Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

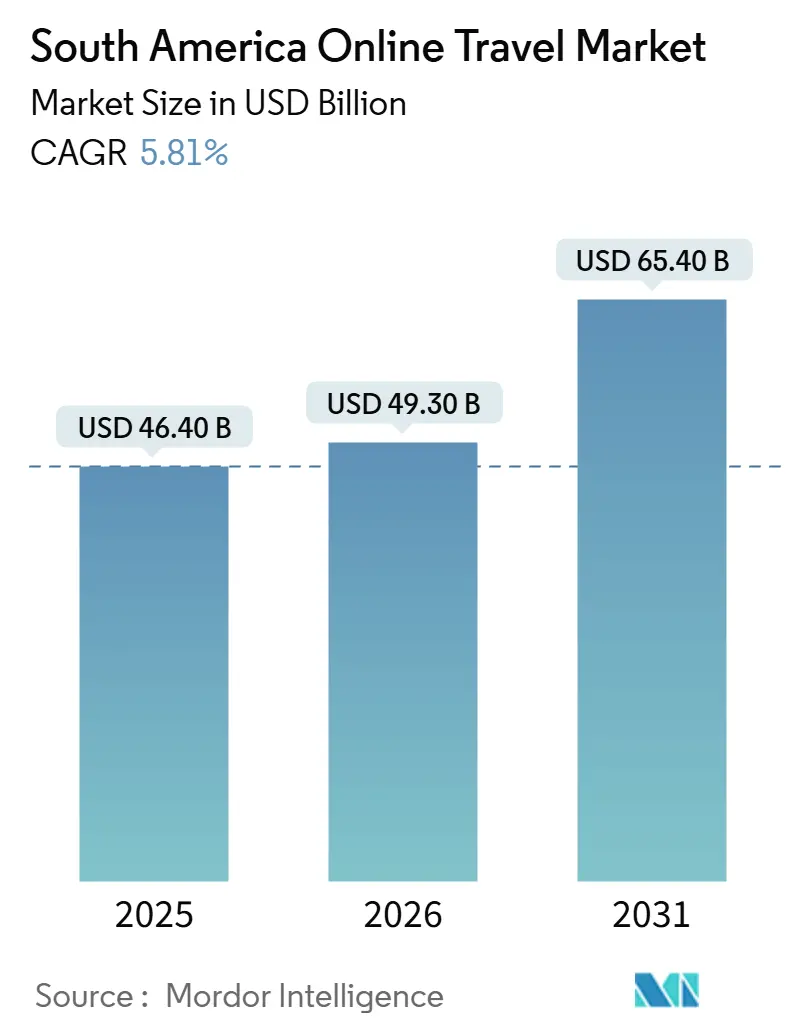

| Base Year Market Size (2025) | USD 46.40 Billion |

| Market Size (2026) | USD 49.30 Billion |

| Market Size (2031) | USD 65.40 Billion |

| Growth Rate (2026 - 2031) | 5.81% CAGR |

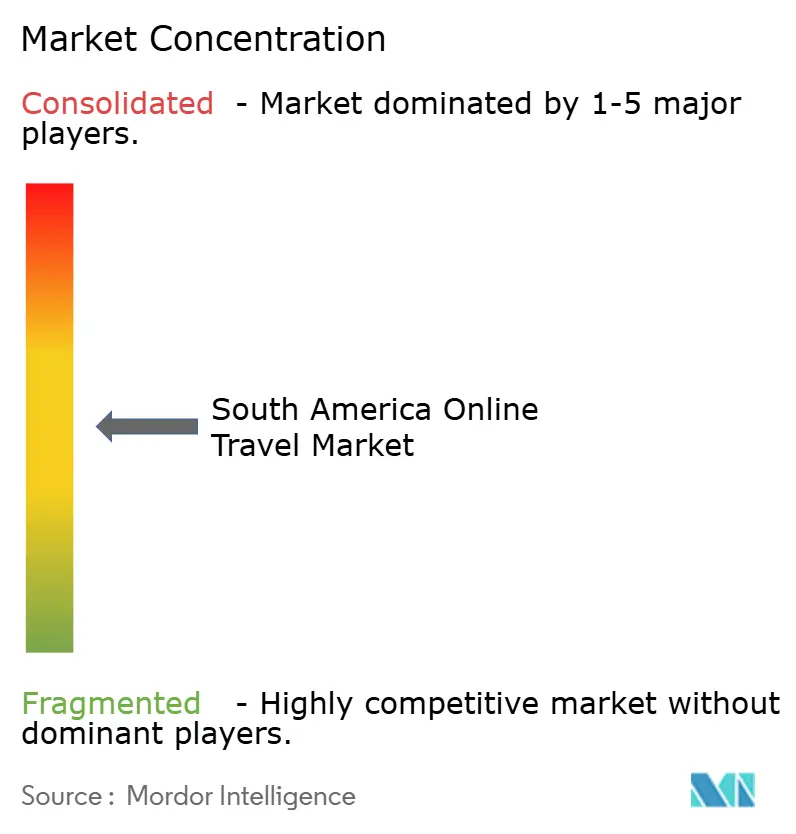

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Online Travel Market Analysis by Mordor Intelligence

The South America online travel market size is USD 46.4 billion in 2025, expected to reach USD 49.30 billion in 2026 and USD 65.40 billion in 2031, reflecting a 5.81% CAGR. The South America online travel market is expanding despite currency volatility and uneven macroeconomic conditions, supported by rising digital adoption and mobile-first booking behavior. More than half of travel bookings are expected to be made online in 2025, marking a key structural shift in consumer behavior across the region. Real-time payment systems and instant transfer rails are reducing checkout friction and improving conversion rates for online travel agencies (OTAs) and suppliers. The rapid adoption of digital wallets and embedded loyalty programs within super-app ecosystems is further extending reach and strengthening customer retention. Airline capacity recovery and growing intraregional passenger volumes are fueling demand for flights and dynamic travel packages. Carriers are enhancing retail capabilities through New Distribution Capability (NDC) content, enabling richer product merchandising and personalization for integrated OTAs. Fraud and chargebacks remain significant cost pressures, but investments in tokenization, real-time alerts, and strong customer authentication are helping mitigate risk.

Key Report Takeaways

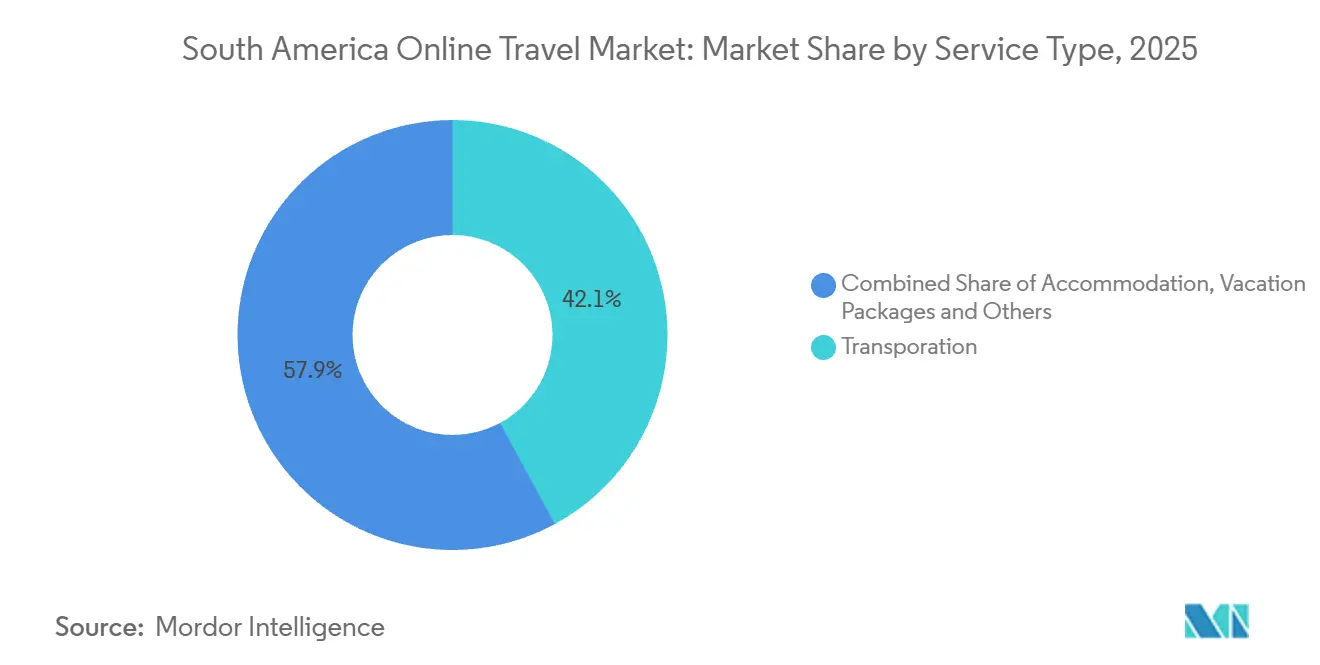

- By service type, transportation accounted for 42.1% of South America online travel market size in 2025, while accommodation is forecast to expand at a 5.93% CAGR to 2031.

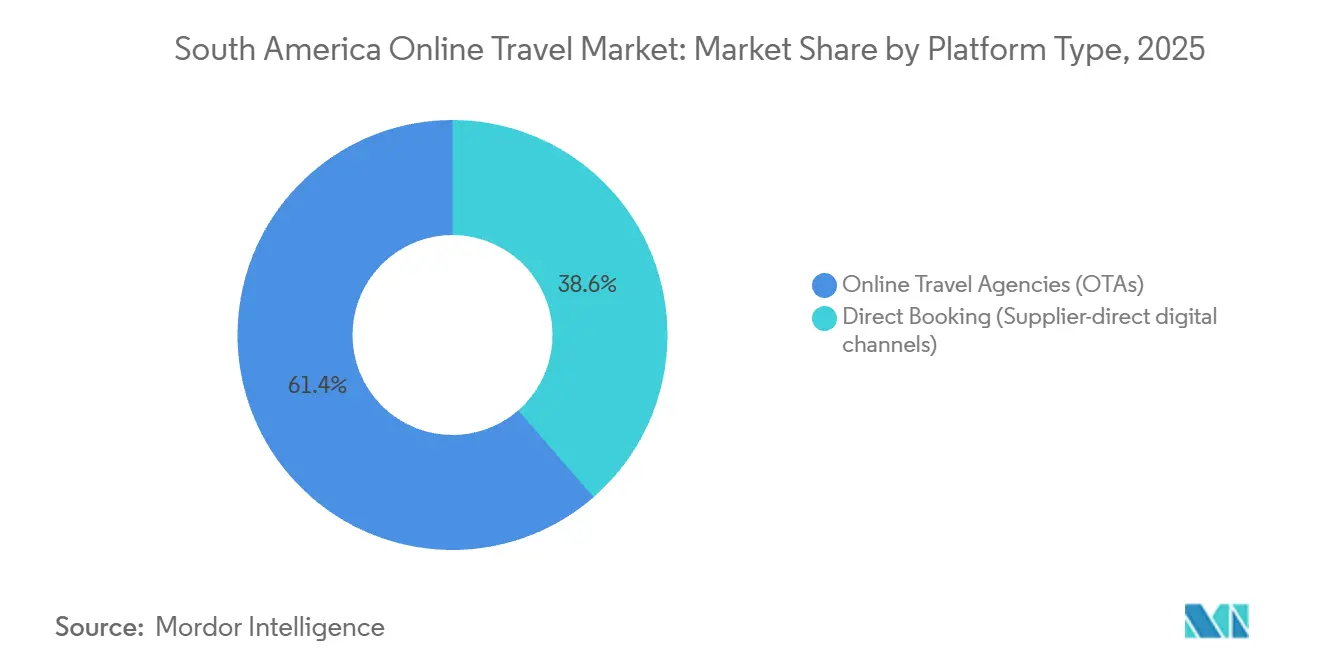

- By platform type, OTAs held 61.4% of the South America online travel market size in 2025 and are projected to grow at a 6.4% CAGR through 2031.

- By device type, mobile captured 69.2% of the South America online travel market size in 2025 and is growing at a 6.1% CAGR through 2031.

- By geography, Brazil led with 29.3% of South America online travel market size in 2025, while Argentina posted the fastest projected growth at a 5.88% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Online Travel Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile-first access and app-based booking adoption | +1.2% | Global, with highest penetration in Brazil and Chile | Short term (≤ 2 years) |

| Instant and alternative payments (PIX, wallets) lift conversion | +1.5% | Brazil core, spillover to Argentina via PIX Roaming | Medium term (2-4 years) |

| OTA penetration and super-app travel ecosystems scale reach | +1.1% | Brazil, Colombia; Rappi and Despegar expanding regionally | Medium term (2-4 years) |

| Airline capacity recovery and NDC-driven retailing | +0.8% | Region-wide; Brazil and Argentina lead passenger growth | Short term (≤ 2 years) |

| Bus-ticketing digitization across markets | +0.3% | Brazil dominant; Colombia, Peru early adoption | Long term (≥ 4 years) |

| Open banking and instant-refund rails reduce friction | +0.6% | Brazil advancing; Chile, Colombia regulatory rollout 2026+ | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mobile-First Access And App-Based Booking Adoption Surge Conversion

Airbnb’s Q4 2025 financial results show how mobile-first access and app-centric innovations are driving higher conversion and booking growth globally, a trend that is highly relevant to the South America online travel market. In the quarter, nights and seats booked grew about 10% year-over-year, while gross booking value increased 16%, reflecting strong consumer engagement with the platform’s digital channels. A key factor was the continued shift to mobile: app-based bookings rose roughly 20% year-over-year and accounted for 64% of total nights booked, up from 60% previously, indicating that more travelers are completing reservations through mobile apps rather than desktop or web interfaces. [1]Source: Airbnb Newsroom Team, “Airbnb Q4 2025 financial results,” Airbnb, news.airbnb.com. This mobile dominance is supported by product enhancements such as improved search, flexible features like “Reserve Now, Pay Later,” updated cancellation policies, and deeper AI integration within the app, all of which reduce friction and make mobile checkout more appealing. Growth in expansion markets including particularly strong performance in Brazil and acceleration in first-time bookers further suggest that a mobile-first strategy is widening the customer base, especially in regions with rising smartphone penetration. These trends underscore that seamless app experiences, localized features, and flexible payment options are key drivers of conversion in the digital travel landscape.

Instant And Alternative Payments Lift Conversion And Lower Merchant Costs

Instant payments now underpin the South America online travel market with lower-cost authorization and faster settlement than traditional card flows. In Latin America, fast-payment systems are accelerating digital adoption across consumer and merchant segments, a shift that reduces friction and expands inclusion for underbanked groups that rely on wallets instead of cards.[2]Source: World Bank Authors, “Fast payments are driving digital transformation in Latin America and the Caribbean,” World Bank Blogs, blogs.worldbank.org Real-time rails enable immediate fund capture and support instant refunds during disruptions, improving trust and conversion for larger transactions. Cross-border expansion is underway as PagBrasil enables PIX payments for tourists and merchants with roaming and direct integrations for Argentine banks and wallets to scan QR codes and settle in local currency while merchants receive funds instantly. Wallet ecosystems in Brazil and across the region tie together stored balances, local acceptance, and installment options that align to travel use cases. As initiation services scale under open-finance frameworks, larger OTAs may partner with licensed providers rather than build from scratch, given compliance and security requirements that favor scale.

OTA Penetration And Super-App Ecosystems Expand Addressable Market

OTA penetration continues to expand as more travelers shift from offline to online booking channels, driven by growing smartphone adoption and faster internet connectivity. The rise of super-app ecosystems integrates travel services with payments, messaging, and loyalty programs, enabling OTAs to reach users in contexts beyond traditional travel search. These platforms lower barriers for first-time digital travelers by combining multiple services in a single interface, increasing convenience and driving higher booking frequency. Localized payment solutions, including instant payments and digital wallets, further enhance accessibility and reduce friction at checkout, boosting conversion rates. OTAs leveraging super-app partnerships can tap into embedded loyalty programs and cross-service promotions, enlarging the addressable market for both domestic and regional travel. Together, increasing OTA adoption and super-app integration allow online travel platforms to capture a broader, more engaged user base, particularly in high-growth markets like Brazil and Chile.

Airline Capacity Recovery And NDC Enable Richer Retailing

Latin America and the Caribbean carried 477.3 million passengers in 2025, up 3.8% year over year, with most net growth in intraregional routes that feed leisure and VFR demand through OTAs and supplier sites.[3]Source: ALTA Staff, “Air passenger traffic in Latin America and the Caribbean grew 3.8% in 2025,” ALTA, alta.aero. Financially stronger airlines expand premium products and sustain stable operations, while restructuring carriers improve liquidity and reset capacity plans, which collectively raises confidence among distributors. NDC adoption enables personalized bundles and dynamic offers that can lift yields, and agencies that integrate NDC content can access richer ancillaries and performance-aligned economics. Industry associations report strong air travel demand into 2026 alongside ongoing capacity constraints, which sustains pricing discipline in major markets.[4]Source: IATA Press Office, “Strong 2025 Passenger Demand Masks Ongoing Capacity Constraints,” IATA, iata.org. As NDC reaches greater share of bookings in South America, API-first distribution becomes standard practice for higher-margin retailing.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated fraud/chargebacks and dispute win-rate gaps | -0.9% | Brazil, Argentina; Brazil wins only 36.9% of chargebacks | Short term (≤ 2 years) |

| FX volatility and policy/tax headwinds on cross-border | -1.2% | Argentina core; Brazil real depreciation affects outbound | Medium term (2-4 years) |

| Parity/MFN enforcement shifts and regulatory scrutiny | -0.4% | Brazil pending legislation; Chile market study underway | Medium term (2-4 years) |

| Route/slot constraints and consolidation risk in air | -0.3% | Brazil domestic; airport infrastructure limits at hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Elevated Fraud And Chargeback Costs Compress Margins And Limit Scale

Travel merchants face the highest global average chargeback value among consumer sectors, and total costs per dispute can be several times the original transaction once fees and operational overhead are included. Industry groups also document rising attack volumes and describe friendly fraud as a dominant vector, which is particularly painful for high-ticket categories like flights and multi-day packages. Conversion suffers when authentication adds friction, yet the long-run payoff from tokenization, biometrics, and real-time alerts is lower dispute exposure and fewer write-offs. Larger OTAs deploy behavioral scoring and identity orchestration at scale, while smaller firms rely on third-party tools and must absorb higher unit costs for fraud management. The net effect is a direct drag on growth for the South America online travel market as resources shift from marketing and product to fraud containment.

FX Volatility Erodes Predictability And Distorts Regional Demand Flows

Currency swings across South America change relative prices for lodging, airfares, and packages, which reshapes inbound, outbound, and domestic travel flows within short windows. Brazil’s tourism receipts and visitor momentum improve when the real weakens, which lifts inbound demand and shifts Brazilian buyers toward domestic trips; this sensitivity aligns with issuer and network data on cross-border spending trends in the region. Hedging options remain limited for many travel firms, and working-capital gaps deepen when settlements and obligations sit in mismatched currencies. Consumers expect local-currency checkout, and multi-currency wallets grow, yet enterprise-scale instant settlement that reduces FX exposure is still uneven across markets. FX volatility therefore lowers forecasting visibility, complicates pricing, and can outweigh near-term gains from product or distribution improvements in the South America online travel market.

Segment Analysis

By Service Type: Transportation Dominates While Accommodation Growth Accelerates

Transportation accounted for 42.1% of bookings in 2025 and remains the largest segment across the South America online travel market, while accommodation is the fastest riser with a 5.93% CAGR projected through 2031 for the South America online travel market size. Airline capacity and punctuality metrics improved across the region in 2025, which supported reliable schedules and increased consumer confidence in booking flights through OTAs and supplier apps. Airlines with strong financials expanded premium offerings and delivered margin gains, while carriers exiting restructuring restored capacity and rebalanced networks that had previously constrained some origin and destination pairs. Bus-ticketing digitization added meaningful incremental supply, with new marketplace entrants using lower commissions, PIX acceptance, and app-based discovery to increase reach among value-focused travelers. Accommodation growth is accelerating as vacation rentals scale and boutique properties leverage OTAs for discovery, with Airbnb’s 2025 results signaling strong regional demand and a healthy host pipeline.

The economics of transportation in the South America online travel market reflect divergent airline balance sheets and content strategies, with NDC adoption enabling richer bundles that can improve conversion and ancillary attach rates for integrated distributors. OTAs deepen their mix of vacation packages to improve margins, while supplier-direct channels push loyalty to strengthen share of wallet. Bus aggregators invest in AI to personalize itineraries and drive conversion at lower basket sizes, extending digital travel’s reach into secondary corridors. Accommodation players promote flexible payments, including installments and instant pay, which aligns with wallet adoption and shortens checkout on mobile. Over the forecast, accommodation narrows the gap with transportation as more rentals, boutique inventory, and packaged experiences improve choice and value for travelers across the South America online travel market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Device Type: Mobile Ascendancy Reshapes Experience And Economics

Mobile held 69.2% of bookings in 2025 and is set to grow at a 6.1% CAGR through 2031, outpacing desktop as app-based loyalty, stored credentials, and one-tap instant payments become standard across the South America online travel market. App engagement improves unit economics through better repeat behavior and push-based reactivation, which reduces reliance on paid search and affiliates. Wallets and biometric authentication simplify checkout on mobile and expand access for underbanked users who do not hold credit cards but pay with instant rails or stored balances. Desktop retains a role in complex itineraries and corporate bookings, yet adaptive mobile design and embedded content tools continue to shift research and purchase to phones. Vacation rentals and last-minute stays see higher mobile conversion, supported by marketplace UX that lowers frictions and highlights flexible cancellation.

The trajectory favors mobile-first strategy in the South America online travel market as issuers and networks accelerate passkey and tokenization, which increase approvals and reduce fraud on smaller screens. Airlines also direct users into apps for day-of-travel services and seat upgrades, a pattern that lifts in-app monetization and loyalty participation. OTAs optimize cross-device continuity so research started on desktop can finish on mobile with stored preferences and saved searches. The long-run effect is a higher mobile share of the South America online travel market as platform leaders refine app funnels, deepen payments integration, and tailor content for shorter booking windows and impulse trips.

By Platform Type: OTAs Extend Lead Through Localized Payments And Loyalty

OTAs held 61.4% of platform bookings in 2025 and are projected to grow at a 6.4% CAGR through 2031, ahead of direct supplier channels that rise at 5.2% in the South America online travel market. Local payment acceptance remains a defining edge for OTAs because shoppers expect PIX, wallets, installments, and account-to-account initiation that many supplier-direct sites still lack. Loyalty scale and B2B distribution further widen the gap, as regional leaders combine consumer travel with white-label programs for banks, retailers, and airlines. Large OTAs also expand into platform services and AI assistants licensed to suppliers, a shift that creates non-transaction revenue streams and deeper integrations with hotel and airline partners.

Direct booking strategies center on loyalty, premium cabin differentiation, and enterprise travel tools, yet parity enforcement and search visibility can still favor OTA listings in many South American markets. NDC adds leverage to airlines that can withhold or surcharge legacy content, so OTAs with NDC access maintain product depth and richer ancillaries. Super-apps cross-sell travel to existing users with embedded wallets and credit, which raises competitive pressure on mid-tier OTAs. The likely outcome is continued OTA leadership in the South America online travel market as long as payment localization and loyalty programs remain ahead of supplier-direct capabilities, with future share shifts tied to regulatory outcomes on parity and conduct rules.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Brazil anchors the South America online travel market with 29.3% share in 2025 and the largest base of online buyers, supported by high urbanization and instant payments that simplify travel checkout. Air traffic data confirm continued passenger growth across Latin America and the Caribbean in 2025, which adds capacity and supports trip planning for both domestic and international segments. Brazil’s payment infrastructure accelerates mobile conversion and broadens inclusion, which reinforces online penetration as consumers adopt instant rails and wallets for larger purchases. Domestic bookings in Brazil benefit from reliable schedules and strong loyalty engagement, while inbound demand responds to relative price advantages during periods of real depreciation. Regulatory momentum on open finance and payment initiation also supports continued adoption of account-to-account flows in the South America online travel market.

Argentina records the fastest projected growth at a 5.88% CAGR through 2031 off a smaller 2025 base in the South America online travel market. The country’s future inbound recovery is linked to currency normalization that restores price competitiveness for foreign travelers. During 2025, outbound lifted due to currency dynamics and relative price signals, while inbound softened and average spend shifted lower in real terms. As currency policy evolves, a rapid rebound in inbound is plausible driven by iconic destinations, wine tourism, and adventure travel. Market participants monitor policy changes and payment rails to gauge demand and the timing of an inbound inflection in the South America online travel market.

Chile and Colombia each contribute mid-single digit shares to the South America online travel market and present steady demand profiles with strong leisure destinations and rising digital maturity. Chile’s open-finance rollout scheduled from 2026 can catalyze payment initiation for travel checkout and reduce merchant costs. Colombia benefits from rising international traffic into leisure hubs, while its super-app ecosystem showcases how embedded payments can cross-sell travel within multi-vertical platforms. Peru sits between 4% and 5% share with steady gains in 2025 and improved airport infrastructure that supports both domestic and international traffic. Secondary markets across Uruguay, Paraguay, Bolivia, Ecuador, Guyana, and Suriname collectively form a meaningful long tail that grows with better connectivity and payments adoption in the South America online travel market.

Competitive Landscape

The South America online travel market is experiencing moderate consolidation among leading players, while mid-tier OTAs remain fragmented and face increasing costs for compliance, fraud prevention, and customer acquisition. Global platforms maintain dominance through broad inventory, strong branding, and metasearch integration, whereas regional pure-plays compete by offering localized payments, omnichannel distribution, and B2B services. Despegar’s integration into a larger Latin portfolio demonstrates a strategy that leverages payments infrastructure, loyalty programs, and adjacent e-commerce audiences to drive synergies. Super-apps reduce marginal customer acquisition costs by bundling travel bookings with wallets and credit, creating pressure on mid-sized OTAs that lack captive user bases. Meanwhile, vacation rentals continue to grow in both inventory and demand, with Airbnb’s 2025 performance highlighting strong regional engagement and onboarding of new guests and hosts.

Strategy patterns in the market cluster into four main approaches. Platform leaders focus on optimizing their mix through loyalty programs and direct-to-consumer channels while investing in AI to improve search, service, and merchandising. Regional OTAs strengthen B2B distribution and add SaaS offerings to monetize technology for suppliers beyond traditional commissions. Super-apps integrate travel with payments and delivery services, using wallets and credit to simplify checkout and offer installment options. Niche disruptors target categories like intercity buses and tours, offering lower commissions and modern UX, relying heavily on mobile discovery and instant payments to capture market share.

Technology scale is a defining factor in competitive advantage. Leading OTAs deploy passkeys, tokenization, and real-time fraud detection, while smaller firms rely on partners with limited differentiation. Adoption of NDC content rewards platforms that integrate modern airline data and penalizes those using legacy feeds, as gaps in content and surcharges can reduce conversion. Mega-events create peak demand periods and fraud risk, emphasizing the need for scalable payment and risk management systems. Over the forecast period, consolidation is expected to continue at the market edges as firms seek scale benefits in payments, risk management, and regulatory compliance.

South America Online Travel Industry Leaders

Despegar.com Corp (includes Decolar brand)

Booking Holdings Inc. (Booking.com)

Airbnb, Inc.

CVC Corp

Expedia Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2026: Azul Linhas Aéreas Brasileiras exited Chapter 11 after raising USD 850 million in new equity, reducing debt and lease obligations by USD 2.5 billion, and lowering net leverage below 2.5x, while ruling out M&A to focus on organic growth.

- December 2025: PagBrasil and COELSA announced a partnership enabling 37 Argentine banks and wallets to integrate PIX and allow cross-border tourism payments with instant settlement and local-currency display for travelers paying in Brazil.

- December 2025: Trip.com Group introduced Trip Community a new integrated travel‑content ecosystem inside its apps that connects inspiration, planning, and booking into a unified user experience. The platform brings together travel content and creator‑generated insights with AI‑powered tools such as TripGenie and Trip.Planner to support end‑to‑end trip design, helping users plan, book, and share travel more seamlessly through the app experience.

- December 2025: Avianca received credit-rating upgrades from Moody’s and Fitch on the back of stronger liquidity, improved leverage, diversification via LifeMiles and cargo, and premium product expansion across new routes.

South America Online Travel Market Report Scope

The online travel market refers to travel and tourism company that plans travel plans for their customers online through a website or a mobile application. A complete background analysis of the Online Travel Market in South America, which includes an assessment of the emerging trends by segments, significant changes in market dynamics, and a market overview, is covered in the report. The Online Travel Market in South America is segmented by Service Type (Accommodation Booking, Travel Tickets Booking, Holiday Package Booking, and Other Services), By Mode of Booking (Direct Booking, and Travel Agents), By Booking Platform (Desktop, Mobile/Tablet), and by Geography (Mexico, Brazil, Argentina, and Rest of South America). The report offers market size and forecast values for the Online Travel Market in South America in USD billion for the above segments.

By Service Type

| Transporation |

| Accommodation |

| Vacation Packages |

| Others |

By Device Type

| Desktop |

| Mobile |

By Platform Type

| Direct Booking (Supplier-direct digital channels) |

| Online Travel Agencies (OTAs) |

By Country

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Others |

| By Service Type | Transporation |

| Accommodation | |

| Vacation Packages | |

| Others | |

| By Device Type | Desktop |

| Mobile | |

| By Platform Type | Direct Booking (Supplier-direct digital channels) |

| Online Travel Agencies (OTAs) | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Others |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size and growth outlook for the South America online travel market?

The South America online travel market size is USD 46.4 billion in 2025 and is projected to reach USD 65.40 billion by 2031 at a 5.81% CAGR.

Which platforms lead digital booking in South America?

OTAs lead with 61.4% of platform bookings in 2025 and are forecast to grow at a 6.4% CAGR through 2031, supported by localized payments and loyalty scale.

How fast is mobile expanding in South America’s digital travel?

Mobile captured 69.2% of transactions in 2025 and is growing at a 6.1% CAGR through 2031 as app-based checkout and instant payments reduce friction.

Which service category is growing the fastest?

Accommodation is the fastest-growing service category with a 5.93% CAGR projected through 2031, supported by vacation rentals and boutique hotel supply.

Which country contributes the largest share and which grows the fastest?

Brazil leads with 29.3% share in 2025, while Argentina posts the fastest projected growth at a 5.88% CAGR through 2031.