourism Group Duty Free acquired DFS’s Hong Kong and Macau retail operations for approximately USD 395 million, with a strategic cooperation framework to expand product offerings, store networks, and customer experience opportunities across Greater China. The deal consolidates control of prime locations and enhances access to premium brands. It also aligns both parties for selective collaboration on activation and customer engagement. The move strengthens leadership in the Greater Bay Area.

- December 2025: GMR Airports increased its stake in Delhi Duty Free to 66.93% after acquiring a 49.9% share, following its operational takeover in July 2025, which advances an integrated operator model across major Indian airports. The platform aims to scale omnichannel services and assortments. The transition underscores airport authorities’ preference for operators with the capacity to manage fee structures. Execution focuses on category depth and digital CX.

- December 2025: Airports of Thailand amended duty-free concession terms with King Power across five airports effective December 2025, introducing updated per-passenger guarantees and revenue-share thresholds. The changes align concession horizons with infrastructure plans. They also seek to balance operator sustainability with airport revenue needs. The revisions influence future bid strategies.

- September 2025: Avolta entered Japan by securing an F&B contract at Kansai International Airport totaling about 500 sqm and four concepts, underscoring continued Asia-Pacific expansion in high-traffic, premium hubs. The entry broadens the firm’s presence in Northeast Asia. It complements existing regional locations and integrated retail-F&B models.

Asia-Pacific Travel Retail Market Report Scope

Travel retail refers to the sale of goods to international travelers in transit environments, such as airports, seaports, train stations, cruise ships, and border zones. This sector includes duty-free and duty-paid outlets that offer competitively priced products such as perfumes, cosmetics, luxury items, alcohol, tobacco, fashion, and confectionery.

The Asia-Pacific travel retail market report is segmented by product type (fashion and accessories, wine and spirits, tobacco, food and confectionary, fragrances and cosmetics, other product types including stationery, electronics, watches, jewelry), distribution channel (airports, cruise liners, railway stations, other distribution channels), traveler demographics (business travelers, leisure travelers, visiting friends & relatives, medical & wellness tourists, student travelers), and geography (India, China, Japan, Australia, South Korea, South-East Asia covering Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines, and Rest of Asia-Pacific). The market forecasts are provided in terms of value (USD).

By Product Type

| Fashion and Accessories |

| Wine and Spirits |

| Tobacco |

| Food and Confectionary |

| Fragrances and Cosmetics |

| Other Product Types (Stationery, Electronics, Watches, Jewelry, etc.) |

By Distribution Channel

| Airports |

| Cruise Liners |

| Railway Stations |

| Other Distribution Channels |

By Traveler Demographics

| Business Travelers |

| Leisure Travelers |

| Visiting Friends & Relatives (VFR) |

| Medical & Wellness Tourists |

| Student Travelers |

By Geography

| India |

| China |

| Japan |

| Australia |

| South Korea |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) |

| Rest of Asia-Pacific |

| By Product Type | Fashion and Accessories |

| Wine and Spirits | |

| Tobacco | |

| Food and Confectionary | |

| Fragrances and Cosmetics | |

| Other Product Types (Stationery, Electronics, Watches, Jewelry, etc.) | |

| By Distribution Channel | Airports |

| Cruise Liners | |

| Railway Stations | |

| Other Distribution Channels | |

| By Traveler Demographics | Business Travelers |

| Leisure Travelers | |

| Visiting Friends & Relatives (VFR) | |

| Medical & Wellness Tourists | |

| Student Travelers | |

| By Geography | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and growth outlook for the Asia-Pacific travel retail market?

The Asia-Pacific travel retail market is expected to grow from USD 36.74 billion in 2025 to USD 39.54 billion in 2026 and is forecast to reach USD 57.06 billion by 2031 at a 7.62% CAGR over 2026-2031.

Which product categories are driving sales in Asia-Pacific travel retail?

Fragrances and cosmetics led with 35.94% of 2025 sales, and wines and spirits are set to grow at a 12.10% CAGR through 2031, as beauty repeat purchases and prestige malt activations underpin growth.

Which channels will expand fastest within Asia-Pacific travel retail?

Airports held a 71.04% share in 2025, while railway stations are projected to post a 14.55% CAGR through 2031, driven by high-speed rail expansion and station retail upgrades.

Which countries are shaping the regional competitive landscape most?

China leads on policy-enabled duty-free and major concessions, while India is the fastest-growing on new airport capacity; Japan and Singapore reinforce premium traffic and omnichannel execution.

What macro or policy factors will most influence spend in Asia-Pacific travel retail?

Visa relaxations from China, yen-related inbound boosts in Japan, and Southeast Asian growth support are positive, while concession fees and stricter tobacco controls pressure margins and category mix.

How are operators improving conversion among business and leisure travelers?

Operators scale click-and-collect and pre-order for business travelers and expand experiential beauty and spirits activations for leisure shoppers, with interoperable payments simplifying checkout.