Luxury Vinyl Tile Floor Covering Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

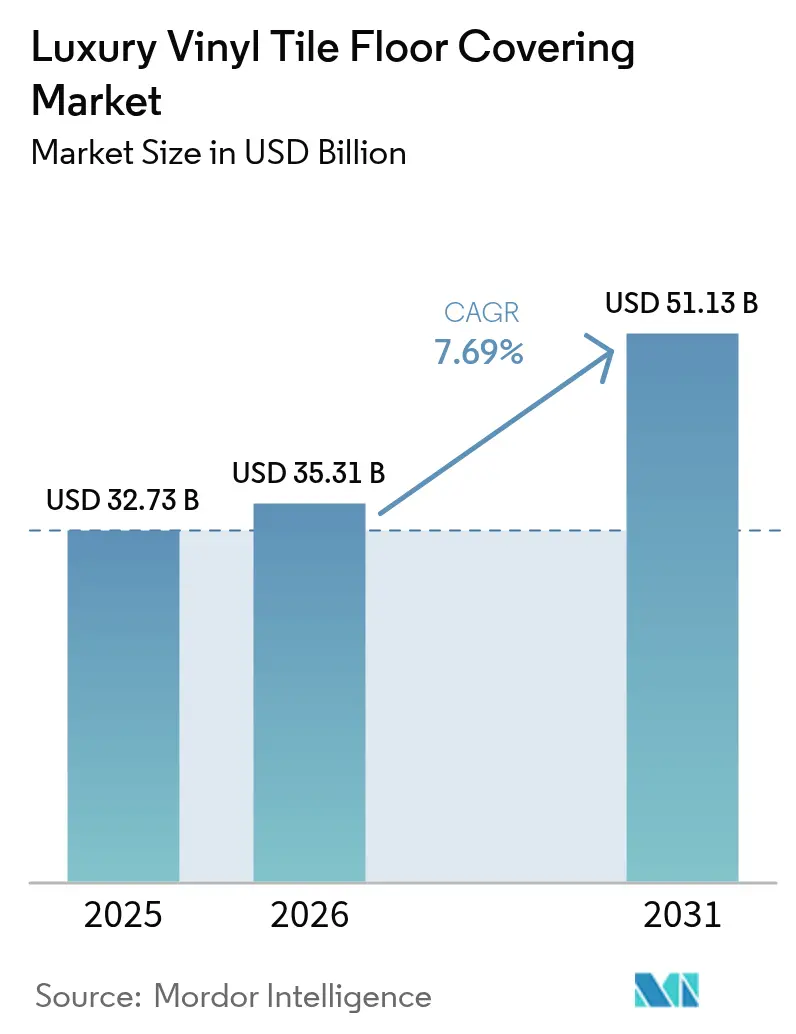

| Market Size (2026) | USD 35.31 Billion |

| Market Size (2031) | USD 51.13 Billion |

| Growth Rate (2026 - 2031) | 7.69% CAGR |

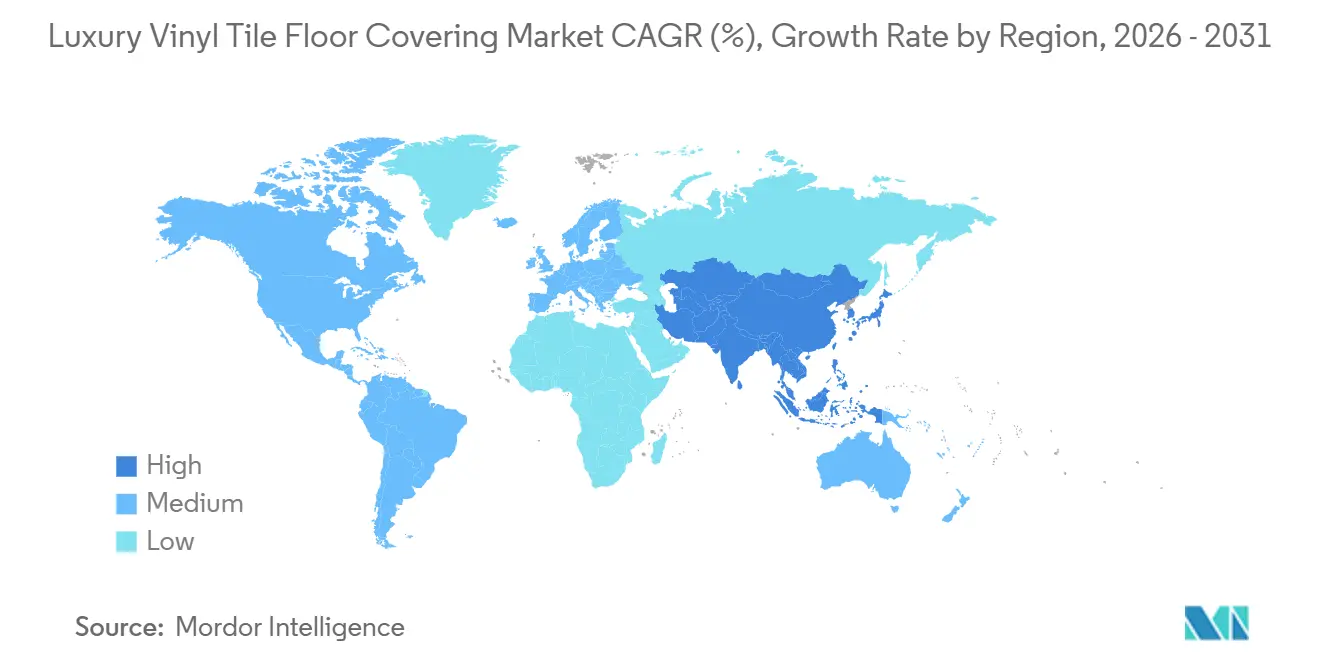

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

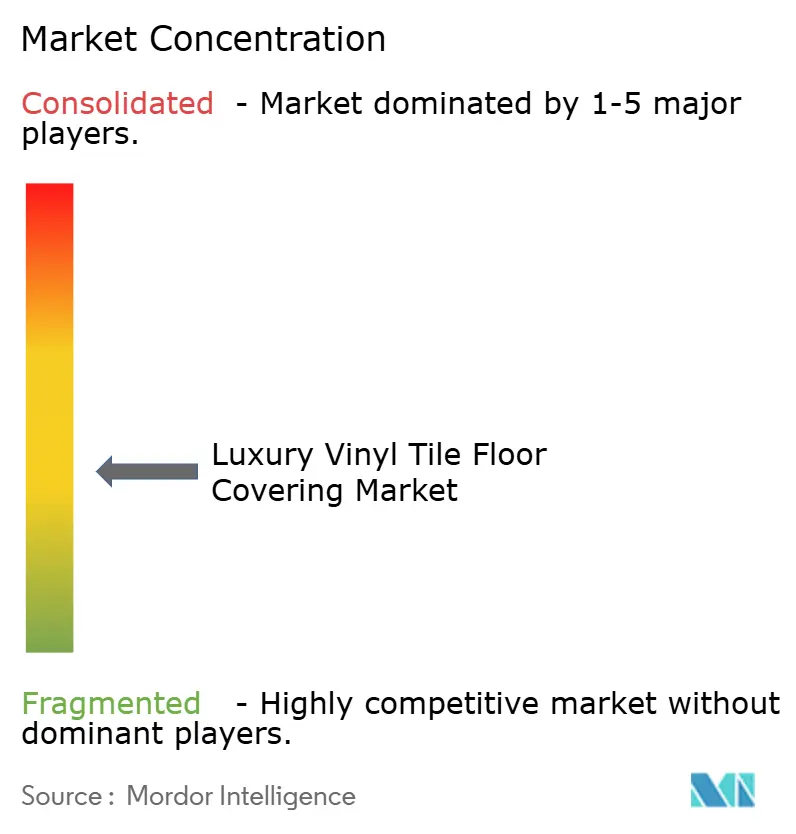

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Luxury Vinyl Tile Floor Covering Market Analysis by Mordor Intelligence

The luxury vinyl tile floor covering market size is expected to increase from USD 32.73 billion in 2025 to USD 35.31 billion in 2026 and reach USD 51.13 billion by 2031, growing at a CAGR of 7.69% over 2026-2031. Growth in 2026 is supported by steady residential retrofit activity and faster commercial renovations that favor rigid-core products for moisture resistance and quick installation. Rigid-core formats continue to gain traction as they reduce subfloor preparation needs and simplify click-lock installation, which lowers project timelines for both homeowners and facility managers. Domestic capacity additions in North America are compressing lead times and de-risking exposure to UFLPA detentions and Section 301 duties on Chinese-origin LVT. Asia-Pacific leads share and growth, with resilient demand from urban housing upgrades and institutional projects that prefer durable, easy-clean, and low-emission surfaces. Sustainability, material disclosure, and PVC-free or phthalate-free options are now baseline requirements in many healthcare, education, and public sector specifications, which are shaping product development and competitive positioning across the luxury vinyl tile floor covering market.

Key Report Takeaways

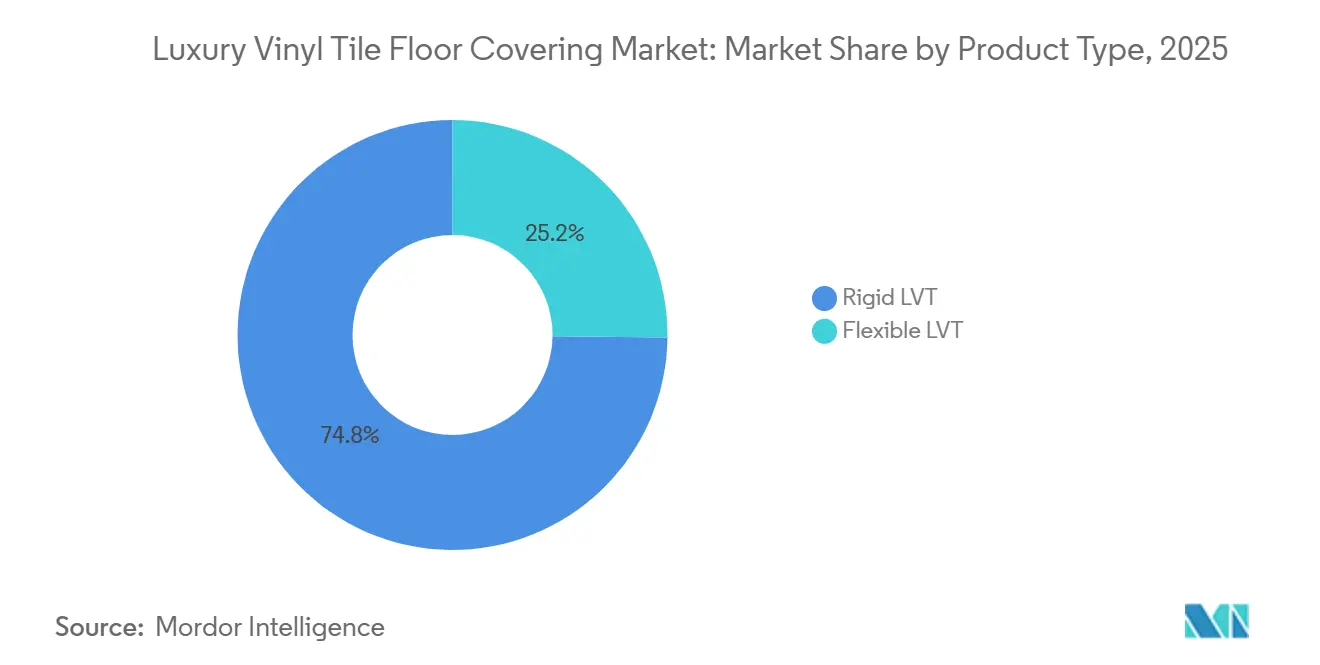

- By product type, rigid-core formats held 74.81% share in 2025 in the luxury vinyl tile floor covering market and are projected to expand at a 9.31% CAGR through 2031.

- By installation type, click-lock and floating installation captured 39.61% share in 2025 in the luxury vinyl tile floor covering market, with click-lock forecast at a 7.91% CAGR through 2031.

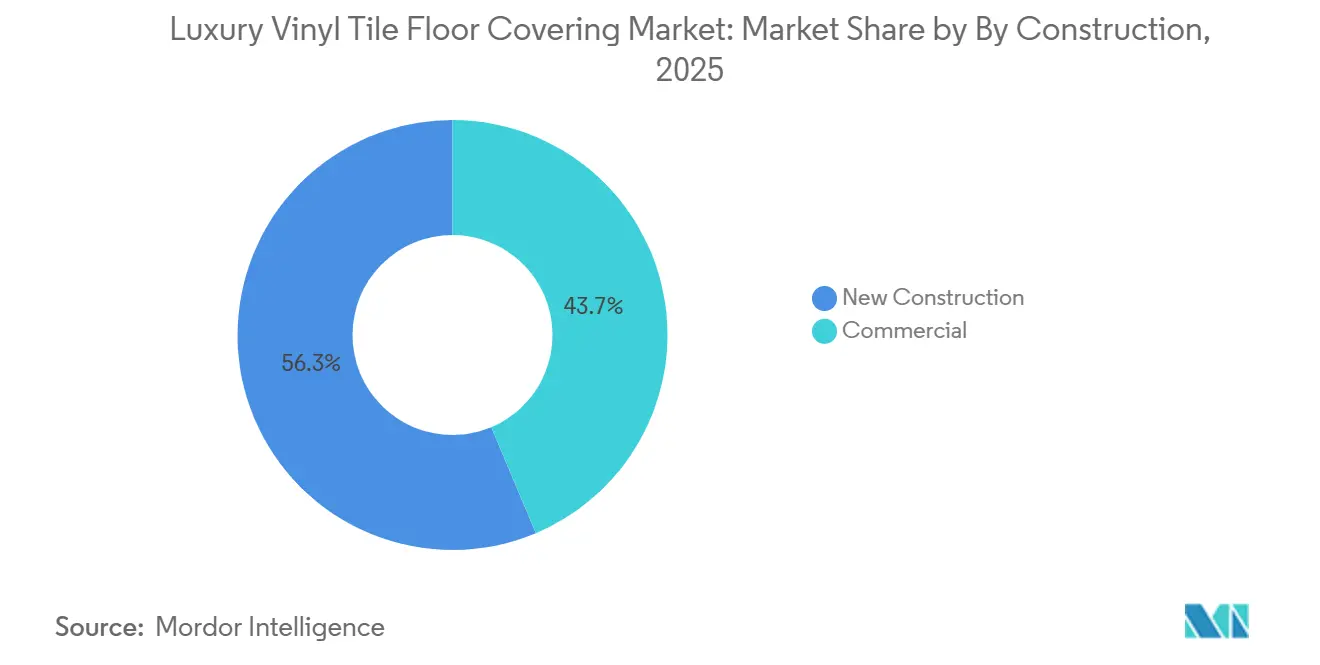

- By construction type, new construction led with a 56.34% share in 2025 in the luxury vinyl tile floor covering market, while remodeling and retrofit are the fastest-growing at an 8.12% CAGR to 2031.

- By end-user, residential applications accounted for a 67.12% share in 2025 in the luxury vinyl tile floor covering market, while commercial applications are projected to grow at a 7.98% CAGR through 2031.

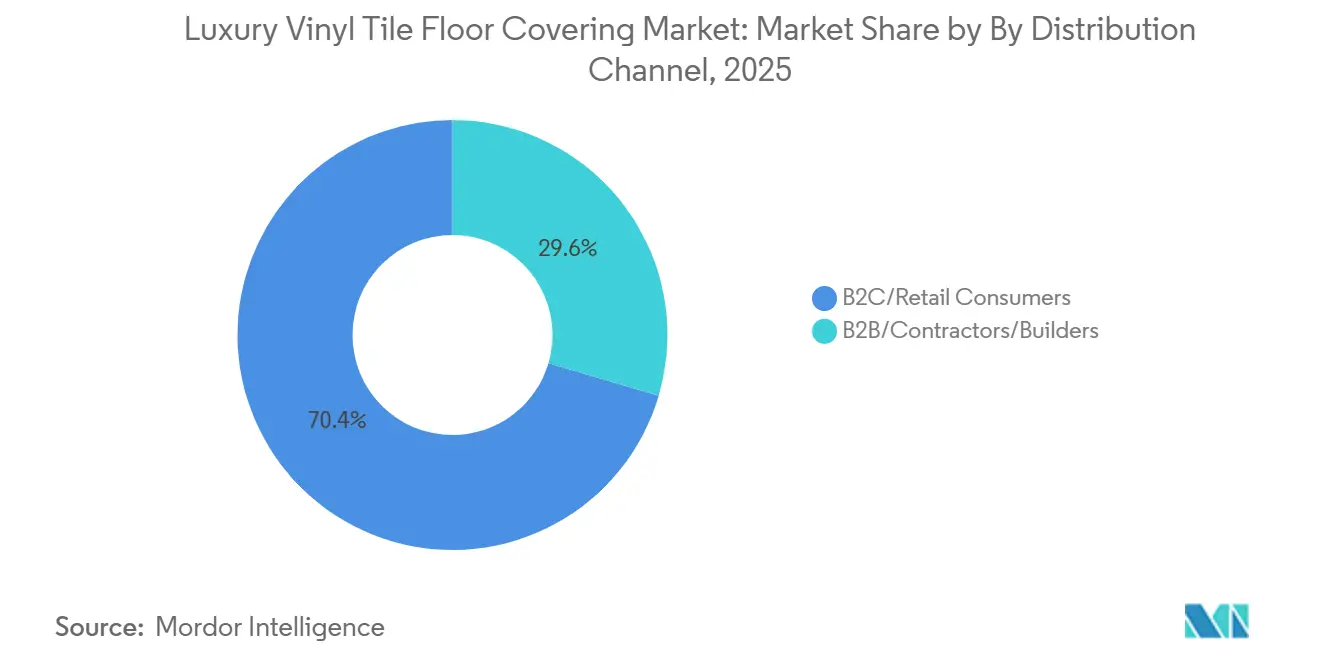

- By distribution channel, B2C represented a 70.44% share in 2025 in the luxury vinyl tile floor covering market, while the B2B contractor and builder channel is projected to grow at a 9.12% CAGR through 2031.

- By geography, Asia-Pacific led with 38.12% share in 2025 and is forecast to post the fastest growth at an 8.51% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Luxury Vinyl Tile Floor Covering Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rigid-core formats are displacing wood/laminate in renovations | +1.8% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Click/DIY installation reduces time and labor for retrofits | +1.2% | Global, particularly strong in North America residential | Short term (≤ 2 years) |

| Commercial retrofit demand for hygienic, low-VOC, easy-clean floors | +1.5% | North America, Europe, Asia-Pacific healthcare/retail hubs | Medium term (2-4 years) |

| E-commerce visualization and sampling are accelerating B2C conversion | +0.9% | Global, spearheaded by North America and Western Europe | Short term (≤ 2 years) |

| Domestic capacity additions de-risk supply and shorten lead times | +1.0% | North America primarily, with a spill-over to Latin America | Medium term (2-4 years) |

| PVC-free and recycled-content LVT unlocks regulated-spec demand | +1.3% | Europe (REACH), United States (Prop 65, state PFAS laws), select Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rigid-Core Formats Displacing Wood and Laminate in Renovations

Rigid-core LVT, encompassing SPC and WPC constructions, held a 74.81% share in 2025 and is projected to grow at a 9.31% CAGR through 2031, supported by dimensional stability, moisture resistance, and click-lock compatibility that lowers installation time in retrofit projects. SPC blends a high-calcium-carbonate content with PVC to achieve tight thermal expansion and compressive performance that limit telegraphing over minor subfloor imperfections, which is valuable in occupied renovations where extensive demo is disruptive [1]Parterre Flooring Team, “SPC and Rigid Core Flooring Technical Guide,” Parterre Flooring, parterreflooring.com. WPC offers improved acoustic comfort and underfoot feel for multi-family settings that prioritize IIC performance, which keeps rigid LVT attractive in condominiums and senior living. Manufacturers are also enhancing rigid cores with recycled inputs, such as Mohawk’s use of recycled PET within rigid cores to meet green-building criteria without sacrificing wear durability or joint integrity. These product attributes are replacing engineered wood in humidity-prone basements and coastal markets and have taken share from traditional laminate in laundry rooms, mudrooms, and other wet-prone zones where waterproofing is non-negotiable, which reinforces the ongoing shift toward rigid-core within the luxury vinyl tile floor covering market.

Click and DIY Installation Reduces Time and Labor for Retrofits

Click-lock and floating systems captured 39.61% share in 2025 and are projected to expand at a 7.91% CAGR to 2031, reflecting homeowner preference for DIY-friendly options and the removal of adhesive cure time that extends project schedules. Surveys indicate a strong tilt toward ease of installation among homeowners, with a large share ranking click systems above glue-down because simple tools and clear instructions reduce the overall complexity of room upgrades. Facility managers and retailers value the speed benefits of click-lock in overnight or off-hours renovations where reopening quickly is essential for revenue continuity, and where adhesive off-gassing would otherwise delay occupancy in sensitive interiors. Visualization tools and online configurators reinforce click adoption by giving buyers high confidence in color and pattern selection before delivery, which lowers returns and speeds the purchase decision. This predictable and faster installation pathway keeps click-lock rising within the luxury vinyl tile floor covering market.

Domestic Capacity Additions, De-Risk Supply, and Shorten Lead Times

CBP enforcement of the UFLPA has subjected PVC-containing imports to heightened scrutiny, producing detainments that disrupt flooring supply and push buyers to diversify toward domestic and nearshore sources [2]U.S. Department of Homeland Security, “Import Detentions and Statistics under UFLPA,” DHS, dhs.gov. In response, Shaw scaled SPC and LVT output in Ringgold, Georgia, with a USD 90 million investment that reduces replenishment times and supports buyers requiring domestic content assurances. AHF Products added a 328,000-square-foot facility in Cartersville, Georgia, in November 2025 to expand rigid-core and glue-down production for commercial and institutional projects with firm schedule requirements. Section 301 duties of 25% on Chinese-origin LVT further tilt procurement toward domestic alternatives, where pricing and timelines are more consistent for long-running programs. As these capacity moves take hold, lead times compress below typical overseas cycles and improve supply assurance for high-velocity SKUs in the luxury vinyl tile floor covering market.

PVC-Free and Recycled-Content LVT Unlocks Regulated-Spec Demand

PVC-free and low-phthalate formulations are gaining share as public health standards and retailer policies tighten, creating demand for polyolefin, polyurethane, and bio-attributed alternatives with strong emissions performance. Mohawk’s PureTech line is positioned with high recycled content and renewable feedstocks to satisfy material disclosure criteria in projects targeting LEED and similar frameworks. Shaw’s EcoWorx Resilient integrates post-consumer polyolefin and closed-loop design to support take-back, which aligns with customer goals on circularity and end-of-life management. AHF Products introduced MedinPure, a PVC-free healthcare solution designed for rigorous cleaning protocols and indoor air quality targets, reflecting a shift toward regulated-spec portfolios. EU REACH restrictions and California Proposition 65 reinforce the move to phthalate-free chemistries at or below prescribed thresholds, making compliant lines from established players such as Tarkett central to specifications across hospitals, schools, and public buildings[3]European Chemicals Agency Editorial, “REACH Restrictions on Phthalates,” ECHA, echa.europa.eu. The resulting formulation changes raise production complexity and cost yet unlock high-value projects and long-term relationships in the luxury vinyl tile floor covering market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| UFLPA detainments and trade barriers disrupt supply chains | -1.4% | The United States primarily, with a spill-over to Canada and Mexico | Short term (≤ 2 years) |

| Raw material price volatility (PVC resin, plasticizers) | -0.9% | Global, with Europe and Asia-Pacific more exposed to energy-linked swings | Medium term (2-4 years) |

| Tightening chemical policies (phthalates/PFAS) increases compliance costs | -0.6% | Europe (REACH), United States (state-level PFAS bans), select Asia-Pacific | Long term (≥ 4 years) |

| Quality issues in entry-level SPC spur warranty claims and brand risk | -0.5% | Global, particularly affecting low-cost import channels | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

UFLPA Detainments and Trade Barriers Disrupt Supply Chains

UFLPA enforcement has increased documentation demands and detentions for PVC-containing products, leading to unpredictable transit times and clearance outcomes that constrain planning for import-reliant programs. Buyers are responding by allocating a larger share of their spending to domestic output or to nearshore sources with traceable inputs, which reduces detainments and port congestion exposure. Section 301 duties at 25% on Chinese-origin LVT are also material to landed costs, making domestic price points more compelling on multi-year renovations or healthcare standardization programs [4]Office of the United States Trade Representative, “Section 301 Tariffs on Chinese-Origin Goods,” USTR, ustr.gov. Projects with strict occupancy milestones or regulatory deadlines are prioritizing domestic content to avoid detainment-driven construction delays. These trade and compliance realities shift sourcing patterns and encourage strategic supplier consolidation in the luxury vinyl tile floor covering market.

Raw Material Price Volatility and Compliance Costs Pressure Margins

Feedstock prices for PVC systems and plasticizers can be volatile, influenced by energy dynamics, operating rates, and regional supply balances that drive periodic surcharges along the value chain. Compliant products require emissions testing and material disclosure that add recurring costs for labs, certification, and quality audits, which manufacturers manage with SKU rationalization and co-extrusion refinements. Washington State’s phthalate threshold at 1,000 ppm for certain product categories and state-level PFAS restrictions make formulation and portfolio management more complex and often require separate configurations by jurisdiction. Proposition 65 labeling requires careful substance controls and disclosure workflows that are now standard in large retail and institutional programs. Entry-level rigid cores with thin wear layers and substandard surface coatings have generated warranty and performance concerns, which pressure value-tier assortments and shift some commercial specifications back to higher-spec rigid LVT or WPC alternatives.

Segment Analysis

By Product Type: Rigid Cores Dominate Through Retrofit Superiority

Rigid LVT commanded 74.81% of the Luxury Vinyl Tile Floor Covering market share in 2025 and is projected to expand to a 9.31% CAGR during 2026-2031 as specifiers prize dimensional stability, waterproofing, and click system compatibility in occupied renovations. SPC uses a high mineral load to resist movement over minor subfloor variation and to control telegraphing, which reduces prep work in commercial corridors and multifamily transitions. WPC’s lighter core structure aids acoustic comfort and thermal feel, which is valued in condominium conversions and senior living, while maintaining the scratch and stain performance needed in daily-use spaces. Manufacturers are improving rigid core sustainability by using recycled inputs and material disclosures to qualify for LEED and related frameworks.

Flexible LVT retains utility in complex perimeter runs, cove base transitions, and heat-welded monolithic installations where rigid planks are less practical. Healthcare and back-of-house settings continue to value sheet and flexible configurations where continuous surfaces reduce microbial harborage points and ease disinfection. As rigid cores scale, product portfolios are diversifying with embossed-in-register finishes and low-gloss topcoats that improve realism under different lighting conditions. These advances sustain the share advantage of rigid cores, while flexible LVT concentrates on technical applications that demand specialized installation and detailing in the luxury vinyl tile floor covering market.

By Installation Type: Click-Lock Gains on Labor Savings and E-Commerce Synergy

Click-lock and floating systems held a 39.61% share in 2025 and are projected at a 7.91% CAGR through 2031, with growth tied to lower installation time, minimal tools, and avoidance of adhesive cure windows that can stall occupancy in time-sensitive jobs. Homeowners report a strong preference for easy-install planks, which supports direct-to-consumer fulfillment and planned weekend projects that avoid the cost of professional labor. In retail and hospitality retrofits, click-lock allows crews to complete corridor or lobby zones overnight, preserving trading hours and guest experience. Online visualizers and mobile-first configurators further encourage click adoption, since buyers can preview colors at scale in their own rooms before ordering cartons.

Glue-down remains important in high-traffic areas that experience rolling loads, where permanent adhesion dampens movement and supports spot repairs by replacing individual planks without disturbing adjacent units. Loose-lay formats occupy specific use cases where subfloor moisture or temporary layouts favor friction or perimeter bonding over full-spread adhesive. Where indoor air quality is central, floors installed without solvent-based adhesives reduce emissions and simplify compliance with third-party certifications. The installation mix keeps shifting toward click-lock as e-commerce integration improves, yet glue-down and loose-lay continue to solve technical needs in the luxury vinyl tile floor covering market.

By Construction Type: Retrofit Gains as Aging Infrastructure Drives R&R Cycles

New construction held 56.34% in 2025, yet remodeling and retrofit are forecast to be the fastest at an 8.12% CAGR, driven by aging building stock and reconfigurations that follow hybrid-work patterns and evolving space standards. Owners prefer solutions that minimize downtime, which puts waterproof rigid LVT and click-lock at an advantage for weekend or overnight work. Surface-ready installation over existing floors reduces demolition and disposal, especially where older vinyl or resilient surfaces may carry abatement concerns. Scheduling reliability and predictable replenishment also matter in retrofit clusters that proceed floor by floor in occupied settings.

In residential retrofit, homeowners often prioritize single-day installations that keep rooms functional and avoid relocation, which supports click-lock growth. In commercial retrofit, facility teams lean on standardized SKUs, colorways, and transitions to consolidate inventory and reduce training complexity for maintenance crews. Public sector projects follow accessibility and indoor-air targets that align better with resilient surfaces than many alternatives at equivalent cost. As more portfolios adopt planned refresh programs, the share of retrofit-ready LVT continues to climb in the luxury vinyl tile floor covering market.

By End-User: Commercial Growth Outpaces Residential on Hygiene Mandates

Residential demand represented 67.12% in 2025, reflecting the broad adoption of waterproof rigid LVT in kitchens, baths, laundry rooms, and basements where moisture performance is decisive. The commercial segment is forecast to grow at a 7.98% CAGR to 2031 as healthcare, hospitality, retail, and education emphasize indoor air quality, cleaning durability, and uptime. Heat-welded seams in flexible or sheet configurations provide monolithic surfaces in sensitive areas that must control microbial growth and withstand repeated disinfection. As organizations standard finish schedules across multi-site portfolios, compliant LVT formats that meet emissions and material disclosure thresholds move from optional to required in many specifications.

Hospitality favors digitally precise visuals at a lower installed cost than natural materials, which extends brand refresh cycles and supports franchise brand standards without disrupting cash flows. Retail and shopping centers prize durability, maintenance simplicity, and spot-repair capability, which reduce life-cycle costs versus products that require broad-area replacement. Education systems target resilient surfaces that work with rigid cleaning routines and lower annual maintenance, improving long-term budgets. Corporate offices and public buildings add demand for low-emitting options that align with LEED and WELL credits, where material health and end-of-life programs are now tracked in capital plan reporting.

By Distribution Channel: B2B Contractor Segment Gains on Institutional Sourcing

B2C channels represented 70.44% share in 2025, while B2B contractors and builders are forecast to grow fastest at 9.12% CAGR as institutional buyers consolidate volume and prioritize assured supply. Home centers and specialty stores remain important to B2C for their broad assortments, visualization tools, and sample programs that lower decision risk. Digital platforms that integrate room preview capabilities and quick-ship samples reinforce B2C confidence in color and texture selection. These tools help B2C, while B2B leverages long-term pricing and capacity commitments to reduce budget variability.

Builders and commercial contractors prefer programs that align with construction schedules, with just-in-time delivery, subfloor guidance, and technical support from manufacturer teams. Domestic capacity expansions, including new lines in Georgia, improve lead times and provide traceable origin documentation that supports public procurement. As buyers diversify supply against trade risk, closer-to-market production strengthens the contractor channel’s reliability and response, which sustains B2B momentum in the luxury vinyl tile floor covering market.

Geography Analysis

Asia-Pacific led with 38.12% share in 2025 and is forecast to grow at 8.51% CAGR during 2026-2031, supported by urban housing upgrades, institutional expansion, and favorable economics for waterproof, easy-clean surfaces in tropical and subtropical climates. China drives large-scale output and domestic consumption, while India’s steady residential and healthcare buildout lifts install volumes for resilient formats. Southeast Asian markets add growth in hospitality and retail footprints that favor durable and slip-resistant surfaces under high traffic. Japan and South Korea maintain consistent demand for lightweight, resilient options compatible with modern building codes and senior-living needs. Australia rounds out regional demand with balanced residential and commercial retrofits that emphasize coastal moisture performance in the luxury vinyl tile floor covering market.

Europe is forecast at an 8.20% CAGR over 2026-2031 as REACH-compliant chemistries and low-emission solutions align with the region’s renovation bias and high average building ages. Phthalate restrictions under EU REACH and evolving discussions on PFAS regulation reinforce the shift to alternative plasticizers and PVC-free solutions in commercial and public tenders. Northern and Western European markets put weight on circularity, take-back options, and EPD-backed disclosures, which reward manufacturers that can document material health and recycled content. Southern markets increase use in hospitality and residential updates, where digitally rich visuals at a lower installed cost than stone or ceramic help projects meet design targets. The United Kingdom retains robust LVT adoption across build-to-rent and public health facilities with procurement that prizes emissions performance and clear compliance documentation, which keeps the region a strong buyer in the luxury vinyl tile floor covering market.

North America is projected at a 7.90% CAGR for 2026-2031, lifted by residential replacements and commercial retrofits that balance budget, speed, and IAQ priorities. Capacity expansions in Georgia improve domestic availability and shorten replenishment cycles for high-turn SKUs, which reduces exposure to UFLPA detainments and Section 301 duties that have complicated import planning. Institutional buyers in healthcare, education, and government emphasize Buy American compliance and third-party emissions certifications, as well as take-back provisions in some bids. Canada adds steady demand in urban provinces for multifamily and commercial retrofits with LEED-aligned goals, while Mexico benefits from nearshoring-led facilities that adopt resilient surfaces for ease of maintenance and durability. State-level restrictions on targeted chemicals and signal policies from major home centers on phthalate-free portfolios further shape assortment and sourcing in the region.

Competitive Landscape

The luxury vinyl tile floor covering market remains moderately fragmented at the global level as top multinational groups compete with regional specialists and private-label programs that serve distinct niches. Players differentiate on sustainability credentials, documented emissions performance, and circularity, which are now standards in many healthcare, education, and public sector specifications. Mohawk’s PVC-free and high-recycled content approach, Shaw’s EcoWorx Resilient take-back and polyolefin content, and AHF’s PVC-free healthcare introduction represent the industry’s material evolution toward regulated-spec portfolios. These platforms align with EU REACH and United States state-level policies, which improve eligibility for long-horizon projects and master service agreements in the luxury vinyl tile floor covering market.

North American capacity expansions illustrate the strategic shift to onshore supply for better schedule control, price certainty, and compliance documentation. Shaw expanded SPC and LVT output in Ringgold, Georgia, with a USD 90 million program, while AHF added a 328,000-square-foot plant in Cartersville in November 2025 to bolster rigid-core and glue-down production. These moves compress lead times below overseas cycles and create assured supply for public procurement that requires origin traceability and material disclosures. Retailer policies also shape supply, as large home centers maintain phthalate-free commitments that accelerate portfolio transitions among tier-one and private-label suppliers.

Product development focuses on realistic visuals, improved abrasion and stain resistance, and mechanical lock designs that withstand rolling loads while enabling fast installation. Embossed-in-register textures and low-gloss finishes elevate aesthetic fidelity, and direct-to-consumer platforms integrate visualizers for faster selection and lower returns. Brands that back advanced visuals with credible emissions certifications and documented recycled or bio-attributed content are gaining access to premium projects in healthcare and education. As procurement tightens material health criteria, suppliers that meet disclosure requirements and support take-back programs stand out as partners for multi-year programs across the luxury vinyl tile floor covering market.

Luxury Vinyl Tile Floor Covering Industry Leaders

Mohawk Industries

Shaw Industries Group

Tarkett

Gerflor Group

Forbo Flooring Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Tarkett unveiled its new Collaborative Collection featuring recycled and bio-attributed materials, targeting LEED v4.1 and WELL Building Standard certifications for commercial projects; the line incorporates post-industrial vinyl recovery streams and renewable-carbon plasticizers to reduce Scope 3 emissions by an estimated 30% versus conventional formulations.

- January 2026: Evonik completed expansion of its Marl, Germany plasticizer production facility, increasing capacity for DOTP and DINCH non-phthalate formulations by 20% to meet rising European demand for REACH-compliant LVT; the investment totals EUR 15 million and includes advanced filtration systems reducing process-water discharge.

- November 2025: AHF Products acquired a 328,000-square-foot manufacturing facility in Cartersville, Georgia—its twelfth North American plant—to expand rigid-core LVT and glue-down vinyl production; the acquisition supports domestic sourcing strategies amid UFLPA enforcement and adds capacity for MedinPure PVC-free healthcare flooring launched earlier in 2025.

- October 2024: Republic Floor introduced its Light SPC rigid-core line, engineered to reduce plank weight by approximately 20% versus traditional SPC while maintaining Class 33 commercial wear-layer durability; installer feedback cited handling fatigue on upper-story installations as the primary design driver.

Global Luxury Vinyl Tile Floor Covering Market Report Scope

A complete background analysis of the Luxury Vinyl Tile Floor Covering Market, which includes an assessment of the National accounts, economy, and the emerging market trends by segments, significant changes in the market dynamics, and the market overview, is covered in the report. The Luxury Vinyl Tile Floor Covering Market Report is Segmented by Product Type (Rigid LVT and Flexible LVT), Installation Type (Click-Lock, Glue-Down, and Loose-Lay), End-User (Residential and Commercial), Construction Type (New Construction and Remodeling), Distribution Channel (B2C and B2B), and Geography (North America, South America, Europe, Asia-Pacific and Middle East & Africa). Market Forecasts are Provided in Terms of Value (USD).

| Rigid LVT | Stone Plastic Composite |

| Wood Plastic Composite | |

| Flexible LVT |

| Click-Lock / Floating |

| Glue-Down |

| Loose-Lay |

| New Construction |

| Remodeling / Retrofit |

| Residential | |

| Commercial | Hospitality & Leisure |

| Retail & Shopping Centers | |

| Healthcare Facilities | |

| Education | |

| Corporate Offices | |

| Public & Government Buildings | |

| Other Commercial Users |

| B2C/Retail Consumers | Home Centers |

| Specialty Flooring Stores | |

| Online | |

| Other Distribution Channels | |

| B2B/Contractors/Builders |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Product Type | Rigid LVT | Stone Plastic Composite |

| Wood Plastic Composite | ||

| Flexible LVT | ||

| By Installation Type | Click-Lock / Floating | |

| Glue-Down | ||

| Loose-Lay | ||

| By Construction Type | New Construction | |

| Remodeling / Retrofit | ||

| By End User | Residential | |

| Commercial | Hospitality & Leisure | |

| Retail & Shopping Centers | ||

| Healthcare Facilities | ||

| Education | ||

| Corporate Offices | ||

| Public & Government Buildings | ||

| Other Commercial Users | ||

| By Distribution Channel | B2C/Retail Consumers | Home Centers |

| Specialty Flooring Stores | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Contractors/Builders | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current and projected size of the luxury vinyl tile floor covering market?

The Luxury Vinyl Tile Floor Covering market size is expected to increase from USD 32.73 billion in 2025 to USD 35.31 billion in 2026 and reach USD 51.13 billion by 2031 at a 7.69% CAGR.

Which product category is growing fastest within the luxury vinyl tile floor covering market?

Rigid-core formats held 74.81% share in 2025 and are projected to grow at a 9.31% CAGR during 2026-2031, outpacing flexible LVT on stability, waterproofing, and fast installation.

Which installation method is preferred for renovations in the luxury vinyl tile floor covering market?

Click-lock and floating systems lead to retrofits due to faster, easier installs and no adhesive cure time, with a 39.61% share in 2025 and a 7.91% projected CAGR.

Which region leads to demand in the luxury vinyl tile floor covering market?

Asia-Pacific led with 38.12% share in 2025 and is forecast to be the fastest-growing region at an 8.51% CAGR through 2031 on urban housing upgrades and institutional projects.

How are trade and compliance factors affecting the luxury vinyl tile floor covering market?

UFLPA detainments and Section 301 duties are shifting volumes toward domestic supply, reducing lead times and improving schedule control for regulated projects.

What sustainability trends are shaping the luxury vinyl tile floor covering market?

PVC-free and phthalate-free lines with recycled or bio-attributed content, credible emissions certifications, and take-back programs are becoming standard in healthcare, education, and public tenders.

Page last updated on: