Online Travel Agency Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

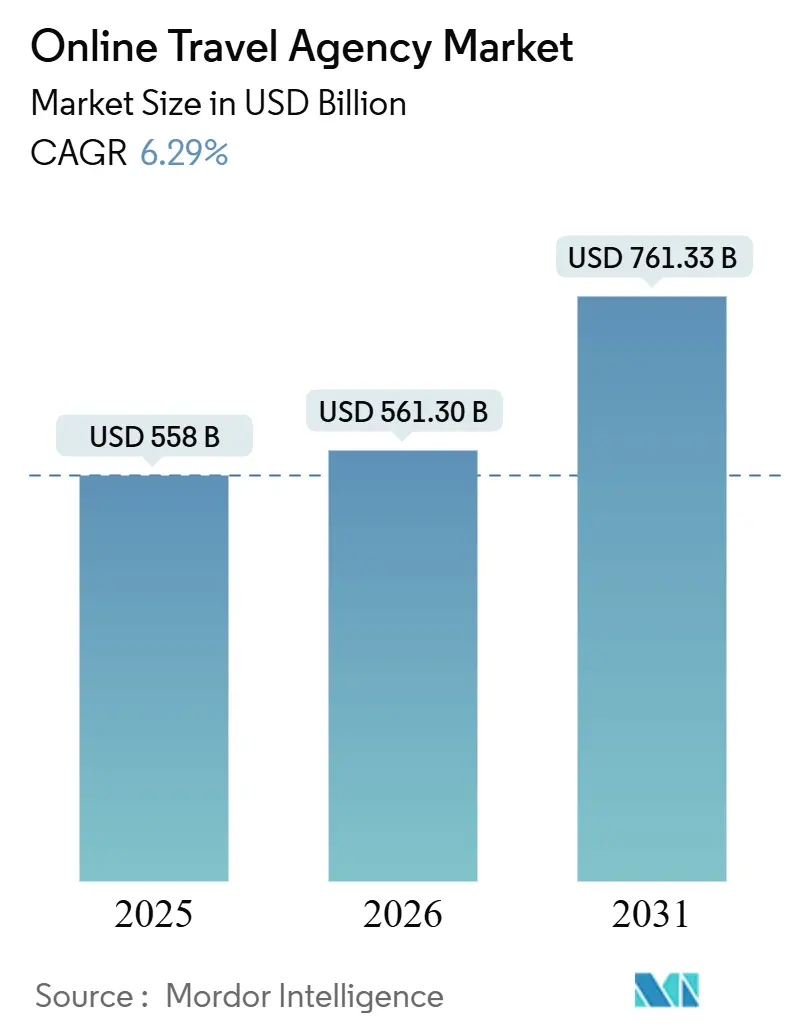

| Market Size (2026) | USD 561.30 Billion |

| Market Size (2031) | USD 761.33 Billion |

| Growth Rate (2026 - 2031) | 6.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Travel Agency Market Analysis by Mordor Intelligence

The online travel agency market size is USD 561.30 billion in 2026 and is projected to reach USD 761.33 billion by 2031 at a 6.29% CAGR. Travelers increasingly use digital channels for trip discovery, booking, and management, with mobile-first designs surpassing desktop interfaces. Mobile platforms gained significant transactional traffic by 2025, driven by biometric logins, offline itinerary access, and real-time alerts. Asia-Pacific led app-centric bookings, supported by superapp ecosystems integrating travel with payments, ride-hailing, and food delivery. Transportation dominates volumes, while accommodation grows rapidly due to alternative stays boosting inventory and margins. These trends shape strategies in the online travel agency market, aligning with ongoing upgrades in app infrastructure and embedded payment solutions.

Key Report Takeaways

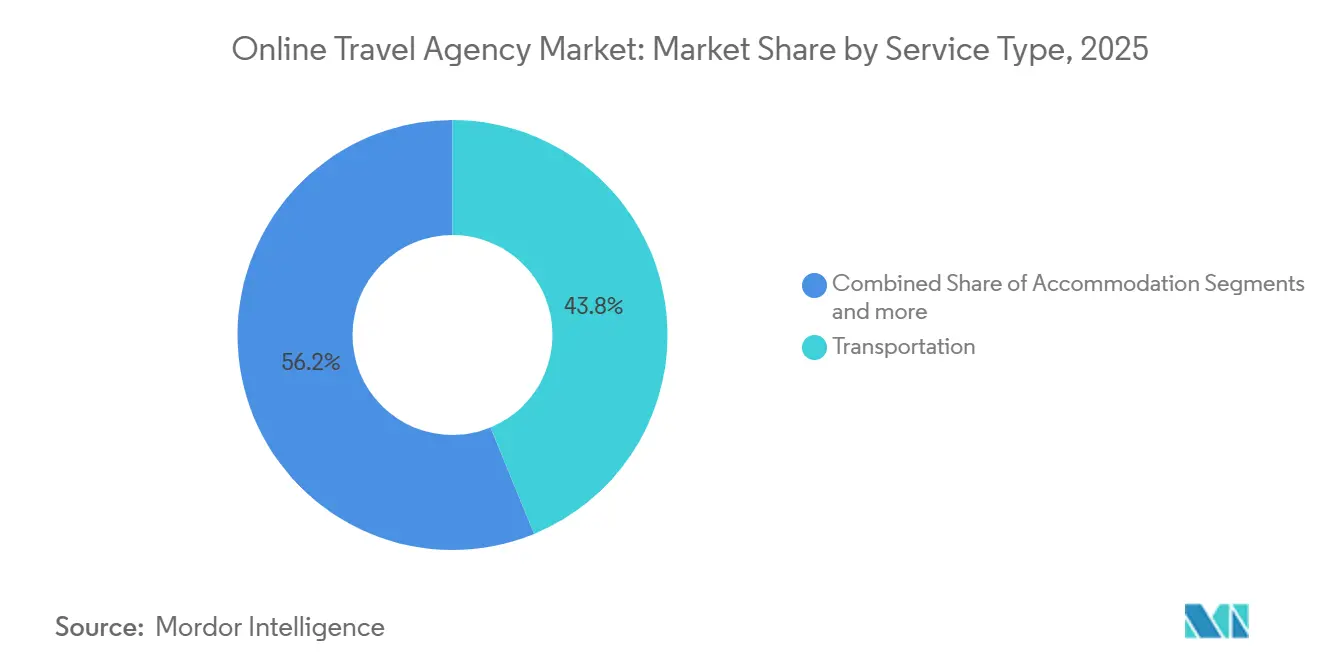

- By service type, transportation bookings held 43.8% of the Global Online Travel Agency Market share in 2025, while accommodation is forecast to expand at a 6.4% CAGR through 2031.

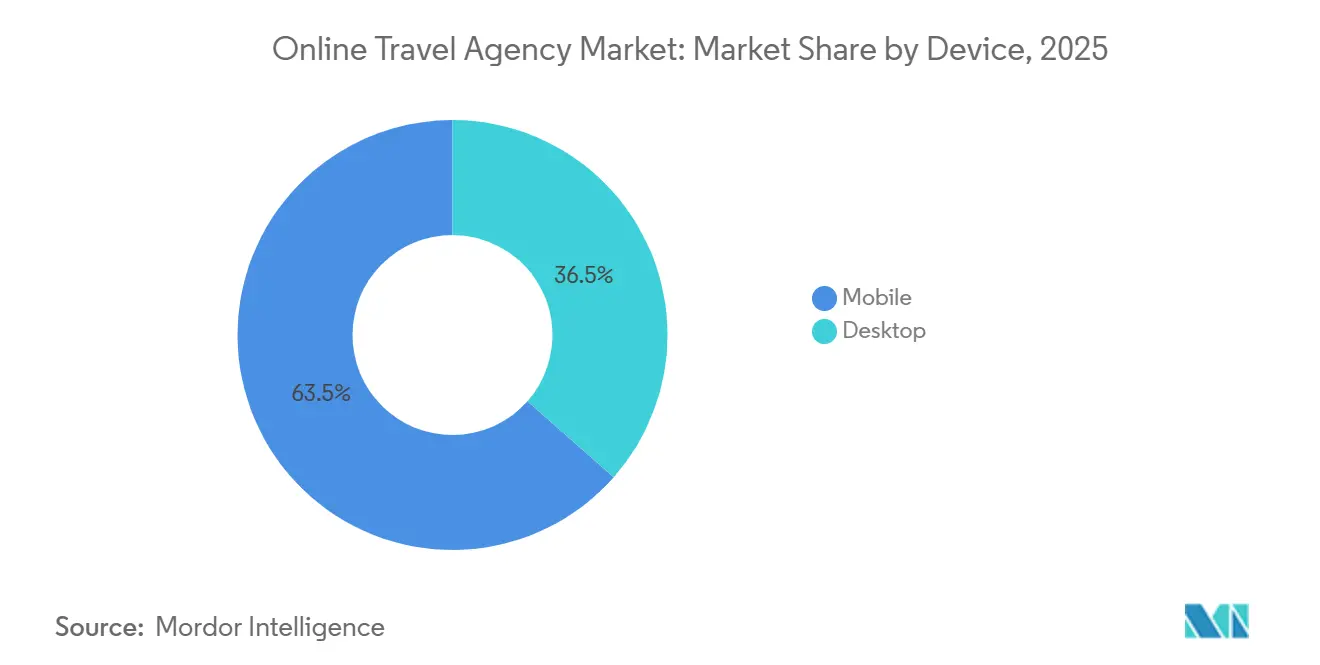

- By device, mobile captured 63.5% of the Global Online Travel Agency Market share in 2025, and is projected to grow at a 6.33% CAGR through 2031.

- By traveler type, leisure accounted for 77.7% of the Global Online Travel Agency Market share in 2025, while business is projected to grow at a 6.45% CAGR through 2031.

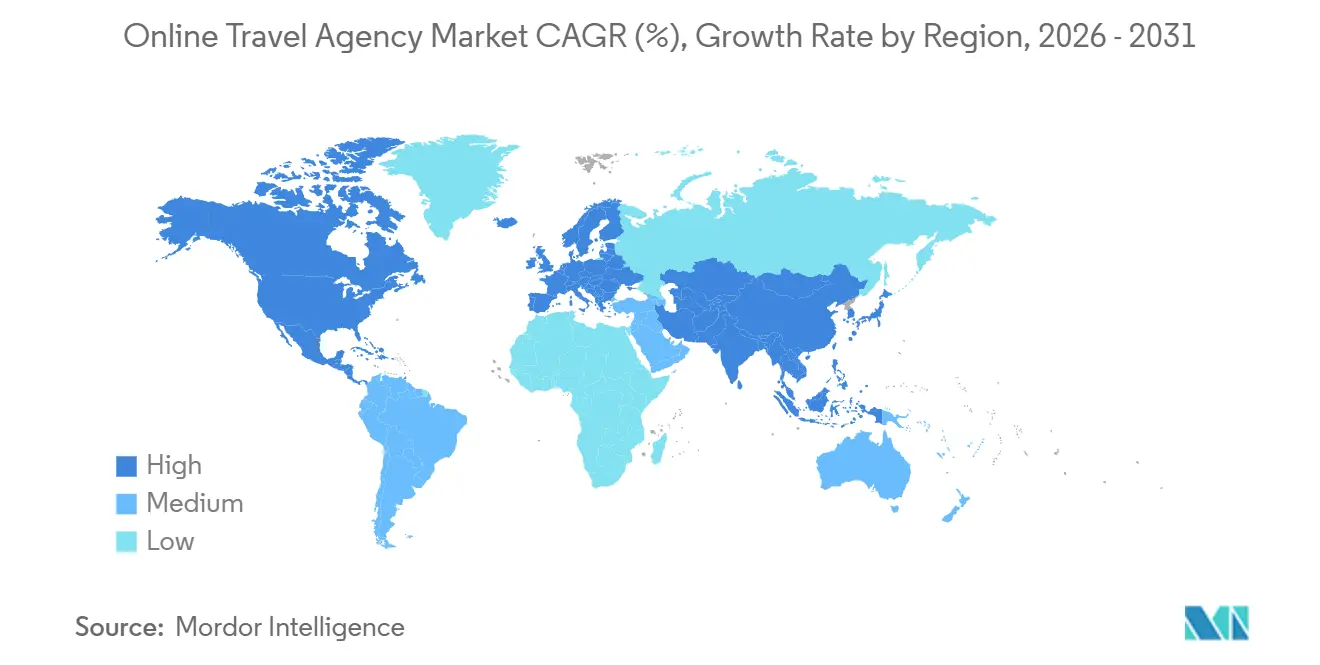

- By geography, Asia‑Pacific held 38.3% of the Global Online Travel Agency Market share in 2025, with the region forecast to expand at a 6.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Online Travel Agency Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mobile-first booking and app adoption | +1.2% | Global, strongest penetration in Asia-Pacific and accelerating in Middle East and Africa | Medium term (2-4 years) |

| International travel recovery and Asia-Pacific-led growth | +1.8% | Asia-Pacific core markets with spill-over to Europe destinations | Short term (≤ 2 years) |

| Embedded fintech and BNPL lift conversion and AOV | +0.9% | Europe and North America mature, expanding in Latin America | Medium term (2-4 years) |

| Airline NDC enables richer air retailing and ancillaries | +0.7% | Global, fastest adoption in Europe and North America corporate travel | Medium term (2-4 years) |

| Superapp and mini-program integrations expand OTA reach | +1.3% | Asia-Pacific dominance with early pilots in Southeast Asia and Latin America | Short term (≤ 2 years) |

| AI-powered personalization and dynamic pricing optimization | +1.1% | North America and Asia-Pacific early adopters, expanding in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mobile-first booking and app adoption

App-native booking functions are reshaping product roadmaps and cost structures in the online travel agency market. Airbnb reported that 64% of its Q4 2025 bookings were made via mobile apps, with mobile volumes growing double digits year-over-year as web traffic lagged. Trip.com Group stated that over 70% of its transactions originate on mobile devices, with higher conversion rates due to biometric checkout and real-time push alerts. Platforms now focus on real-time inventory accuracy, latency control, and dynamic repricing to capture intent quickly. In Southeast Asia, platforms such as Klook prioritize app experiences before extending features to web interfaces. Incumbents face a multi-year shift toward app-centric architectures to enhance booking and servicing operations[1]Whalesbook, “Airbnb’s India Surge Fuels Global Growth Amidst Margin Squeeze,” Whalesbook, whalesbook.com.

International travel recovery and Asia-Pacific-led growth

Asia-Pacific international arrivals reached 331 million in 2025, recovering to 92.6% of 2019 levels by January 2026. Outbound travel from China grew in 2025, while inbound and intra-Asia travel strengthened in Japan, South Korea, and Southeast Asia. India saw a sharp rise in booked nights on major platforms, highlighting the need for localized payments, loyalty, and content strategies. Trip.com Group reported strong international booking growth in Q3 2025, driven by inventory depth and regional supply-sharing relationships. Visa’s efforts in cross-border payment acceptance and localized checkout experiences underscore the importance of settlement infrastructure and risk control as key differentiators in the region’s online travel agency market expansion[2]OpenPR, “Asia Pacific Tourism Outlook 2026 2036: Market to Expand,” OpenPR, openpr.com.

Embedded fintech and BNPL lift conversion and AOV

Embedded payments are transforming booking conversions and cash flows in the online travel agency market. Airbnb introduced "Reserve Now Pay Later" in the United States during Q4 2025, achieving over 70% adoption among eligible bookings, highlighting the demand for flexible payment options. Fintech providers are shifting from flat-fee processing to value-based models tied to booking and basket size growth. Checkout processes now involve diverse providers, with installment plans, digital wallets, and local payment rails sequenced strategically. Strong fraud controls are essential, as card-not-present and cross-border flows pose risks that can erode payment margins if not managed with advanced tools. Payment strategies now drive growth and cost efficiency, with platforms reducing fraud losses and improving approval rates, gaining a competitive edge[3]AltexSoft, “Airbnb Expands Pay Later Worldwide for Peak Demand Bookings,” AltexSoft, altexsoft.com.

AI-powered personalization and dynamic pricing optimization

AI is transforming the online travel agency market by reducing service costs. Airbnb's AI-powered customer support autonomously resolves routine tasks, such as rebookings and check-in guidance, lowering per-contact costs compared to human-only workflows. Post-booking, intelligent assistants streamline tasks that typically require manual intervention. Regulated markets are adopting ISO 42001 AI management standards to ensure governance and human oversight in critical decisions. Early adopters are using AI for dynamic pricing and shopping optimization, where speed and relevance improve conversions and margins. These advancements are shifting AI from pilot features to scalable production systems, enhancing resilience and efficiency in the online travel agency market.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dependence on Google/AI search raises CAC volatility | -0.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Regulatory scrutiny and rate-parity bans (European Union DMA) | -0.6% | Europe core with precedent potential for Asia-Pacific | Medium term (2-4 years) |

| NDC-driven content fragmentation and servicing complexity | -0.5% | Global aviation distribution, most acute for multi-airline corporate bookings in North America and Europe | Medium term (2-4 years) |

| Rising fraud/chargebacks in cross-border payments | -0.4% | Global, highest impact in high-velocity cross-border corridors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Dependence on Google/AI search raises CAC volatility

AI-generated travel summaries on large search platforms are reducing clicks to OTA sites, creating budget uncertainties in performance channels for the online travel agency market. This impacts both cost per click and predictability, as model updates and UI changes occur more frequently than quarterly. Larger players are reallocating budgets from auction-based intent capture to brand-led awareness, boosting direct traffic. Smaller and mid-sized OTAs face challenges due to weaker brand search volumes and limited ability to outbid larger competitors. This dynamic creates a divide, with global platforms and niche providers maintaining steadier traffic funnels, while mid-market generalists experience increased pressure.

Regulatory scrutiny and rate-parity bans (European Union DMA)

The European Commission designated Booking.com as a gatekeeper under the Digital Markets Act in May 2024, introducing rules on parity clauses, data portability, and interoperability that impact contracts with hotels and suppliers. By August 2025, over 10,000 European hotels filed lawsuits, claiming best-price guarantees violated competition laws, complicating distribution agreements. DMA violations risk penalties of up to 10% of global turnover, pressuring compliance strategies. GDPR mandates require customers to export booking histories in machine-readable formats, increasing churn risk if competitors use this data for targeted offers. These regulations tighten operations in Europe and could inspire similar interventions in other regions over the medium term in the online travel agency market[4]The Guardian, “Thousands of Hotels in Europe to Sue Booking.com Over Abusive Practices,” The Guardian, theguardian.com.

Segment Analysis

By Service Type: Accommodation Gains as Air Bookings Fragment

Transportation bookings accounted for 43.8% of the online travel agency market share in 2025. Accommodation bookings are projected to grow at a 6.4% CAGR through 2031, driven by expanded alternative stays and improved cross-selling into packages. Supplier-side investments reflect this shift, with alternative accommodations scaling inventory and attracting longer-stay demand with better unit economics. Booking Holdings added 8.6 million alternative accommodation listings in 2025, an 8% year-over-year increase that supported higher-margin categories. Airlines’ New Distribution Capability adoption fragmented content across proprietary APIs, while look-to-book ratios above 1,000:1 in 2025 strained infrastructure and servicing costs for flight-only transactions. Platforms focusing on accommodations and experiences benefit from richer content, stronger margins, and improved loyalty engagement.

Flights remain critical for cross-selling. Booking.com processed 68 million flight bookings in 2025, a 37% year-over-year increase, though flights still represent a small portion of its room-night base, highlighting growth potential with better air content. Tours and activities are consolidating into branded marketplaces. Klook listed over 100,000 bookable experiences across 300+ destinations, capitalizing on experiential demand in leisure trips. IATA’s NDC framework advances content modernization, but servicing remains complex due to heterogeneity among 300+ airlines. Vertically integrated platforms combining supply, distribution, and payments mitigate these challenges, aligning with the market’s medium-term value concentration.

Note: Segment shares of all individual segments available upon report purchase

By Device: Mobile Supremacy Reshapes Platform Economics

Mobile devices accounted for 63.5% of OTA bookings in 2025, with the segment projected to grow at a 6.33% CAGR through 2031. Smartphones have become the primary interface in the online travel agency market. App-based transactions convert better than mobile web due to features like biometric authentication, offline receipts, and proactive alerts, which streamline processes and reduce abandonment. Trip.com Group reports over 70% of bookings from mobile, driven by app features that outperform mobile browsers in conversion rates. Asia-Pacific leads this trend, as many users first accessed the internet via smartphones, while desktops remain relevant for complex itineraries and corporate workflows. The focus is now on app performance, with desktops serving as a secondary research tool.

Desktops held a 36.5% share in 2025, supporting tasks like multi-city comparisons and policy reviews, but this share is declining as mobile platforms integrate enterprise-ready features. Corporate platforms such as Navan and TravelPerk incorporate expense capture and policy checks into mobile booking flows, reducing reliance on larger screens for routine trips. Progressive Web App standards from the World Wide Web Consortium provide app-like capabilities to mobile web experiences, bridging gaps where app installations are less common. Investments are expected to focus on load times, caching, and personalization on apps, directly impacting conversion rates and customer lifetime value.

By Traveler Type: Corporate Buyers Outpace Leisure Growth

Leisure travelers accounted for 77.7% of OTA bookings in 2025. Business travel is projected to grow at a 6.45% CAGR through 2031 as enterprises adopt self-service platforms with embedded expense and duty-of-care features. Global business travel spending reached USD 1.5 trillion in 2025, with a significant portion shifting to digital platforms that simplify booking while enforcing policies. Business travelers, who take multiple trips annually, require timely support for changes, reissues, and approvals. Platforms with advanced automation and 24/7 support are better positioned to meet these needs, enhancing satisfaction and retention. This trend is driving a shift toward enterprise-focused features in the online travel agency market.

Leisure demand dominates in volume but is more volatile across months and regions. The rise of "bleisure," where employees combine business and personal travel, highlights the need for diverse inventory to manage both in one workflow. Corporate sustainability rules, including the European Union’s Corporate Sustainability Reporting Directive requiring Scope 3 emissions reporting by 2026, are pushing companies to consolidate travel data on platforms with carbon APIs. Consumer-facing OTAs are adding B2B features, while TMCs are modernizing user experiences and mobile interfaces. These developments are increasing competition and driving more enterprise spending into the online travel agency market.

Geography Analysis

Asia-Pacific held 38.3% of the online travel agency market share in 2025 and is projected to grow at 6.8% through 2031, driven by mobile-first consumer behavior and superapp ecosystems integrating travel, payments, and mobility. International arrivals in the region reached 331 million in 2025, recovering to 92.6% of 2019 levels by January 2026. Payment localization and language support are critical in markets like India, Indonesia, and Vietnam, where app-native consumers demand flexible options and quick confirmations. Trip.com Group reported strong international booking growth through Q3 2025, supported by regional inventory partnerships and localized operations. Visa’s cross-border acceptance tools highlight the importance of aligning checkouts with local preferences to improve conversions.

North America and Europe accounted for a significant share of the global online travel agency market in 2025, with growth varying by corridor and policy environment. The United States experienced a 14% drop in international arrivals in March 2025 and a growing travel trade deficit, influencing marketing strategies for inbound tourism. Europe recorded 793 million international tourists in 2025, with high online booking penetration requiring differentiation beyond pricing. The DMA’s regulations on Booking.com add compliance challenges, potentially altering commission structures, data sharing, and parity clause enforcement in European Union markets. These changes emphasize the need for brand loyalty to reduce reliance on paid media.

The Middle East, Africa, and South America offer growth opportunities but require tailored strategies. Visa liberalization and destination investments in Gulf states drive demand, though online penetration remains below global averages, necessitating efforts in payment and language support. Currency volatility and inflation in South America increase the need for dynamic pricing, multi-currency transactions, and strong refund policies to maintain consumer confidence. Regional players integrate travel services into broader ecosystems like e-commerce, fostering trust and familiarity among new users. These strategies focus on value chain control and local credibility for sustainable growth.

Competitive Landscape

The online travel agency market has moderate concentration, with top global players expected to hold a significant share of gross bookings in 2025. Specialists and regional operators are focusing on niche segments. Accommodation booking often shows oligopoly traits, with platform brand equity driving direct traffic and partnerships. Booking Holdings and Airbnb maintain strong positions in accommodation due to consumer recall and broad property coverage. Flights and ground transportation remain fragmented because of airline direct channels and diverse local operators, creating opportunities for platforms that unify shopping, servicing, and payments. This structure emphasizes the need for high merchandising quality and app performance.

Strategic models in the market include horizontal super-app breadth, vertical depth, and embedded distribution. Trip.com Group demonstrates breadth by integrating flights, hotels, car rentals, and experiences with loyalty programs. Vertical specialists, such as GetYourGuide, expand through exclusive supplier relationships and curated content, including shows and events. Embedded travel grows as corporate platforms like Navan integrate expense management and duty-of-care systems, embedding travel into enterprise workflows. These strategies reduce reliance on auction-based traffic and encourage repeat purchases.

Market players continue to invest, partner, and acquire to enhance capabilities. Hopper’s fintech features, including price freeze and price-drop protection, generated significant fee revenue in 2025, highlighting the potential of ancillary services. Sabre’s NDC workflow solutions and agentic AI orchestration point to increased automation in shopping and servicing tasks. Expedia Group acquired Tiqets in December 2025 to strengthen tours and activities content and expand in-destination demand. Amex Global Business Travel acquired CWT in September 2025, consolidating B2B travel management and emphasizing enterprise-ready platforms. Compliance with ISO 42001’s AI management framework has become a trust marker in regulated regions, differentiating mature platforms in procurement processes.

Online Travel Agency Industry Leaders

Booking Holdings (Booking.com, Priceline, Agoda)

Navan (Reed & Mackay, Comtravo, Resia, Atlanta Events & Corporate Travel Consultants)

Perk (Formerly TravelPerk)

Expedia Group (Expedia, Hotels.com, Vrbo)

Klook

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Airbnb reported 121.9 million nights booked in Q4 2025. It launched the "Reserve Now, Pay Later" feature in the U.S., which saw over 70% adoption for eligible bookings. This initiative aims to increase access to higher-value bookings.

- January 2026: BCD Travel and Delta Air Lines have established a long-term strategic partnership to integrate Delta's content directly into BCD's corporate booking platform. This collaboration reflects the increasing adoption of direct distribution methods in the corporate travel market.

- January 2026: The State Administration for Market Regulation in China initiated an antitrust investigation into Trip.com Group. The probe examines merchant exclusivity and ranking practices, creating regulatory uncertainty for Asia's largest OTA platform.

- December 2025: Expedia Group has acquired Tiqets to enhance its activities vertical and improve access to experiential content for users, aiming to diversify its offerings and strengthen its position in the market.

Global Online Travel Agency Market Report Scope

The Global Online Travel Agency Industry report explores the digital travel ecosystem, including accommodations, transportation, vacation packages, and services booked via OTAs. The market is segmented by service type, device (desktop, mobile), traveler type (leisure, business), and geography (North America, South America, Asia‑Pacific, Europe, Middle East & Africa). It examines drivers such as mobile‑first bookings, international travel recovery, embedded fintech, NDC‑enabled air retailing, superapp integrations, and AI personalization, alongside challenges including CAC volatility, regulatory scrutiny, content fragmentation, and fraud risks. Porter’s Five Forces framework evaluates the regulatory landscape, technology trends, supply chain, and competition. The report includes market size, growth forecasts, company profiles, strategic developments, and future opportunities, identifying unmet needs. The report provides market size and forecasts for the Global Online Travel Agency Market, in value (USD), for the above segments.

| Accommodation (Hotels, Alternative Accommodations) |

| Transportation |

| Vacation Packages |

| Others |

| Desktop |

| Mobile |

| Leisure Travelers |

| Business Travelers |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Service Type | Accommodation (Hotels, Alternative Accommodations) | |

| Transportation | ||

| Vacation Packages | ||

| Others | ||

| By Device | Desktop | |

| Mobile | ||

| By Traveler Type | Leisure Travelers | |

| Business Travelers | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and five-year outlook for the global online travel agency market?

The online travel agency market size is USD 561.30 billion in 2026 and it is projected to reach USD 761.33 billion by 2031 at a 6.29% CAGR.

Which service types are setting the growth pace in the online travel agency market?

Transportation holds the largest share at 43.8% in 2025, while accommodation leads growth with a 6.4% CAGR projected through 2031.

How fast is mobile expanding in the online travel agency market?

Mobile captured 63.5% of bookings in 2025 and is projected to grow at a 6.33% CAGR through 2031, supported by app-native features and faster checkout.

What regions contribute most to growth in the online travel agency market?

Asia-Pacific held 38.3% in 2025 and is forecast at 6.8% CAGR through 2031, aided by superapp ecosystems and localized payments.

How will regulation in Europe affect the online travel agency market?

The EU Digital Markets Act imposes obligations on large platforms and could reshape parity and data portability, increasing compliance requirements and altering commission dynamics.

What role will embedded fintech play in the online travel agency market over the next few years?

Flexible payments like installment plans improve conversion while also requiring tighter fraud controls, as seen in the strong adoption of Reserve Now Pay Later on Airbnb for eligible bookings.