Saudi Arabia MICE Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

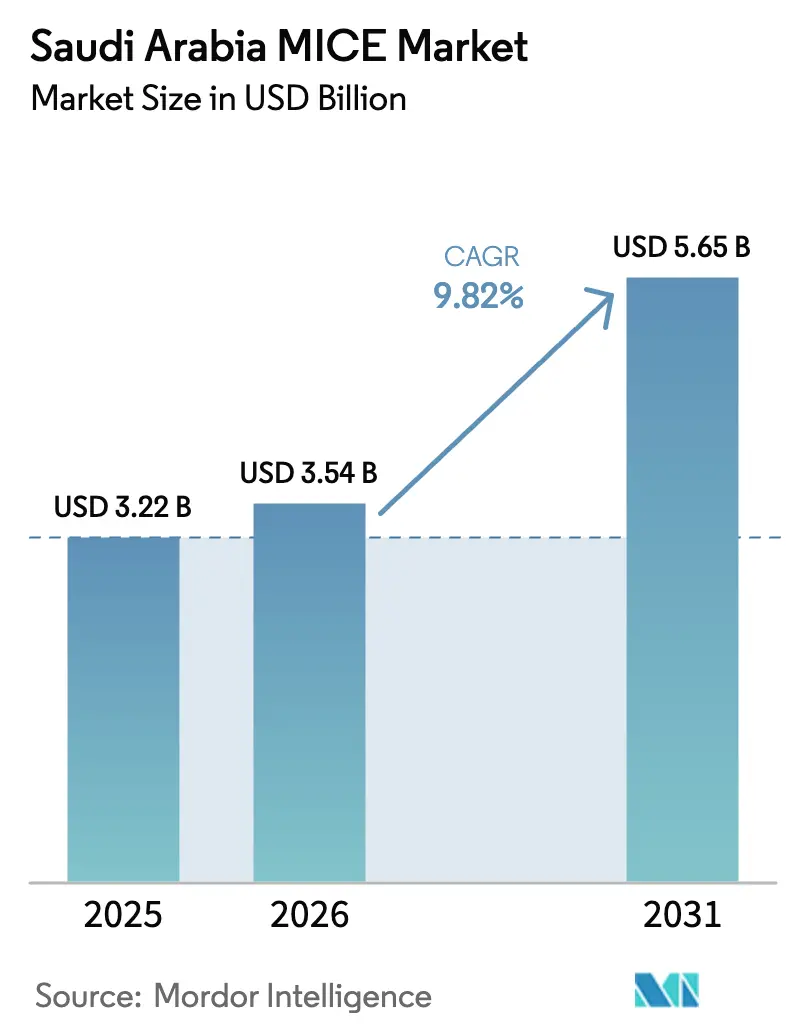

| Base Year Market Size (2025) | USD 3.22 Billion |

| Market Size (2026) | USD 3.54 Billion |

| Market Size (2031) | USD 5.65 Billion |

| Growth Rate (2026 - 2031) | 9.82% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia MICE Market Analysis by Mordor Intelligence

The Saudi Arabia MICE market size was USD 3.22 billion in 2025, is projected to reach USD 3.54 billion in 2026, and is forecast to climb to USD 5.65 billion by 2031 at a 9.82% CAGR. This expansion is supported by Vision 2030’s large-scale capital program and Public Investment Fund-backed giga-projects that add venues, hotels, and interlinked districts suited to large conferences and exhibitions. Aviation connectivity and simplified entry processes are widening access, with Saudia carrying 37 million passengers in 2025, an e-visa regime in place for more nationalities, and a 96-hour stopover visa designed to convert transit traffic into short-stay business travelers. The policy focus on tourism diversification continues, as the Ministry of Tourism notes that inbound arrivals surpassed the original 2030 target well ahead of schedule and that hospitality capacity is being scaled to meet future visitation. The ecosystem effect is clear, since capital-intensive investments in airports, hospitality, and mixed-use districts are designed to support sustained delegate flows across conferences, exhibitions, incentives, and meetings over the medium term. As new venues open under giga-projects and legacy city-center facilities expand their capabilities, organizers can secure year-round calendars for the Saudi Arabia MICE market across a broader range of price points and service levels.

Key Report Takeaways

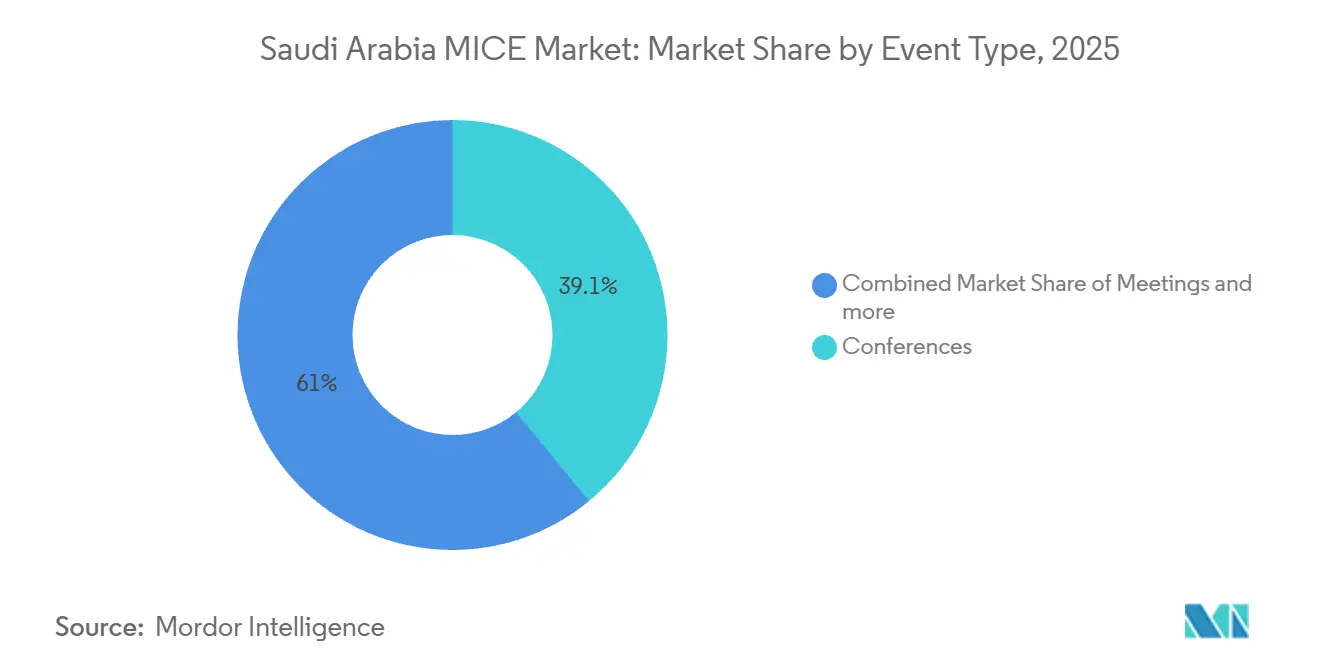

- By event type, conferences accounted for 39.05% of Saudi Arabia MICE market size in 2025, and the incentives segment is set to expand at a 14.83% CAGR through 2031.

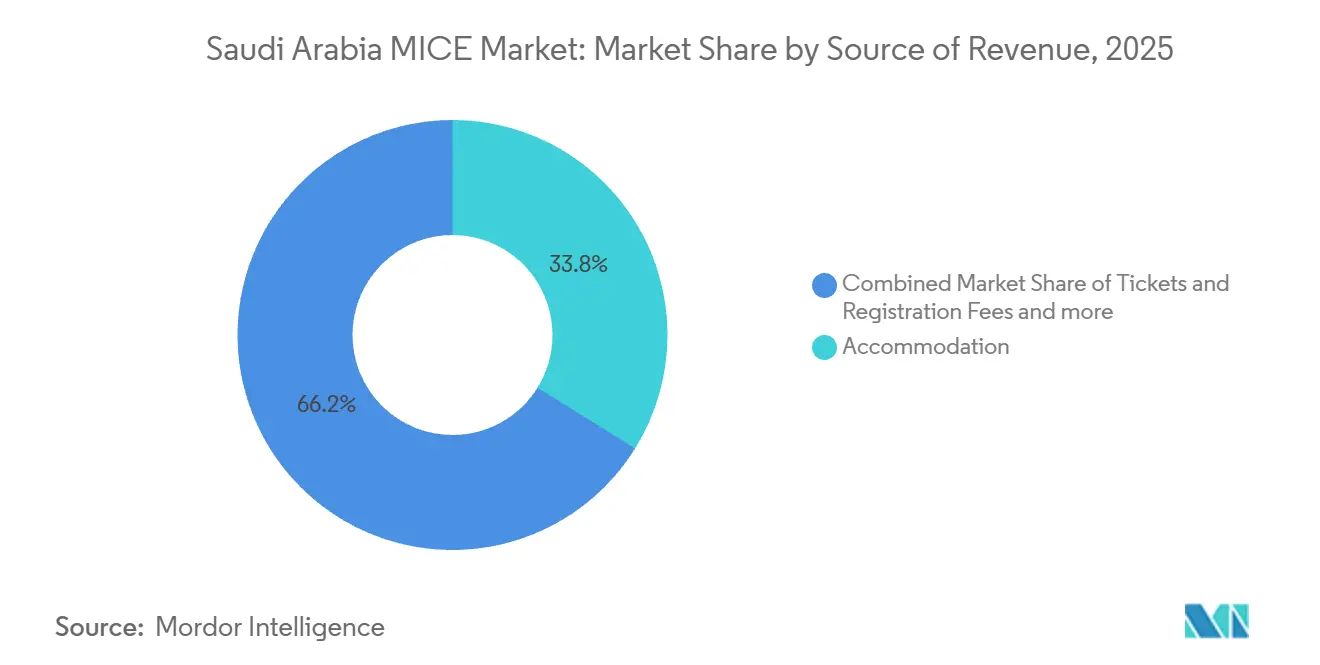

- By source of revenue, accommodation accounted for 33.84% of Saudi Arabia MICE market size in 2025, while tickets and registration fees recorded the highest growth at a 16.35% CAGR to 2031.

- By industry participant, corporate stakeholders commanded 55.92% of the Saudi Arabia MICE market size in 2025, and associations and NGOs posted an 11.97% CAGR through 2031.

- By geography, the Central Region led with 42.12% of Saudi Arabia MICE market size in 2025, while the Western Region is the fastest-growing area with a 28.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia MICE Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led Vision 2030 investment in business tourism infrastructure | +2.8% | National, with concentrated impact in Riyadh, Jeddah, NEOM | Long term (≥ 4 years) |

| Surge in giga-projects (NEOM, Qiddiya) adding world-class venues | +2.1% | National, with primary focus on NEOM, Qiddiya, Red Sea Project | Medium term (2-4 years) |

| Expansion of national carrier Saudia and Riyadh Air is boosting connectivity | +1.7% | National, with hub effects in Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Growing corporate demand for incentive travel packages | +1.4% | National, with premium segments in Riyadh, Red Sea destinations | Short term (≤ 2 years) |

| Rise of "bleisure" extensions encouraged by new e-visa schemes | +0.9% | National, with spillover effects to AlUla, Tabuk, Abha | Short term (≤ 2 years) |

| MICE demand from rapidly expanding fintech & gaming clusters | +0.8% | National, with technology hubs in Riyadh, KAUST, NEOM | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-led Vision 2030 Investment in Business Tourism Infrastructure

Saudi Arabia’s capital program is enlarging the supply of high-spec venues and hotels, and it is backed by sovereign initiatives that integrate convention-grade facilities into broader urban and tourism plans. SCEGA’s infrastructure reporting and official communications highlight rising volumes of accredited venues, exhibition capacity, and meeting seats, collectively creating headroom for larger event calendars across cities and giga-project districts. Aviation infrastructure is planned at a scale consistent with sustained delegate growth, with King Salman International Airport’s master plan targeting 120 million annual passengers by 2030 and incorporating meeting space within terminals to simplify transfers for business travelers.[1]Amadeus, “Riyadh Air Partners with Amadeus to Power Global Travel Distribution,” Amadeus, amadeus.com Vision 2030 framing documents underscore the objective to diversify the economy by growing tourism and entertainment, with business events positioned as a high-value segment that supports hotels, airlines, ground transport, and food service. Public and private developers are also encouraged to align new hotel and mixed-use builds with conference and exhibition functionality, ensuring ballrooms and divisible meeting rooms can switch between corporate events and social demand to maximize utilization and return on capital. Together, these initiatives are strengthening the foundation for multi-format event delivery and are creating a consistent pipeline of venues that improve planning visibility for organizers in the Saudi Arabia MICE market.

Surge in Giga-Projects Adding World-Class Venues

Giga-projects such as NEOM, Qiddiya, and Red Sea Global developments are embedding meeting, incentive, and exhibition capabilities into destination-scale master plans. NEOM’s program is designed to anchor next-generation urban and resort environments with innovation districts and hospitality offerings that can host high-profile meetings alongside leisure extensions, and it carries Public Investment Fund backing as part of Saudi Arabia’s strategic development agenda.[2]Public Investment Fund, “Giga-Projects - Public Investment Fund,” Public Investment Fund, pif.gov.sa Qiddiya is positioned as a global entertainment and sports destination on Riyadh’s periphery, and official program narratives emphasize that the project will deliver major attractions, esports infrastructure, and multipurpose event spaces that cater to incentive groups and experiential corporate gatherings. Red Sea Global is scaling a luxury coastal cluster with marine and nature assets that are attractive to executive retreats and incentive groups, and the program’s targets for resorts and rooms through 2030 reflect a plan to support premium events requiring privacy and diversified leisure access. Diriyah’s heritage redevelopment is set to deliver hotels and cultural institutions in a UNESCO setting, which expands the range of culturally immersive pre- and post-conference experiences in the Riyadh area[3]Vision 2030, “Qiddiya,” Vision 2030, vision2030.gov.sa. The combined effect is a pipeline of differentiated event destinations that reduce reliance on single-purpose convention centers and add capacity for the Saudi Arabia MICE market across a wide range of formats and budgets.

Expansion of national carrier Saudia and Riyadh Air is boosting connectivity

Aviation growth is expanding the addressable delegate pool, since new and more frequent routes reduce travel time and broaden origin markets for organizers. Saudia confirmed it transported 37 million passengers in 2025 and continues to expand international service, which supports business events that depend on steady and reliable airlift to the capital and the western gateway.[4]TTR Weekly, “Saudia flies 37 million passengers in 2025,” TTR Weekly, ttrweekly.comComplementing that, Riyadh Air plans to begin commercial operations in 2026 under a Public Investment Fund mandate to enhance long-haul connectivity and strengthen Riyadh’s role as a hub for premium and transfer traffic. Distribution and technology partnerships, such as the Riyadh Air agreement with Amadeus, indicate investment in the digital backbone needed for global sales and itinerary servicing, which benefits corporate travel managers arranging complex MICE itineraries. Ongoing airport upgrades and master plans highlighted on official portals point to sustained increases in passenger capacity across Riyadh and Jeddah, which will relieve bottlenecks during peak event seasons. Visa facilitation adds to this momentum, as the e-visa and the 96-hour stopover program reduce friction for short-notice, short-stay business travelers, who are a core audience for conferences and exhibitions in the Saudi Arabia MICE market.[5]Ministry of Tourism, Saudi Arabia, “IMF Recognizes Saudi Arabia’s Surpassing of Vision 2030 Tourism Target,” Ministry of Tourism, mt.gov.sa.

Growing Corporate Demand for Incentive Travel Packages

Corporate interest in incentive travel is rising as companies seek memorable, values-aligned experiences that can reward performance and reinforce culture. The incentives segment has the highest forecast growth rate among event types, a trajectory supported by the rollout of upscale leisure assets in heritage and coastal destinations that can be paired with executive programming. Program narratives for NEOM and other flagship developments emphasize renewable energy and environmental stewardship, helping multinationals reconcile their internal sustainability policies with premium itineraries for senior teams. Visa liberalization and airport VAT refund processes reduce administrative friction and improve perceived value, thereby supporting conversion among incentive groups that link business sessions to curated leisure days. The steady addition of upper-upscale and luxury hotels in strategic nodes such as Makkah, Diriyah, and the Red Sea region is broadening the inventory of properties that can host incentive cohorts with high service standards and on-site event spaces. These elements combine to create a favorable environment for incentive planners seeking differentiated venues and frictionless logistics in the Saudi Arabia MICE market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified meeting-planning professionals | -1.2% | National, with acute pressure in NEOM, AlUla, Abha | Medium term (2-4 years) |

| Seasonality due to extreme summer temperatures | -0.9% | National, especially in outdoor venues and non-climate-controlled sites | Short term (≤ 2 years) |

| High dependence on the expatriate event workforce | -1.1% | National, with concentration in Riyadh, Jeddah, and NEOM | Medium term (2-4 years) |

| Limited Tier-2 city airlift restricting regional dispersal | -0.8% | Emerging cities, including AlUla, Abha, Dammam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified Meeting-Planning Professionals

Rapid growth in venues and hotel pipelines has outpaced the supply of certified planners, production specialists, and multilingual service talent, which creates hiring strains during peak seasons. Industry training initiatives and professional development programs are expanding, but the near-term skills mix still requires many organizers and venues to supplement with external specialists, which increases costs and compresses margins for budget-sensitive events. Government and industry stakeholders continue to roll out training cohorts and accreditation pathways, though graduates need time to gain on-the-ground experience across bidding, sponsorship, and hybrid broadcast execution. The challenge is most acute in new or remote destinations, where project timelines and pre-opening staffing ramps need to be synchronized with event calendars to avoid last-minute resourcing gaps. As more international associations and corporates commit to Saudi dates, workforce development and credentialing remain essential for improving service reliability and delegate experience in the Saudi Arabia MICE market.

Seasonality Due to Extreme Summer Temperatures

Summer climate conditions constrain event design and attendee comfort, which pushes a large share of meetings and conferences into cooler months from late fall through spring. This clustering can limit venue availability in peak windows and depress attendance for events scheduled during hotter months, even when organizers offer favorable pricing or enhanced amenities. Projects such as Qiddiya and elements of NEOM are incorporating extensive indoor and climate-controlled venues that can host large-scale events year-round, although completion timelines mean some existing facilities remain seasonally exposed in the mid-2020s. Organizers often prioritize dates around major city calendars and national holidays to sustain delegate energy and ensure program flexibility across indoor and outdoor functions. Over time, venue technology upgrades and diversified destination options are expected to ease summer gaps and widen scheduling flexibility within the Saudi Arabia MICE market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Event Type: Conferences Drive Market Leadership

Conferences accounted for 39.05% of 2025 activity, while the incentives segment is the fastest-growing with a forecast 14.83% CAGR through 2031, signaling a pivot toward experience-led corporate programs that extend trips with leisure components. The capital hosts a full slate of flagship events that draw senior decision-makers and multi-track audiences, including finance, technology, and public policy gatherings that require high-security logistics and modern convention infrastructure. Incentive itineraries are benefiting from the opening of luxury assets in the Red Sea region and from heritage-led experiences around Diriyah and AlUla that can be programmed as exclusive tours with curated dining and culture. Visa simplification supports this shift, since streamlined entry and the stopover program make it easier for executives to add leisure days to business travel without extending overall travel complexity. The Saudi Arabia MICE market continues to favor conferences in volume terms, yet incentives are where operators are pushing premium packages and differentiated experiences that can support higher yields for organizers and venues.

This event-type mix is reinforced by the growing roster of specialized trade shows and format innovation among exhibition organizers. INDEX Saudi Arabia 2025, for example, showcased international exhibitors in interiors and fit-out, underlining the momentum for vertical communities that rely on in-person product discovery and dealmaking. Meetings remain the smallest event-type category by share, yet they are essential in high-compliance industries and for leadership off-sites, where face-to-face time is central to the program objective and cannot be substituted by fully virtual formats at the same efficacy. Gaming and fintech ecosystems also influence programming content, with the Esports World Cup and related events proving the draw of blended entertainment and B2B sponsorship models that extend beyond traditional conference agendas. As new resort and city-center venues join the inventory, broader dispersion across event types is likely, but the current configuration supports the view that incentives will continue to post the fastest growth in the Saudi Arabia MICE market through the forecast window.

Note: Segment shares of all individual segments available upon report purchase

By Industry Participant: Corporate Dominance with Association Upside

Accommodation generated 33.84% of 2025 revenues, while tickets and registration fees have the highest expected growth at a 16.35% CAGR through 2031, pointing to stronger organizer pricing power as delegate profiles tilt toward senior decision-makers and specialized buyers. Hotels continue to anchor large event budgets, particularly for multi-day conferences with pre- and post-event programming that requires on-site meeting rooms, ballrooms, and suites for private sessions and sponsor engagement. Upscale and luxury inventory additions by major hotel groups around the Red Sea and in Riyadh’s heritage districts introduce properties with high service levels that support VIP hosting and tailored F&B, which is central to high-yield corporate events. Food and beverage play a larger role in program design as operators differentiate with local culinary experiences that can be staged in grand ballrooms or in culturally resonant settings tied to destination narratives. Advertising and sponsorship revenue is helped by growth in gaming and technology content, where the Esports World Cup’s scale illustrates the potential for integrated brand activations and measurable lead capture within and beyond the event perimeter.

The revenue mix is also shifting as organizers refine tiering strategies and value propositions for premium passes, curated matchmaking, and closed-door sessions. Stronger air connectivity and visa facilitation increase conversion for time-sensitive travelers who place a premium on condensed, high-value agendas and guaranteed access to senior peers, which supports pricing for passes that include concierge services and small-format networking. On the accommodation side, room-night yields benefit from clustering of flagship events in peak windows, but organizers and hotels are also co-designing offers that distribute demand into shoulder periods to improve occupancy balance. The Saudi Arabia MICE market has sufficient runway to support this premiumization, since the combination of more branded hotels and destination-scale projects is expanding the pool of properties and venues capable of hosting high-spec corporate programs at scale. As the supply base broadens and digital tools make lead qualification and sponsorship attribution more precise, tickets and advertising are positioned to contribute a rising share of the overall Saudi Arabia MICE market over the forecast period.

By Source of Revenue: Accommodation Leads, Registration Fees Accelerate

Corporate participants held 55.92% in 2025, and associations and NGOs are projected to grow at an 11.97% CAGR through 2031 as multilateral bodies and standards organizations increase in-person convening in the Kingdom. This momentum is aided by policy visibility and regulatory engagement in Riyadh, which facilitates programming that requires ministerial participation or cross-agency coordination. Hosting of global institutional gatherings and assemblies has signaled capacity and willingness to stage complex events, which encourages further bids and rotations by international associations evaluating Middle East sites. Partnerships between government entities and event operators streamline permitting and licensing workflows for cross-border topics such as standards setting, water management, and inclusion, which accelerates go-to-market timelines for association conferences. The result is a more balanced portfolio in the Saudi Arabia MICE market across corporate, public sector, and association participants, with the association segment rising from a smaller base on stronger annualized growth.

Corporate demand remains the volume anchor but is selectively prioritized for high-stakes product launches, regional kickoffs, and board-level meetings that require secure environments and premium service. Event brands and operators tied to major associations and global organizers are expanding their Saudi footprints, as seen in the growth of professional exhibitions like the Saudi Event Show, which provides a forum where buyers vet AV, staging, and catering suppliers in one place. The Saudi Arabia MICE industry continues to benefit from a policy environment that invites international headquarters to increase their local presence, which in turn expands the base of corporate buyers and partners for year-round scheduling. Collectively, these shifts point to a healthier spread of client types that reduces over-reliance on any single category and sustains demand for small to very large event footprints across the Saudi Arabia MICE market.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

The Central Region captured 42.12% in 2025 and remains the largest node due to administrative centrality and a high density of accredited venues, while the Western Region is the fastest-growing geography with a 28.03% CAGR through 2031, supported by coastal appeal and substantial air connectivity investments. Riyadh’s venue ecosystem spans large exhibition centers and purpose-built conference facilities that can host multi-track programs and high-security delegations, and it links directly to the capital’s continuing airport upgrades and master plans. Jeddah’s position as the western gateway supports high international throughput, and long-term capacity plans for King Abdulaziz International Airport point to scalability that matches anticipated growth in business events and incentive travel along the Red Sea corridor. The Saudi Arabia MICE market share of the Central Region reflects the concentration of ministries and corporate headquarters that rely on ready access to officials and partners, a configuration that will persist even as coastal projects enlarge their venue base. As more mixed-use districts open in Riyadh and as Red Sea and heritage destinations mature, planners gain a broader spectrum of formats and settings to stage events of varying size and complexity in the Saudi Arabia MICE market.

Riyadh’s growth outlook is tied to air hub development, improved international scheduling, and the continued addition of high-spec venues near government and financial districts. The King Salman International Airport master plan includes six runways and terminal configurations that anticipate large-scale passenger volumes by 2030, and on-terminal meeting facilities are intended to minimize transfer times for business travelers who require swift movement between flights and event sites. In the Western Region, Jeddah Superdome and other large venues provide indoor capacity for exhibitions and conferences, and the city’s waterfront and heritage assets increase the appeal of programs that blend daytime business with evening leisure. In Makkah, growing hotel capacity offers off-peak windows when properties can host corporate events and incentive groups while maintaining strong religious tourism seasons, thereby improving asset utilization across different demand profiles. The Eastern Province adds technical conferences linked to petrochemicals and energy, while northern and southern destinations are positioned longer term as their airport and venue infrastructure expands along with giga-project development in nearby zones.

Intra-regional dynamics show each area sharpening a distinct value proposition. The Central Region leverages proximity to policymakers and a high concentration of suppliers that support rapid event build-outs across formats. The Western Region markets an attendee-friendly mix of airport convenience, indoor capacity, and coastal leisure that encourages extended stays, which benefits both conferences and incentives. The Eastern Province serves industry-specific needs with technical venues and ready corporate demand, while future growth in the northern and southern regions is linked to destination brand building, better airlift, and purpose-built facilities that can attract mid-sized association gatherings. As these geographic strategies progress, organizers can match event objectives with city and venue strengths to sustain utilization and experience quality across the Saudi Arabia MICE market.

Competitive Landscape

The Saudi Arabia MICE Market is experiencing rising competitive intensity as international hotel brands, sovereign-backed developers, venue operators, and global organizers expand their footprints and capabilities. IHG has committed to over 100 hotels open and in the pipeline, signaling confidence in sustained corporate, public sector, and leisure demand. Accor’s scheduled openings include luxury and MICE-capable properties that broaden the supply of branded venues in key cities and destination clusters. Giga-project developers are integrating accommodations, venues, and destination management services under single-operating groups, introducing vertically integrated competitors that can bundle experiences, logistics, and space. This combination of legacy city-center operators and new destination-scale entrants is raising service and technology standards while expanding options for buyers across formats and price points.

The Saudi Arabia MICE Market is further shaped by global organizers and event brands scaling their presence and partnering with local entities to accelerate delivery and expand annual calendars. Events like the Saudi Event Show highlight the growing professional community and a widening supplier base that supports high-quality production across industries. Venues are adopting advanced registration, access control, and matchmaking tools, while flagship properties invest in hybrid broadcast capabilities to monetize digital audiences alongside in-person attendees. At the same time, regional venues with earlier-stage technology focus on cost and location advantages, creating a two-tier environment of premium and value-focused options. This competitive diversity attracts a broader set of organizers and supports year-round utilization patterns across the Kingdom.

The Saudi Arabia MICE Market is increasingly influenced by sustainability and design differentiation as key factors in buyer decisions. Properties combining credible environmental certifications with flexible room layouts and embedded networking spaces are prioritized for multi-day conferences, incentive programs, and exhibitions. Content-intensive sectors, such as gaming, demonstrate the value of immersive formats and sponsorship activation, with events like the Esports World Cup anchoring experiential and B2B crossover programming. Venue operators are refining their offerings with outcomes-based pricing and data-driven service agreements, emphasizing measurable impact on lead quality, attendee satisfaction, and sponsor ROI. Over time, the competitive landscape is expected to favor suppliers who can deliver both premium experiences and tangible performance outcomes.

Saudi Arabia MICE Industry Leaders

Marriott International

Hilton Worldwide

Accor

InterContinental Hotels Group (IHG)

Radisson Hotel Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: IHG Hotels & Resorts marked 50 years in Saudi Arabia on November 26, 2025, surpassing 100 hotels open and in the pipeline, including InterContinental Red Sea Resort and upcoming voco/Indigo properties adding 1,700 rooms near King Abdulaziz International Airport.

- November 2025: Saudia launched direct flights from Dammam to London in October 2025, expanding business-travel connectivity from the Eastern Province’s petrochemical hub to European financial centers, reducing total travel time versus Riyadh connections.

- November 2025: Saudi Arabia has launched a bold expansion of its Meetings, Incentives, Conferences & Exhibitions (MICE) sector, highlighted by the International MICE Summit 2025 (IMS25) in Riyadh, which opened with 20 major agreements and MoUs and saw global companies announce new offices, boosting investment and business events infrastructure.

- September 2025: INDEX Saudi Arabia 2025 attracted over 400 exhibitors from 33 countries at Riyadh Front Exhibition & Conference Center from September 9-11, marking the largest edition of the interiors and fit-out trade event, with Architecture and Design Commission spotlighting the "Designed in Saudi" initiative.

Saudi Arabia MICE Market Report Scope

MICE, or meetings, incentives, conferences, and exhibitions, represents a specialized industry within the travel and tourism sector. MICE involves organizing and hosting business events such as corporate meetings, incentive travel for rewarding employees, large-scale conferences, and trade exhibitions. MICE events are characterized by their emphasis on networking, professional development, and showcasing new products and services.

The Saudi Arabian MICE market is segmented by type and source of revenue. By type, the market is segmented into meetings, incentives, conferences, and exhibitions. By source of revenue, the market is segmented into tickets and registration fees, accommodation, food and beverages, advertising, and other sources of revenue. The report offers market sizes and forecasts in value (USD) for all the above segments.

| Meetings |

| Incentives |

| Conferences |

| Exhibitions |

| Tickets and Registration Fees |

| Accommodation |

| Food & Beverage |

| Advertising |

| Corporate |

| Government & Public Sector |

| Associations & NGOs |

| Central Region |

| Western Region |

| Eastern Region |

| Northern Region |

| Southern Region |

| By Event Type | Meetings |

| Incentives | |

| Conferences | |

| Exhibitions | |

| By Source of Revenue | Tickets and Registration Fees |

| Accommodation | |

| Food & Beverage | |

| Advertising | |

| By Industry Participant | Corporate |

| Government & Public Sector | |

| Associations & NGOs | |

| By Region | Central Region |

| Western Region | |

| Eastern Region | |

| Northern Region | |

| Southern Region |

Key Questions Answered in the Report

What is the growth outlook for the Saudi Arabia MICE market through 2031?

The Saudi Arabia MICE market size was USD 3.22 billion in 2025, is expected to reach USD 3.54 billion in 2026, and is projected to hit USD 5.65 billion by 2031 at a 9.82% CAGR, supported by large-scale infrastructure programs and improved air connectivity.

Which region leads and which is growing the fastest within Saudi Arabia?

The Central Region leads by share at 42.12% in 2025, while the Western Region is the fastest-growing with a 28.03% CAGR through 2031, reflecting infrastructure maturity in Riyadh and coastal appeal and airlift advantages in Jeddah and nearby destinations.

Which event type is the largest, and which is scaling the quickest?

Conferences lead with 39.05% of 2025 activity, while incentives show the fastest growth at a 14.83% CAGR to 2031, driven by premium experiences in heritage and coastal destinations.

What are the main growth drivers for business events in Saudi Arabia?

Vision 2030 led investment, giga-project venues, expanding airline networks, and easier entry through e-visa and stopover programs combine to increase venue supply and improve access for international delegates.

Which revenue stream is positioned to grow fastest for event organizers?

Tickets and registration fees have the highest growth outlook at a 16.35% CAGR through 2031, while accommodation remains the largest revenue component at 33.84% in 2025, reflecting both premiumization and hotel-driven budgets.

Page last updated on: