Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

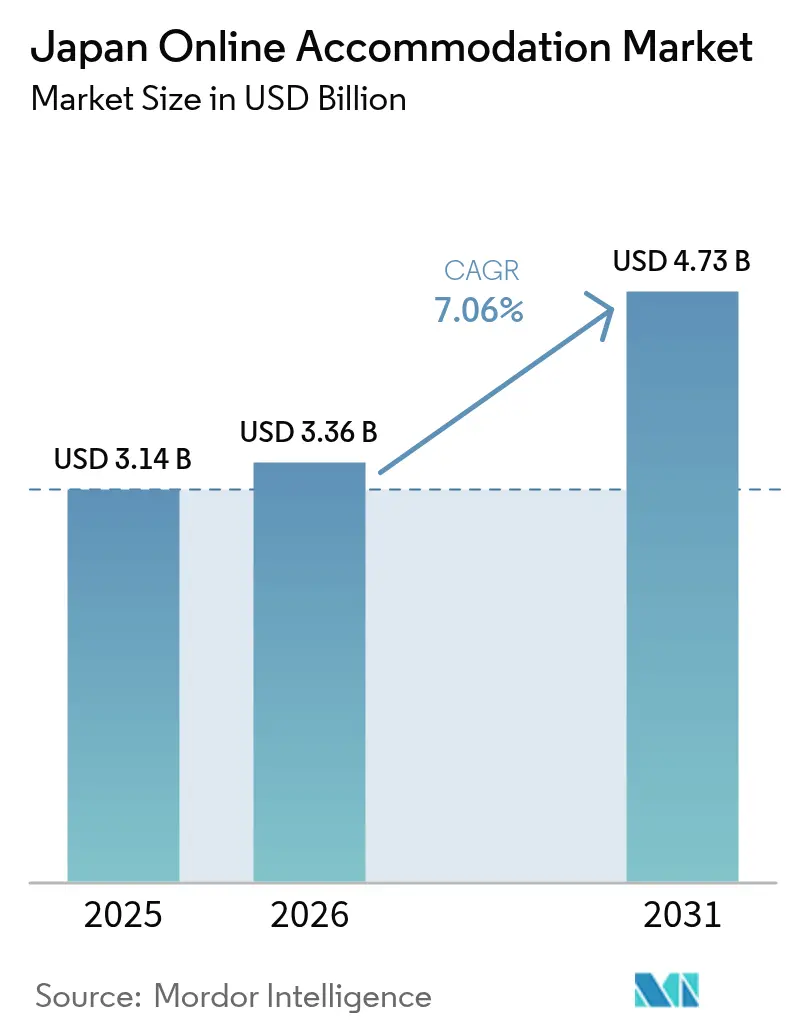

| Base Year Market Size (2025) | USD 3.14 Billion |

| Market Size (2026) | USD 3.36 Billion |

| Market Size (2031) | USD 4.73 Billion |

| Growth Rate (2026 - 2031) | 7.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Online Accommodation Market Analysis by Mordor Intelligence

The Japan online accommodation market size was valued at USD 3.14 billion in 2025 and estimated to grow from USD 3.36 billion in 2026 to reach USD 4.73 billion by 2031, at a CAGR of 7.06% during the forecast period (2026-2031). Growth in 2026 is led by sustained inbound recovery that brought 42.7 million international visitors in 2025, continued channel shift to mobile, and platform innovation that improves conversion and monetization across fragmented inventory[1]Japan National Tourism Organization, “Visitor Arrivals & Japanese Overseas Travelers,” JNTO, jnto.go.jp. Key distribution and infrastructure factors amplify this channel realignment in 2026. Japan’s 5G population coverage reached 98.4% by the end of FY2024 (March 2025), while median download speeds reported by independent measurement providers sustain high-quality visual merchandising that reduces booking friction on phones [2]Ministry of Internal Affairs and Communications, “5G Population Coverage and Telecommunications Statistics,” MIC, soumu.go.jp. Large-scale events and seasonal peaks continue to push major city occupancy higher, with Osaka posting elevated levels across the six-month Expo 2025, reinforcing the appeal of algorithmic revenue tools that smaller operators can now access via packaged APIs. Regional dispersion policies and targeted subsidies are in place in 2026 to spread demand away from the three largest urban areas, which strengthens prospects for faster growth in Kyushu and Okinawa relative to Kanto’s larger, steadier base.

Key Report Takeaways

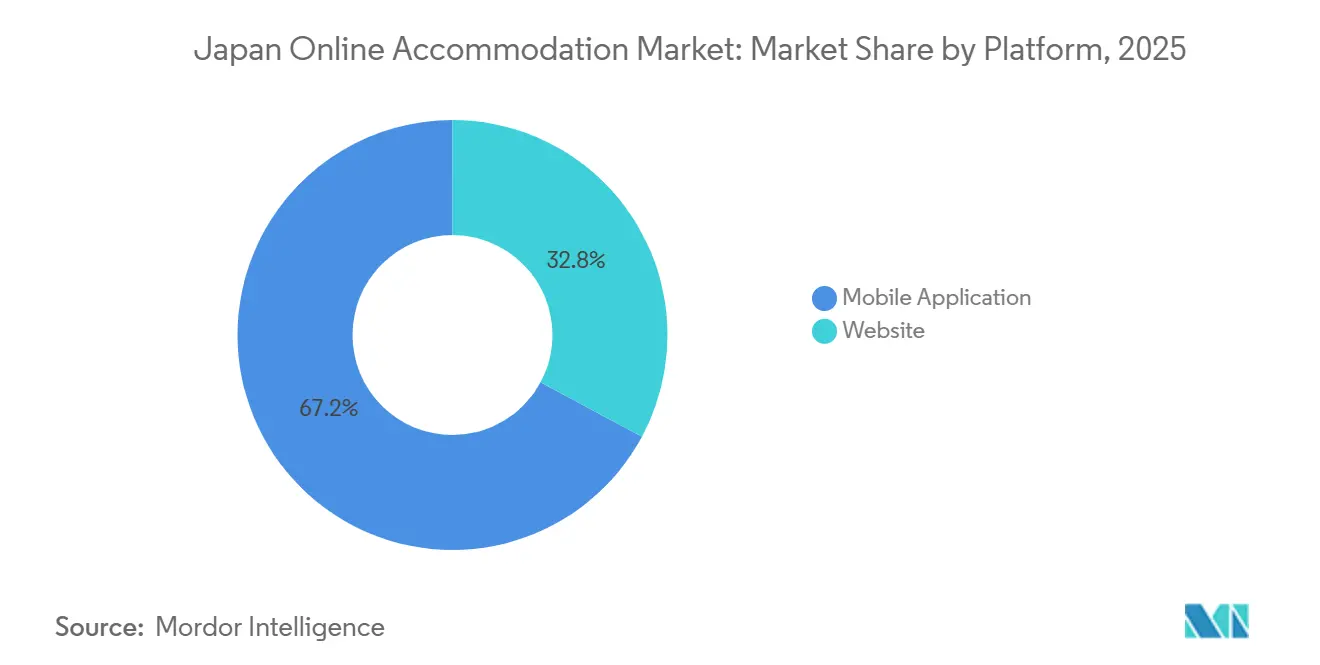

- By platform, mobile applications led with 67.16% of the market share of the Japanese online accommodation market in 2025 and are forecast to expand at a 11.55% CAGR to 2031.

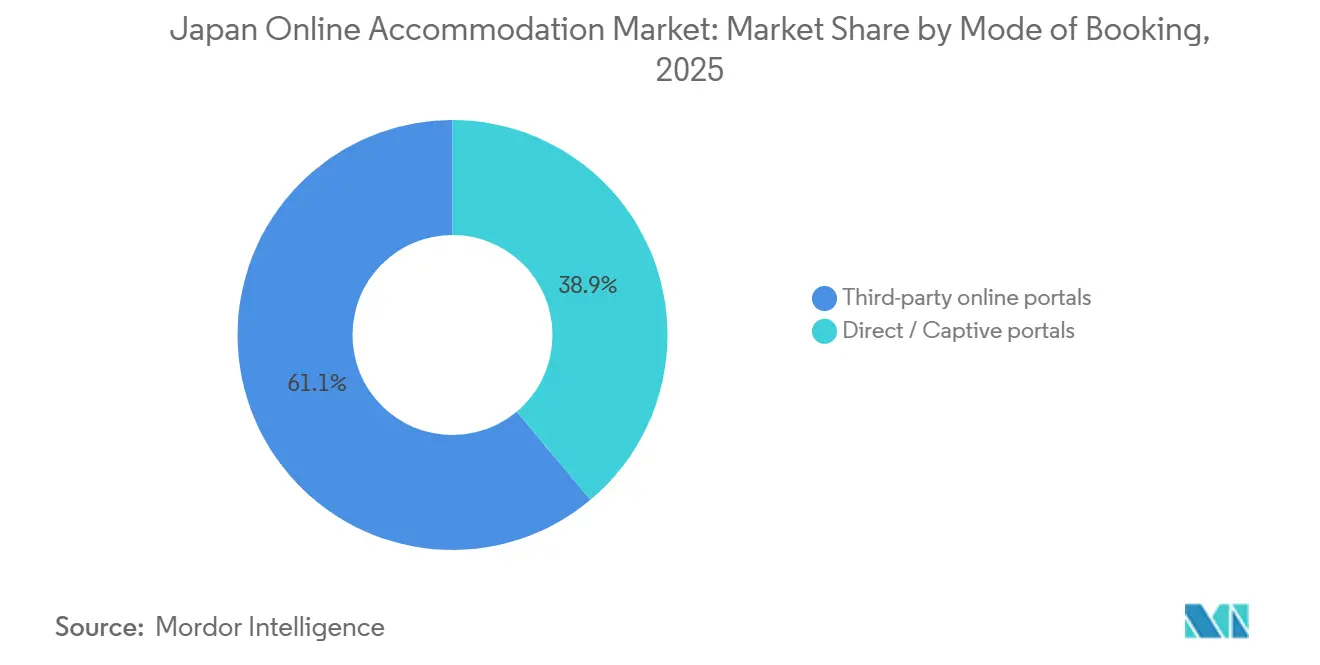

- By mode of booking, third-party online portals held 61.10% of the Japanese online accommodation market share in 2025, while vacation rentals via third-party portals posted the fastest projected growth at a 13.72% CAGR through 2031.

- By property type, hotels and resorts accounted for 46.75% of the Japan online accommodation market share in 2025, while vacation rentals are projected to grow at a 15.11% CAGR through 2031.

- By geography, Kanto accounted for 36.44% of the Japanese online accommodation market in 2025, and Kyushu & Okinawa are forecast to be the fastest-growing region at a 9.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Online Accommodation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Travel subsidies significantly boost domestic tourism growth | +1.2% | National, with concentration in Fukushima, Tohoku, and Kyushu prefectures, offering travel coupons | Medium term (2-4 years) |

| 5g penetration drives surge in mobile travel bookings | +1.8% | National, urban centers show strong 5G availability, and rural areas benefit from 98.4% population coverage | Short term (≤ 2 years) |

| Regulatory easing expands vacation rental market supply | +1.3% | National, centralized verification effective from April 2026 | Long term (≥ 4 years) |

| Local OTAs introduce SME-focused corporate travel bundles | +0.7% | National, with emphasis on regional hubs such as Nagoya, Sapporo, and Fukuoka | Medium term (2-4 years) |

| AI pricing strategies target Osaka Expo 2025 demand | +1.1% | National, with early gains in Osaka and Tokyo expanding to regional events | Short term (≤ 2 years) |

| Rural incentives extend stays for digital nomads | +0.9% | Regional, strongest in Nagasaki pilots, Tohoku revitalization zones, and coastal prefectures | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Travel Subsidies Significantly Boost Domestic Tourism Growth

Prefectural campaigns in 2026 are designed to extend stay lengths and shift bookings into under-visited areas, which supports steadier occupancy outside the three largest metros. Fukushima Prefecture offers traveler subsidies for multi-night tours through February 28, 2026, which directly targets longer-stay behavior and reinforces regional cash flows for smaller operators [3]Fukushima Prefecture Tourism, “Fukushima Travel Subsidies 2025–2026,” Fukushima Travel Trade, fukushima-tourism.jp. These localized incentives pair well with regional transport and onsen access, which platforms can promote through targeted landing pages and app notifications to help shift demand away from peak dates. The policy emphasis on dispersal complements national overtourism measures and enables cross-selling for domestic OTAs that maintain deeper regional supplier relationships. As these programs scale, the Japan online accommodation market benefits from broader geographic conversion and reduced dependence on urban peaks that strain capacity.

Local OTAs Introduce SME-Focused Corporate Travel Bundles

A next-generation travel management platform launched in 2025 targets small and medium enterprises with integrated lodging, transport, and meeting solutions that simplify procurement and compliance. Rakuten Travel expanded its global property coverage in late 2025, allowing SMEs to consolidate domestic and outbound hotel purchases into a single loyalty stack to reduce fragmentation. [4]Rakuten Group, “Rakuten Travel Service and Global Inventory Expansion,” Rakuten Travel, travel.rakuten.comAirlines and transport partners extend these bundles by exposing accommodation inventory in their apps and loyalty programs to generate ancillary revenue without building proprietary supply systems. These initiatives increase average booking values and improve repeat-purchase frequency, stabilizing seasonality for domestic platforms serving regional business corridors. As these use cases mature, the SME segment expands the addressable base for the Japan online accommodation market and strengthens platform moats via embedded rewards and reporting tools.

AI Pricing Strategies Target Osaka Expo 2025 Demand

Dynamic pricing tools are now widely accessible via cloud APIs that automate rate updates based on demand signals, such as events and competitor movements, improving revenue capture during peak periods. A 2025 acquisition of a hotel pricing specialist by a major technology supplier accelerated the deployment of enterprise-grade revenue algorithms across independent and midscale properties. Vendor case studies report material RevPAR improvements where automated elasticity modeling replaces static rate cards, including outcomes for Japan properties using a leading pricing manager. Hospitality chatbots and booking engines integrate with these pricing systems to personalize offers and shorten search-to-booking paths for both hotels and professionally managed rentals. As event calendars expand and seasonality remains pronounced, AI-led pricing supports monetization across the Japan online accommodation market by aligning rates with real-time willingness-to-pay signals.

Rural Incentives Extend Stays for Digital Nomads

Japan’s digital nomad visa policy allows eligible remote workers from selected countries to stay for several months, creating demand for furnished accommodations with reliable connectivity and workspaces. Nagasaki Prefecture piloted a program in late 2025 to host digital workers for extended residencies, signaling local appetite to attract knowledge workers to offset population decline. National revitalization initiatives place professionals in smaller municipalities on one- to three-year assignments, which sustains steady demand for serviced apartments and extended-stay options. Budgeted overtourism and regional dispersion measures complement these efforts by improving tourism infrastructure and co-working availability in targeted prefectures. Together, these programs add longer-stay segments that reinforce the growth of vacation rentals and serviced options within the Japan online accommodation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulations on short-term rental zoning and licensing | -1.0% | National, with acute limits in Kyoto residential zones and selected Tokyo wards | Long term (≥ 4 years) |

| Low digital literacy among the aging population | -0.6% | National, most pronounced in rural prefectures with older demographics | Medium term (2-4 years) |

| Profit margins impacted by super-apps | -0.8% | National, strongest in urban commuter belts with deep payment wallet penetration | Short term (≤ 2 years) |

| Hotel capacity constraints during peak events | -0.7% | Kanto and Kansai, with event-driven surges and high baseline occupancy | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regulations on Short-Term Rental Zoning and Licensing

Japan’s private lodging regime combines a national baseline with municipal overlays, and heritage districts in Kyoto enforce particularly tight residential-area limits to preserve neighborhood character. Local caps and calendar restrictions create uneven availability, shifting bookings toward licensed hotels and ryokans during high season, when lodging demand is concentrated. A national system for real-time verification now improves overall compliance hygiene, but municipalities retain authority to impose stricter rules when housing or quality-of-life concerns escalate. This layered enforcement raises operational complexity and costs for smaller hosts while tilting the field toward professional managers who can navigate local compliance requirements. These constraints moderate the speed at which rentals can scale in core districts and shape how platforms curate listings in the Japan online accommodation market.

Hotel Capacity Constraints During Peak Events

During citywide events, occupancy and rates rise quickly, and operators often institute minimum-stay policies that reduce options for budget travelers and SME corporate trips. Osaka maintained elevated occupancy and strong RevPAR throughout the six-month Expo period, which concluded in mid-October 2025, demonstrating how extended events compress availability. Tokyo’s high baseline of business and leisure demand heading into 2026 points to recurring tight windows around festivals and sports schedules in the capital. With construction timelines measured in years, new capacity lags event calendars, which sustains intermittent scarcity and pushes some travelers to alternate formats that do not always meet business standards. These bottlenecks drive spillover across regions and channels, influencing price discovery and conversion patterns in the Japan online accommodation market.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Mobile Apps Dominate as 5G Enables Real-Time Discovery

Mobile applications accounted for 67.16% of bookings by platform in 2025 and are projected to post 11.55% growth through 2031, beating the overall pace as users adopt app-first shopping and checkout flows. The Japan online accommodation market benefits from broad 5G coverage, which reduces latency and supports rich media, making mobile the default interface in both urban and regional settings. Median network speeds sustain high-resolution imagery and virtual tours, closing the experience gap that once favored in-person agents and desktop comparison. App-only promotions and wallet-linked events in the Yahoo! Travel ecosystem increase repeat usage, reinforcing app engagement loops and narrowing the role of desktop in many booking journeys. As these forces compound, mobile’s lead becomes a durable feature of the Japan online accommodation market, with discovery, loyalty, and payments integrated into a single screen.

Website-based bookings remain relevant for multi-room groups and policy-heavy corporate itineraries, where larger screens and side-by-side comparisons increase confidence before purchase. AI-enabled search on domestic travel platforms improves result relevance across both the app and the web, and these features often launch first on mobile before being adapted for desktop. Property-side systems now also integrate chat and dynamic packaging tools that streamline higher-touch workflows and free up desktop space during complex negotiations. The Japan online accommodation industry, therefore, maintains a pragmatic dual-channel equilibrium as platforms align product roadmaps and promotional calendars across devices. With 5G coverage still expanding and app features compounding, the balance continues to tilt toward mobile while desktop remains critical for specific planning scenarios.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Mode of Booking: Third-Party Portals Hold Majority as Vacation Rentals via Platforms Surge

Third-party online portals accounted for 61.10% of the booking mix in 2025, reflecting the power of aggregated comparisons, ratings, and loyalty incentives shown at the point of sale. Within this mix, vacation rentals via third-party platforms are the fastest-growing subcategory with a 13.72% trajectory through 2031, supported by improved compliance verification and the professionalization of supply. Direct and captive portals remain valuable for brand-loyal guests and negotiated corporate contracts, but third-party discovery engines continue to capture high-intent shoppers comparing hotels and rentals. Partnerships between global hotel chains and domestic aggregators extend reach to younger mobile-first travelers, highlighting how distribution pragmatism complements brand-direct strategies. As a result, the Japan online accommodation market sustains a balanced mode split that favors third-party portals for breadth while preserving direct channels for loyalty and corporate use cases.

Transport-linked ecosystems deepen the prominence of third-party inventory by embedding hotels and rentals inside airline and rail apps where users already plan and pay for trips. Platform outlooks from leading aggregators also show faster growth in secondary destinations, which supports algorithmic discovery of long-tail properties that direct portals struggle to promote. Airline partnerships that rely on API connections to hotel platforms allow carriers to expand ancillary revenue without building complex supplier systems, while preserving points and wallet benefits at checkout. As these integrations scale, third-party portals build defensibility through network effects and loyalty interoperability across transport and lodging. These dynamics keep third-party platforms central to conversion in the Japan online accommodation market, even as direct channels refine user experience for existing customers.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Property Type: Hotels Dominate but Vacation Rentals Post Highest Growth

Hotels and resorts accounted for 46.75% in 2025 on the back of business demand in Tokyo and Osaka, and international travelers seeking standardized service with loyalty benefits. Vacation rentals are projected to grow at 15.11% through 2031 as families and long-stay guests seek multi-bedroom layouts and kitchens at competitive price points. The national verification system for private lodging listings increases confidence in rental quality and compliance, which is necessary for institutional participation and professional management growth. Platform-supported co-hosting and operations outsourcing lower barriers for new supply, improving responsiveness to seasonal and event-driven demand shifts in regional markets. These developments strengthen alternatives without displacing the core role that hotels play in premium leisure, meetings, and corporate travel within the Japan online accommodation market.

Institutional partnerships that add purpose-built flexible-stay apartments expand professionally managed inventory and reduce reliance on fragmented peer-to-peer supply. Revenue science capabilities continue to advance across hotels and rentals as vendors integrate dynamic pricing and competitive monitoring into property stacks accessible to independents. Case studies show that material RevPAR lifts for properties that adopt algorithmic pricing tools, helping smaller operators compete on yield with chains. As content quality, pricing sophistication, and compliance converge, travelers can more easily compare formats and select by trip purpose and party size, improving overall matching efficiency. These matching supports across formats in the Japan online accommodation market as each segment serves distinct, durable use cases.

Geography Analysis

Kanto is the largest region, accounting for 36.44% in 2025, sustained by Tokyo’s role as the country’s commercial and governmental center and by the region’s international gateways, which capture a high share of inbound flows. Japan’s inbound arrivals reached a record monthly level in December 2025, and Kanto’s connectivity channeled a significant portion of these stays into mobile-led booking journeys. National policy in 2026 focuses on dispersing tourism and investing in regional capacity, which moderates peak pressure in central wards while promoting travel to surrounding prefectures. Dense rail networks and strong 5G performance support last-minute bookings and micro-neighborhood discovery across weekdays and shoulder seasons. These features keep Kanto central to the Japan online accommodation market even as some peripheral regions outpace it on growth rates from a smaller base.

Kansai ranks second by size and demonstrated strong occupancy through the six-month Expo period that ended in mid-October 2025, validating event-driven demand concentration. Elevated RevPAR and limited slack during large-scale events underscore the importance of algorithmic pricing and diversified distribution for local operators. Kyoto’s residential-area limits for private lodgings further channel demand into licensed hotels and ryokans during high season and special events. As 2026 progresses, operators focus on staffing and yield strategies to manage spikes while aligning with heritage-preservation priorities that shape supply pipelines. These conditions reinforce a premium for compliance, technology adoption, and loyalty integration in the Japan online accommodation market within Kansai.

Hokkaido and Tohoku benefit from winter sports, nature-led travel, and revitalization programs that place professionals in smaller municipalities for extended periods. Kyushu and Okinawa are projected to be the fastest-growing region at 9.23% through 2031 as wellness and beach travel expand and as proximity to key source markets supports repeat visitation. International arrivals from nearby countries favored Kyushu gateways in 2025, strengthening the case for targeted promotions and instant confirmation in local inventory. National verification for private lodging increases the viability of rental supply in coastal prefectures where family travelers seek multi-bedroom options unavailable at scale in dense urban cores. These factors together broaden regional participation in the Japan online accommodation market and support a more balanced national growth profile.

Competitive Landscape

The Japan online accommodation market in 2026 remains moderately concentrated, with domestic platforms defending their share through loyalty ecosystems, deep regional inventory, and rapid product iteration. Rakuten Travel expanded global inventory in late 2025 to improve one-stop convenience for outbound and inbound travelers within a single points platform. Super-app distribution with integrated wallets like PayPay compresses checkout steps and increases the frequency of promotional events that drive engagement and repeat behavior. Revenue science providers and enterprise tech firms have made dynamic pricing and merchandising tools more accessible to independents, narrowing performance gaps with chains. These dynamics increase the importance of loyalty, payments, and pricing capabilities as primary levers for share defense within the Japan online accommodation market.

Strategic moves since 2025 have focused on consolidation and ecosystem building, centered on pricing, supply professionalization, and operational integration. A 2025 acquisition added an AI pricing specialist to a larger technology portfolio, which accelerates the deployment of automated revenue systems across property types. A 2025 partnership between a leading platform and a major developer will add purpose-built, flexible-stay apartments from 2026, expanding professionally managed rental supply. Rakuten integrated its branded lodging operations into the parent company in early 2026 to streamline resources and speed feature development across the travel stack. These steps compress innovation cycles and reward platforms that can integrate discovery, pricing, payments, and loyalty in the Japan online accommodation market.

Airlines and travel integrators now play larger roles as distribution and loyalty partners for accommodation platforms through API-driven inventory and in-app bundles. Aggregators highlight rising demand in secondary destinations, which supports algorithmic discovery of long-tail properties beyond the top metros. Super-app integrations that pair rail reservations with lodging lower friction for multi-city trips and raise cross-sell opportunities in regional hotels and rentals. As these ecosystems mature, platform scale and embedded payment rails are set to determine which players compound share in the Japan online accommodation market. The competitive focus in 2026 is on deepening loyalty value, expanding compliant supply, and deploying AI-led merchandising to sustain margin in a price-sensitive environment.

Japan Online Accommodation Industry Leaders

Rakuten Travel

Booking.com

Expedia Group Inc.

Agoda Company Pte. Ltd.

Jalan (Recruit Co.)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: Rakuten Travel expanded worldwide hotel booking inventory to over 400,000 international properties, enabling Japanese travelers to accumulate Rakuten Points on outbound trips while offering inbound visitors seamless booking within an ecosystem that includes dining, transport, and entertainment services.

- September 2025: Rakuten Travel launched an AI Hotel Search agent providing tailored recommendations based on user browsing history, loyalty tier, and stated preferences, leveraging natural language processing to accept voice queries and delivering personalized results that increase conversion rates by surfacing properties aligned with individual travel styles.

- August 2025: Airbnb, Inc. announced a partnership with Daiwa House Industry to develop "Sumu powered by Airbnb Partners" apartments opening in autumn 2026, marking institutional capital's entry into purpose-built short-term rental inventory designed from inception for flexible booking rather than traditional long-term leases, addressing supply constraints that fragmented peer-to-peer hosting cannot resolve at scale.

- February 2025: ANA X Inc. partnered with Fujitsu and Toshiba Data Corporation for a CO2 reduction pilot using the ANA Pocket app to track user mobility patterns and incentivize low-carbon transport choices, aligning with ESG mandates and differentiating ANA's travel services as environmentally responsible options for corporate procurement departments facing sustainability reporting requirements.

Japan Online Accommodation Market Report Scope

Online accommodation refers to the lodging booked online by travelers for a stay. Travelers can choose from the various available accommodations such as hotels, hostels, resorts, vacation rentals, etc. Accommodation can be booked through various sources, which include online travel agencies, hotel websites, booking through agents, and direct bookings.

The Japan online accommodation market report is segmented by platform (mobile application, website), mode of booking (third-party online portals, direct/captive portals), property type (hotels & resorts, vacation rentals, hostels & budget accommodations, alternate lodgings), and geography (Kanto, Kansai, Chubu, Hokkaido & Tohoku, Chugoku & Shikoku, Kyushu & Okinawa). The market forecasts are provided in terms of value (USD).

By Platform

| Mobile Application |

| Website |

By Mode of Booking

| Third-party online portals |

| Direct/captive portals |

By Property Type

| Hotels & Resorts |

| Vacation Rentals |

| Hostels & Budget Accommodations |

| Alternate Lodgings (Glamping, Farm-stays) |

By Geography

| Kanto |

| Kansai |

| Chubu |

| Hokkaido & Tohoku |

| Chugoku & Shikoku |

| Kyushu & Okinawa |

| By Platform | Mobile Application |

| Website | |

| By Mode of Booking | Third-party online portals |

| Direct/captive portals | |

| By Property Type | Hotels & Resorts |

| Vacation Rentals | |

| Hostels & Budget Accommodations | |

| Alternate Lodgings (Glamping, Farm-stays) | |

| By Geography | Kanto |

| Kansai | |

| Chubu | |

| Hokkaido & Tohoku | |

| Chugoku & Shikoku | |

| Kyushu & Okinawa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the outlook for the Japan online accommodation market to 2031?

The Japan online accommodation market size is USD 3.36 billion in 2026 and is projected to reach USD 4.73 billion by 2031 at a 7.06% CAGR, supported by mobile-first adoption, inbound recovery, and platform innovation.

Which booking platform is leading in Japan's lodging ecosystem?

Mobile applications lead with 67.16% in 2025 and are projected to grow at 11.55% through 2031 as 5G coverage and wallet-linked promotions sustain high conversion on apps.

How are regulations affecting vacation rentals in Japan?

A national verification system, effective April 1, 2026, aligns platform listings with official registrations and supports more consistent enforcement alongside municipal overlays such as Kyoto's residential-area limits.

Which regions are set to grow fastest through 2031?

Kyushu and Okinawa have the fastest growth projection at 9.23% through 2031, while Kanto remains the largest base due to Tokyo's connectivity and demand depth.

What technologies are improving pricing performance for properties?

Dynamic pricing and revenue science tools delivered through cloud APIs and property integrations are raising RevPAR for adopters, supported by acquisitions and vendor deployments that scale access for independents.

How are super-apps influencing competition?

Integrations like Yahoo! Travel with PayPay streamline checkout and consolidate discovery in a few high-frequency apps, compressing margins and raising the importance of loyalty and wallet interoperability.