Metal Precision Turned Product Manufacturing Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

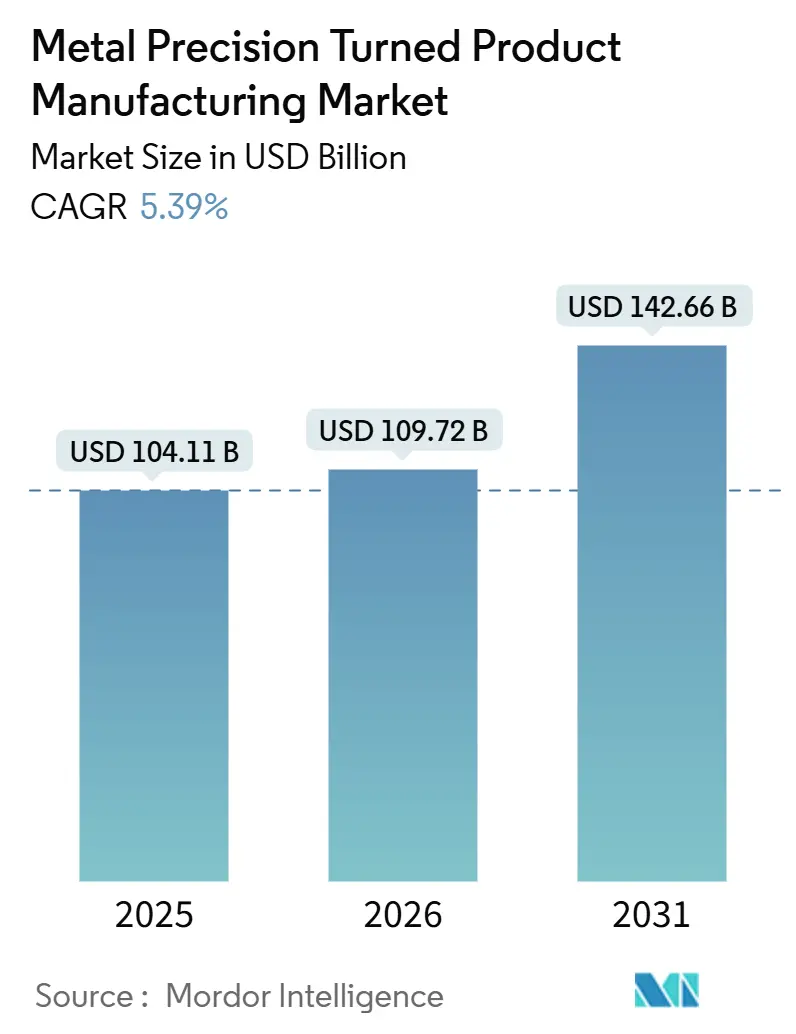

| Market Size (2026) | USD 109.72 Billion |

| Market Size (2031) | USD 142.66 Billion |

| Growth Rate (2026 - 2031) | 5.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Metal Precision Turned Product Manufacturing Market Analysis by Mordor Intelligence

The metal precision turned product manufacturing market size is projected to grow from USD 104.11 billion in 2025 to USD 109.72 billion in 2026 and is forecast to reach USD 142.66 billion by 2031, registering a CAGR of 5.39% between 2026 and 2031. Rising vehicle electrification, recovering commercial-aircraft build rates, and the miniaturization of orthopedic and dental implants are together tightening tolerance bands and shortening cycle-time expectations across the metal-precision-turned product manufacturing market. As battery-electric platforms replace traditional ferrous power-train components, the demand for lightweight aluminum and copper alloys is increasing. Concurrently, aerospace giants are reviving previously dormant production lines, now favoring nickel- and titanium-based alloys. Hospitals are expanding orders for small implant screws, pushing suppliers to transition from standard chucking lathes to precision Swiss-type machines capable of holding extremely tight tolerances. In the metal precision turned product manufacturing arena, automation and in-process metrology have become the benchmarks of competitiveness, narrowing the performance divide between Tier-1 precision shops and their smaller regional counterparts.

Key Report Takeaways

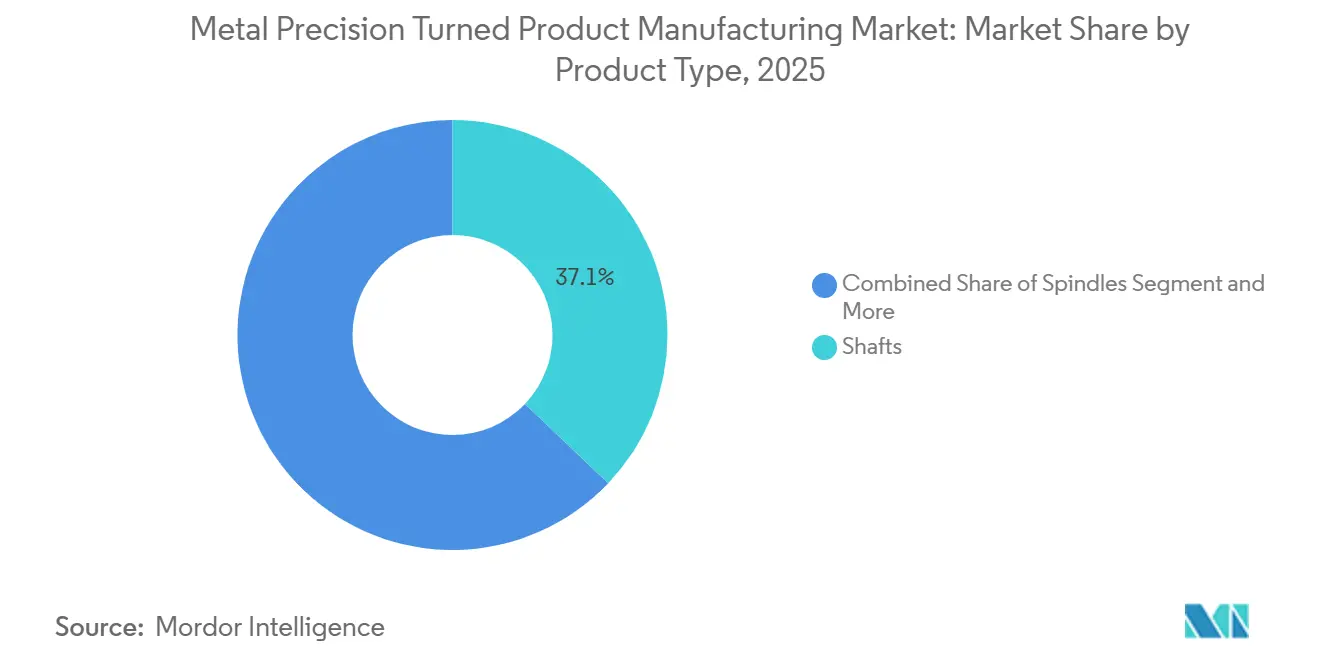

- By product type, shafts led with 37.11% of the metal precision turned product manufacturing market share in 2025, while couplings are projected to expand at a 7.81% CAGR through 2031.

- By material, steel dominated the metal precision turned product manufacturing market, accounting for 43.22% of the market size in 2025, and aluminum is advancing at a 6.78% CAGR through 2031.

- By process, CNC turning commanded 61.76% of the metal-precision turned product manufacturing market in 2025, whereas Swiss-type turning is on track for a 7.93% CAGR through 2031.

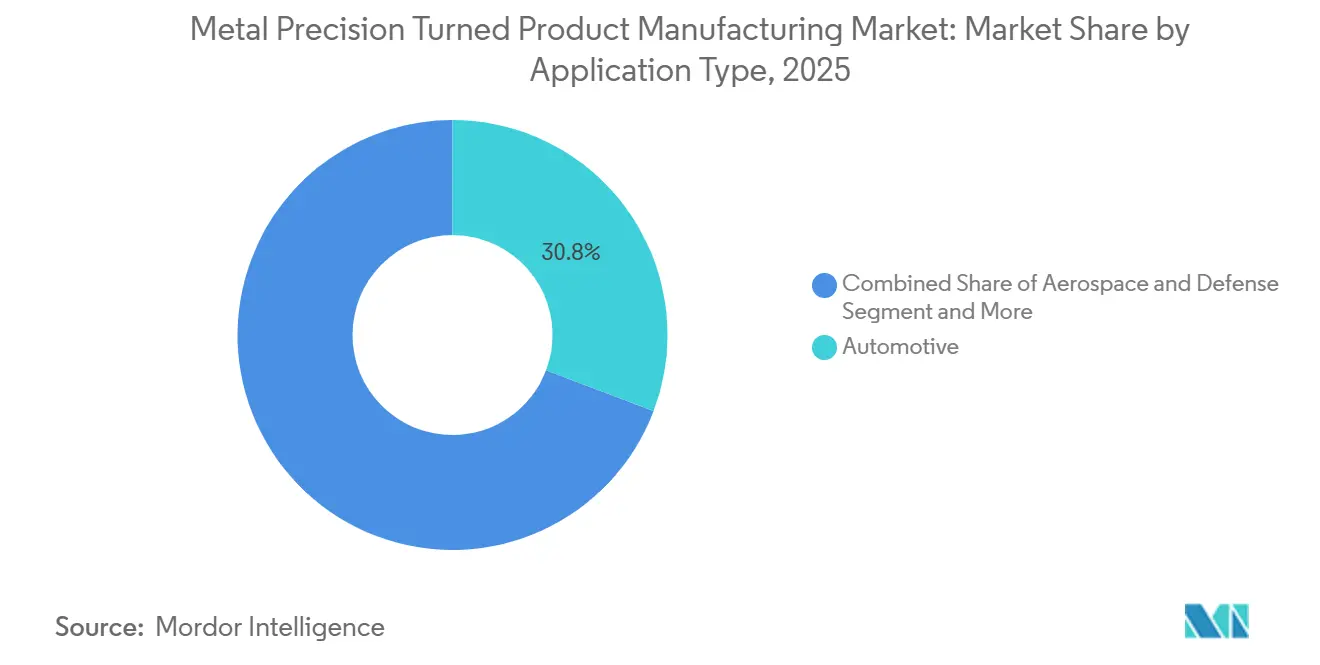

- By application, automotive accounted for 30.75% of the metal precision turned product manufacturing market share in 2025; medical devices recorded the fastest growth at an 8.11% CAGR through 2031.

- By sales channel, OEM direct procurement accounted for 73.44% of the metal precision turned product manufacturing market share in 2025, with a forecast CAGR of 7.29% through 2031.

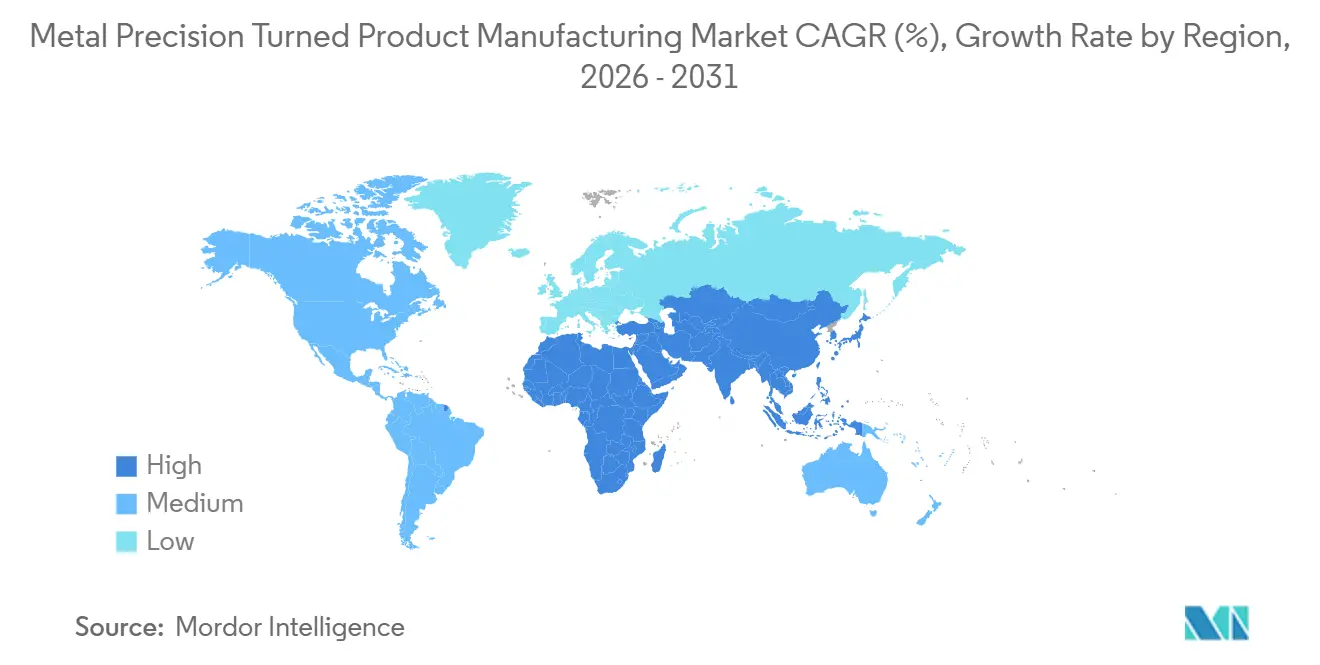

- By geography, Asia-Pacific accounted for 46.34% of the metal precision turned product manufacturing market share in 2025 and is growing at a 7.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Metal Precision Turned Product Manufacturing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timline |

|---|---|---|---|

| EV Power-Train Lightweight Precision Demand | +1.2% | Global, with concentration in China, EU, North America | Medium term (2-4 years) |

| Industry 4.0-Enabled Multi-Axis CNC Adoption | +1.0% | APAC core, spill-over to North America and EU | Long term (≥ 4 years) |

| Aerospace Build-Rate and MRO Surge | +0.9% | North America, Europe, Middle East | Medium term (2-4 years) |

| Micro-Implant Swiss-Turning Boom | +0.8% | North America, EU, Japan | Long term (≥ 4 years) |

| OEM Regional Supplier-Park Localisation | +0.7% | Mexico, Vietnam, India, Central Europe | Short term (≤ 2 years) |

| On-Machine Real-Time Metrology and Adaptive Control Adoption | +0.6% | Global, early adoption in aerospace and medical hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EV Power-Train Lightweight Precision Demand

As automakers in the European Union aimed to meet stricter CO₂ emission thresholds, the aluminum content in light vehicles increased significantly [1]“CO₂ Emissions Regulation,” European Commission, ec.europa.eu. In the same period, China experienced a substantial rise in the production of battery-electric and plug-in hybrid vehicles, driving higher demand for aluminum heat-sink pins and copper busbars. Tesla's giga-casting approach reduced the number of parts but concentrated precision machining on fewer, larger aluminum nodes, requiring post-cast boring with high precision. Accelerated tool wear on non-ferrous alloys is prompting Tier-2 shops to adopt ceramic inserts and through-spindle coolant, which significantly extends tool life. These trends are collectively boosting demand for high-speed CNC cells in the metal-precision-turned product manufacturing sector.

Industry 4.0-Enabled Multi-Axis CNC Adoption

Yamazaki Mazak revealed that a significant portion of its shipments featured automation-ready robot interfaces. These interfaces facilitate overnight "lights-out" operations, effectively doubling the spindle hours. Meanwhile, a German power-train supplier successfully reduced its unplanned downtime by integrating digital twins with predictive bearing analytics. Multi-axis turning centers, now capable of simultaneous multi-axis operation, can finish turbine-blade roots or orthopedic hip stems in a single setup, thereby eliminating cumulative tolerance stack-up. Japan's machine-tool output in NC lathes achieved a notable penetration rate, indicating a near-total shift to programmable platforms. Furthermore, adaptive CAM software, which adjusts feeds and speeds in real-time, is achieving a significant reduction in cycle times for Inconel 718 and Ti-6Al-4V programs.

Aerospace Build-Rate and MRO Surge

Commercial aircraft backlogs reached a significant level, while global spending on engine maintenance, repair, and overhaul (MRO) grew substantially. GKN Aerospace's new facility in San Diego, funded by a significant investment, sparked a surge in demand for NADCAP-qualified titanium turnings. ST Engineering expanded its overhaul capacity to handle more engines annually, leading to increased demand for high-precision valve bodies. NATO members increased their defense budgets, directing a significant portion toward fighter sustainment, which relies on components such as hydraulic bushings, actuator pins, and avionics mounts. The AS9100 standard, adopted by many suppliers worldwide, requires a rigorous documentation process. While this safeguards established precision shops, it also necessitates ongoing investments in metrology.

Micro-Implant Swiss-Turning Boom

Globally, hip replacement procedures are performed in significant volumes, each utilizing multiple titanium or PEEK screws crafted on advanced Swiss-type machines. These lathes, designed to feed bar stock through a guide bushing, employ dual turrets for simultaneous cutting, effectively reducing cycle times for smaller parts. The United States and Swiss contract manufacturers, recognizing the demand, have been installing Star Micronics and Citizen cells at a steady pace, catering specifically to minimally invasive instrument lines. While patient-specific implants are produced using additive manufacturing methods, they still depend on subtractive Swiss turning to achieve final dimensional accuracy and deburring. The medical devices sector is experiencing consistent growth, driven by factors such as reimbursement models and an aging population, which outweigh the challenges posed by high alloy-qualification costs in the metal-precision turned product manufacturing market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Steel and Brass Pricing | -0.8% | Global, acute in import-dependent regions | Short term (≤ 2 years) |

| Skilled CNC Machinist Shortage | -0.7% | North America, EU, Japan | Long term (≥ 4 years) |

| Qualification Costs For Exotic Alloys | -0.5% | Aerospace and medical hubs in North America, EU | Medium term (2-4 years) |

| Rising Electricity Prices For High-Speed Machining Operations | -0.4% | EU, select APAC markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Steel and Brass Pricing

Aluminum prices increased over the period and are expected to remain steady in the near future, constrained by limited supply flexibility amid high energy costs in the EU and production restrictions in China. Copper prices have risen sharply and are expected to continue rising, driven by increasing demand for electric vehicle cables. The United States imposed substantial tariffs on certain copper imports, prompting Midwest shops to source from Canada at a premium. In the metal-precision turned product manufacturing market, brass-focused job shops without pass-through clauses are facing challenges as rising copper and zinc prices strain working capital and reduce profit margins.

Skilled CNC Machinist Shortage

More than half of North American fabricators are struggling to fill open CNC operator positions, and the median age of machinists continues to rise. The U.S. Bureau of Labor Statistics highlights a significant shortage of manufacturing jobs, particularly in CNC roles. To attract scarce talent, German Mittelstand firms are offering incentives such as signing bonuses and shorter workweeks. In Japan, initiatives are being implemented to train young operators, but retirements still outpace new entrants. While robots handle loading tasks, intricate first-piece setups remain reliant on human expertise, limiting the potential for substitution in the metal-precision turned product manufacturing sector.

Segment Analysis

By Product Type: Shafts Lead, Couplings Accelerate

Shafts accounted for 37.11% of the metal-precision turned product manufacturing market share in 2025. High-rpm electric-motor designs spinning 15,000-20,000 rpm now demand ultra-fine surface finishes to avert bearing failures, pushing shops toward diamond-impregnated honing stones and in-machine balancing. Couplings, although smaller in absolute volume, are forecast to expand their revenue base at a 7.81% CAGR as warehouse automation and collaborative robots require zero-backlash torque transmission. Suppliers command price premiums by using sensor-embedded couplings that report vibrational signatures.

While commoditized nuts, bolts, and bushings are sensitive to price fluctuations, aerospace fasteners made from A286 stainless steel or Inconel maintain their margins, thanks to their NADCAP pedigree. Multi-spindle screw machines dominate high-volume contracts for automotive nuts. Meanwhile, flexible CNC platforms are replacing cam-driven legacy assets for medium-volume runs. In the realm of metal precision turned product manufacturing, as EV powertrains reduce part counts, shafts and couplings remain strategically important because they transmit torque between electric motors and final-drive reducers.

Note: Segment shares of all individual segments available upon report purchase

By Material: Steel Dominates, Aluminum Gains

Steel accounted for 43.22% of the metal-precision turned product manufacturing market share in 2025, yet aluminum’s 6.78% CAGR is the fastest path to volume accretion. The aluminum content of battery-electric cars has increased significantly over time. Stainless steel grades, such as 304 and 316L, dominate niches like implants, food processing, and marine applications due to their corrosion resistance, which enables them to command premium pricing. Brass continues to hold its position in low-voltage connectors due to its excellent machinability and electrical conductivity, despite fluctuations in commodity prices. Exotic alloys, including titanium, Inconel, and PEEK, account for a small share of total tonnage but represent a substantial share of market value. This emphasizes the high revenue per unit weight driven by the aerospace and medical sectors within the metal precision turned product manufacturing market.

Machining economics vary significantly. For example, Ti-6Al-4V is machined at a much slower speed compared to aluminum and requires flood coolant to prevent work hardening, which increases production costs. Similarly, PEEK polymer screws have a rotational speed limit to avoid melting, which extends production times. However, these screws command significantly higher prices than their stainless steel counterparts.

By Process: CNC Turning Leads, Swiss-Type Surges

CNC turning accounted for 61.76% of the metal-precision turned product manufacturing market share in 2025, reflecting its diameter range of 5 to 500 millimeters. However, Swiss-type lathes are slated for a 7.93% CAGR on the back of miniature medical screws and electronic connector pins that comprise growing portions of the Metal precision turned product manufacturing market. Automatic cam-driven machines secure substantial contracts for automotive bolts, achieving extremely short cycle times. Multi-spindle CNCs are driving economies of scale in EV battery fittings, significantly reducing per-part costs for large production orders.

With Japan showcasing widespread adoption of NC technology, the era of manual lathes seems to be waning. Even in Germany, the multi-spindle sector is shifting towards servo-indexing, drastically cutting changeover times. The Swiss-type machine's ability to complete tasks in one go minimizes tolerance stack-ups, offering a competitive advantage in producing orthopedic stems and turbine metering nozzles within the precision turned product manufacturing arena.

By Application: Automotive Largest, Medical Fastest

Automotive accounted for 30.75% of the metal-precision turned product manufacturing market share in 2025, with shafts, suspension bushings, and motor housings making up the bulk of the order book. Medical devices lead the growth chart, with an 8.11% CAGR through 2031, driven by an aging population that is driving annual implant procedures and hip replacements.

Backed by order backlogs and MRO cycles, the aerospace and defense sectors experience consistent growth. These gains are further supported by gatekeepers such as NADCAP and AS9100, which tend to favor established suppliers in the metal-precision-turned-products manufacturing industry. Meanwhile, industrial machinery and construction equipment maintain stable demand, driven by replacement demand. In the electronics sector, the reliance on brass and copper micro pins has positioned Swiss cells as a key player.

Note: Segment shares of all individual segments available upon report purchase

By Sales Channel: OEMs Dominate Direct Procurement

OEM call-offs accounted for 73.44% of the metal-precision turned product manufacturing market share in 2025, and the model is forecast to deliver a 7.29% CAGR as co-located supplier parks minimize logistics lag. Automotive Tier-1s are securing vendor rosters from multiple shops and conducting annual audits for PPAP compliance, a move that solidifies longer engagement cycles.

Aerospace primes intensify this approach with multi-year, take-or-pay contracts. StandardAero's significant surge in component-repair receipts underscores the aftermarket's resilience. However, overall volumes are more closely linked to the installed base than to new production. As a result, OEM channels will continue to influence both volume and technology roadmaps in the metal precision turned product manufacturing market.

Geography Analysis

Asia-Pacific captured 46.34% of the metal-precision turned product manufacturing market share in 2025 and is projected to grow at a 7.89% CAGR through 2031, as China remains a leading producer of vehicles, while India continues to experience significant annual growth in precision-machining capacity [2]“Production Report 2025,” China Association of Automobile Manufacturers, caam.org.cn. In Chennai, Tsugami's complex highlights Japan's approach of co-locating foundry and finish-machining operations to meet India's domestic demand. South Korea's supply to Samsung and Hyundai ensures steady local demand for high-volume connectors and fasteners. Meanwhile, Vietnam's substantial FDI inflow is channeling brass and stainless steel turnings to global electronics brands. Thailand and Indonesia are emerging as auxiliary "China+1" nodes to address excess demand driven by rising labor costs in China.

North America and Europe, while growing steadily, maintain dominance, holding the majority of NADCAP and ISO certifications, particularly in the aerospace and medical sectors. Mexico's significant FDI investments are strengthening Bajío parks, ensuring timely shipments to U.S. assembly plants in line with USMCA regulations. Germany's machine tool exports include a notable share of precision turning centers for aerospace and automation applications. The U.K.'s Viking Precision has optimized a new production cell for the continuous manufacturing of titanium MRO parts.

Although South America, the Middle East, and Africa are smaller players, they are gaining momentum, particularly in mining and energy. Brazil's São Paulo cluster supports local OEMs. In the Middle East, both the UAE and Saudi Arabia are developing aerospace MRO hubs, though they currently rely on European imports. South Africa's mining sector, requiring large-diameter steel shafts, is sourcing them locally, significantly reducing lead times compared to imports. Turkey is leveraging its customs-union access to the EU, focusing on automotive and appliance parts, and benefiting from the established subcontractor networks in Istanbul and Bursa. This division—volume concentrated in Asia-Pacific and value in the West—appears set to continue in the metal-precision-turned-product manufacturing market.

Competitive Landscape

A small group of global suppliers captures a significant share of market revenue, leaving numerous regional specialists to address the remaining demand. Machine-tool OEMs, including DMG Mori, Mazak, Okuma, Citizen, and Tsugami, are advancing capabilities by incorporating automation features and metrology ports. Precision Castparts, supported by Berkshire Capital and recognized for its NADCAP certification, sets premium prices for nickel and titanium parts, positioning them above market averages.

GKN Aerospace’s MRO line in San Diego generates demand streams that smaller job shops cannot compete with. At the same time, Indian and Vietnamese companies, benefiting from lower labor costs and ISO 9001 certifications, are capturing Tier-2 auto contracts previously dominated by North America and the EU. Technology remains the critical differentiator: Users of Renishaw and Blum-Novotest probes report significant reductions in scrap, while competitors without probes face challenges in maintaining margins at similar price levels. DMG Mori is focusing on reducing cycle times through real-time digital twins, with plans to establish a research hub at the University of Tokyo. The private-equity market is highly active, particularly in aerospace and medical platforms, which are attracting high EBITDA multiples due to their stable contracts and regulatory advantages in the metal-precision product manufacturing industry.

Metal Precision Turned Product Manufacturing Industry Leaders

E&H Precision (Thailand) Co., Ltd.

Precision Castparts Corp.

NINGBO JH Metal Technology Co.,Ltd.

Suzhou Cheersson Precision Industry Group Co., Ltd.

PennAero

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: PrecisionX Group, a top provider of precision metal components for critical applications, has launched its 3D Design Hub on its website. This digital platform gives engineers instant access to CAD drawings for over 15,000 standard deep-drawn components, featuring detailed technical specifications and fully editable models.

- July 2025: PMGC Holdings Inc. completed the acquisition of AGA Precision Systems LLC, a specialized CNC machining business based in California. The acquired entity is renowned for its high-tolerance milling, turning, and mold manufacturing capabilities, particularly for complex metals such as titanium and Inconel, serving the aerospace and defense sectors.

Global Metal Precision Turned Product Manufacturing Market Report Scope

The metal precision turned product manufacturing market report is segmented by product type (shafts, spindles, bushings, fasteners, couplings, nuts and bolts, and others), material (steel, stainless steel, brass, aluminum, copper, and others), process (CNC turning, automatic turning, swiss-type turning, and multi-spindle turning), application (automotive, aerospace and defense, industrial machinery, electrical and electronics, medical devices, construction equipment, and others), sales channel (OEMs and aftermarket), and geography (North America, South America, Europe, Asia-Pacific, and Middle-East and Africa). The market forecasts are provided in terms of value (USD).

| Shafts |

| Spindles |

| Bushings |

| Fasteners |

| Couplings |

| Nuts and Bolts |

| Others (Pins, Connectors) |

| Steel |

| Stainless Steel |

| Brass |

| Aluminum |

| Copper |

| Others (Alloys, Specialty Metals) |

| CNC Turning |

| Automatic Turning |

| Swiss-Type Turning |

| Multi-Spindle Turning |

| Automotive |

| Aerospace and Defense |

| Industrial Machinery |

| Electrical and Electronics |

| Medical Devices |

| Construction Equipment |

| Others |

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Shafts | |

| Spindles | ||

| Bushings | ||

| Fasteners | ||

| Couplings | ||

| Nuts and Bolts | ||

| Others (Pins, Connectors) | ||

| By Material | Steel | |

| Stainless Steel | ||

| Brass | ||

| Aluminum | ||

| Copper | ||

| Others (Alloys, Specialty Metals) | ||

| By Process | CNC Turning | |

| Automatic Turning | ||

| Swiss-Type Turning | ||

| Multi-Spindle Turning | ||

| By Application | Automotive | |

| Aerospace and Defense | ||

| Industrial Machinery | ||

| Electrical and Electronics | ||

| Medical Devices | ||

| Construction Equipment | ||

| Others | ||

| By Sales Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Metal precision turned product manufacturing market in 2031?

It is expected to reach USD 142.66 billion by 2031, reflecting a 5.39% CAGR from 2026 to 2031.

Which region is expanding fastest within the Metal precision turned product manufacturing market?

Asia-Pacific is registering a 7.89% CAGR, driven by Chinese EV volumes and Indian capacity additions.

Which application segment shows the highest growth rate?

Medical devices are advancing at an 8.11% CAGR through 2031 as implant volumes rise.

Why are Swiss-type turning machines gaining share?

They achieve precise tolerances while machining small parts, significantly reducing the cutting cycle time for implants and electronic connectors.

How are raw-material price swings affecting suppliers?

Shops without pass-through clauses are facing challenges as fluctuations in aluminum, copper, and brass prices impact their growth projections.