Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

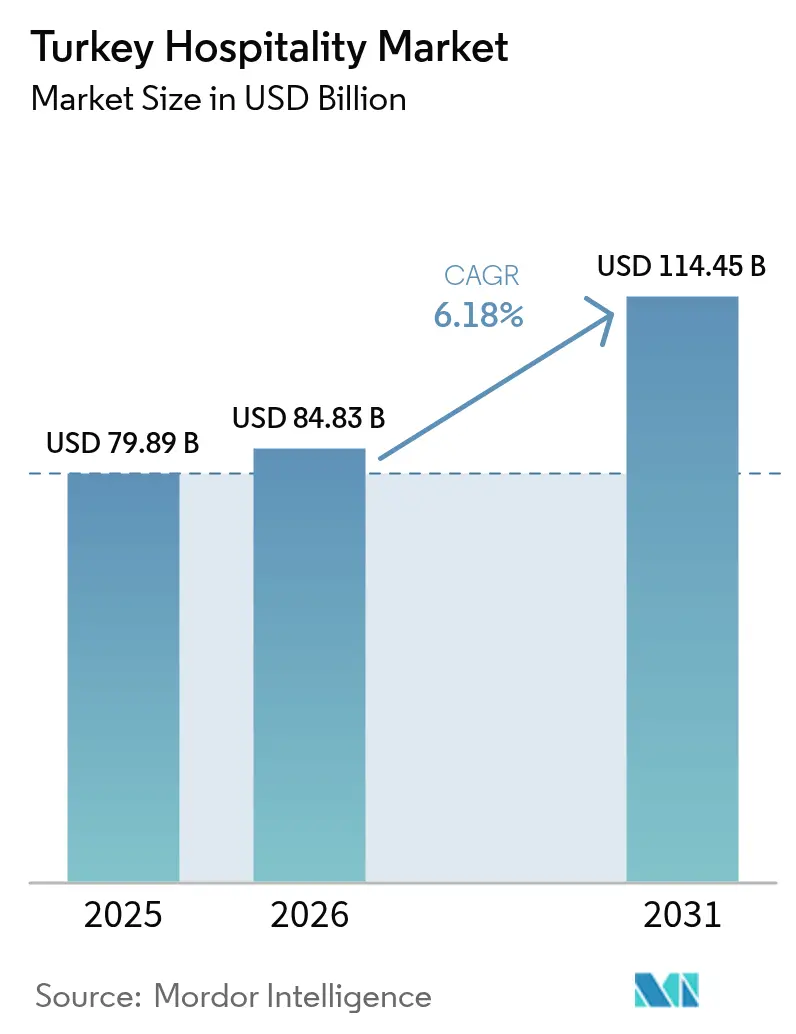

| Base Year Market Size (2025) | USD 79.89 Billion |

| Market Size (2026) | USD 84.83 Billion |

| Market Size (2031) | USD 114.45 Billion |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

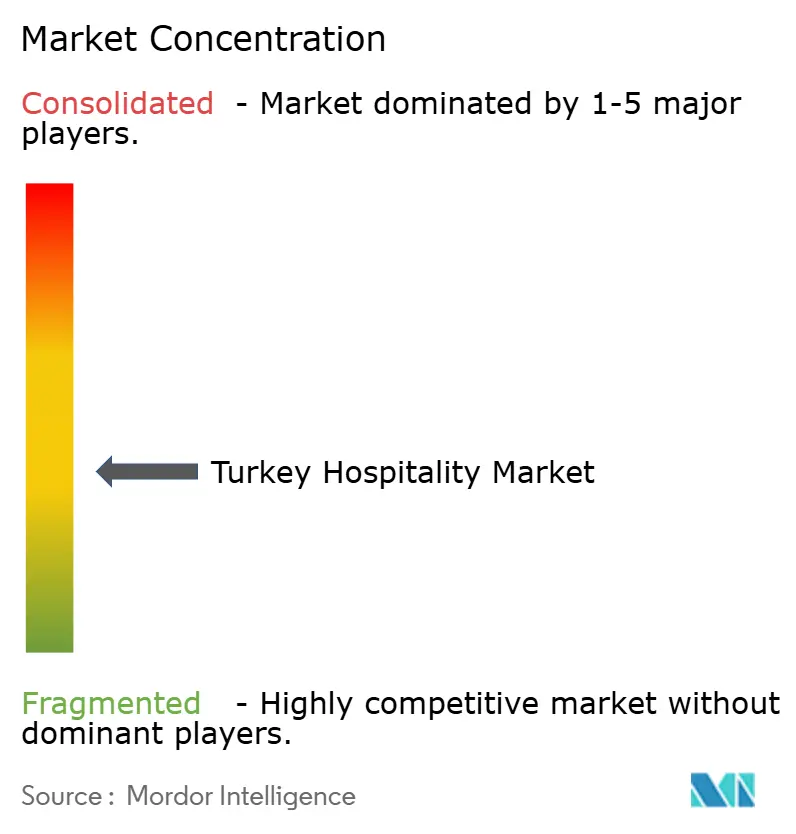

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Hospitality Market Analysis by Mordor Intelligence

The Turkey hospitality market size stood at USD 79.89 billion in 2025 and is projected to reach USD 84.83 billion in 2026 and USD 114.45 billion by 2031, reflecting a 6.18% CAGR. In 2025, Turkey welcomed 63.94 million visitors, a 2.7% increase from 2024, and generated USD 65.23 billion in tourism receipts, surpassing the Medium-Term Program target and highlighting the sector’s resilience to lira volatility. Average nightly spend rose 3.7% to USD 100, indicating a shift toward higher-value travel segments and premium experiences.[1]112.ua, “Resting in Turkey will become more expensive: forecast for 2025,” 112.ua Market growth is driven by rising international arrivals, increasing demand for luxury and experiential travel, and strong government support through initiatives such as the Istanbul Incentives program extended through 2028, which encourages hotel construction and investment in heritage-tourism assets. Operators are also optimizing distribution strategies in response to the EU Digital Markets Act, improving efficiency and profitability. Overall, the Turkey hospitality market shows robust growth potential, supported by favorable policy measures, strategic infrastructure investments, and evolving traveler preferences.

Key Report Takeaways

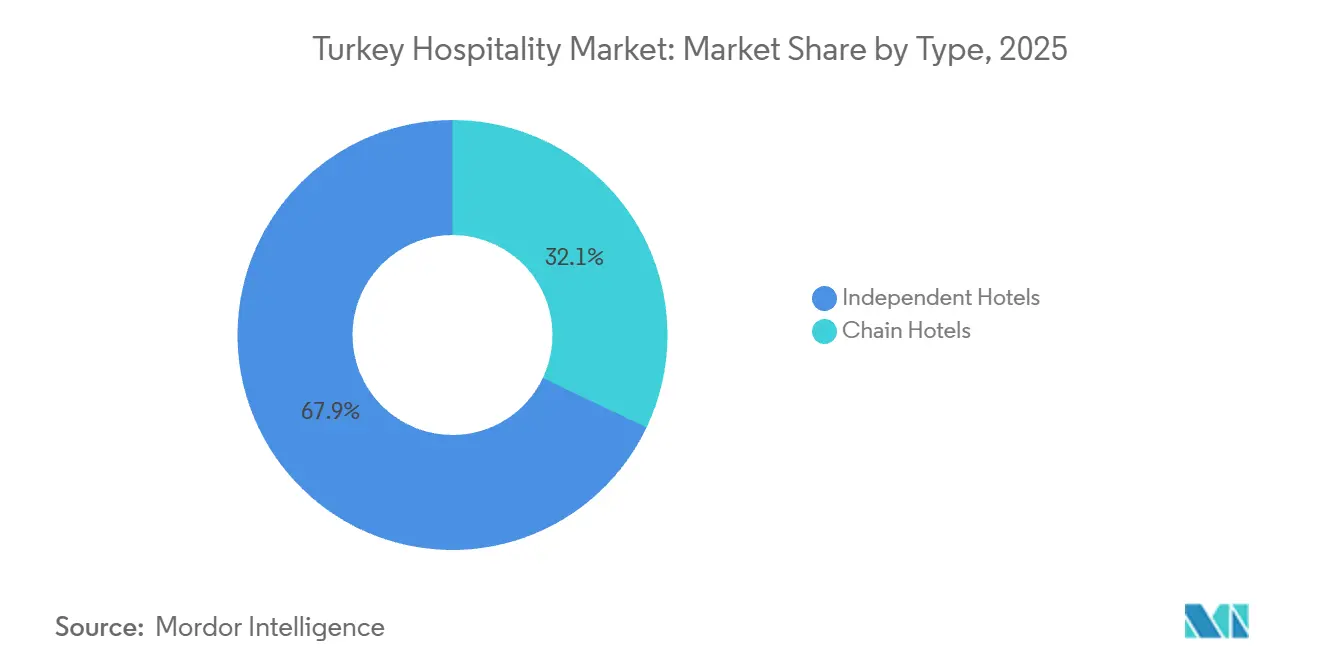

- By type, independent hotels held 67.92% of Turkey hospitality market size in 2025, while chain hotels are projected to grow at a 5.71% CAGR through 2031.

- By accommodation class, mid and upper-mid-scale led with 46.88% of Turkey hospitality market size in 2025, while service apartments are forecast to expand at a 7.82% CAGR to 2031.

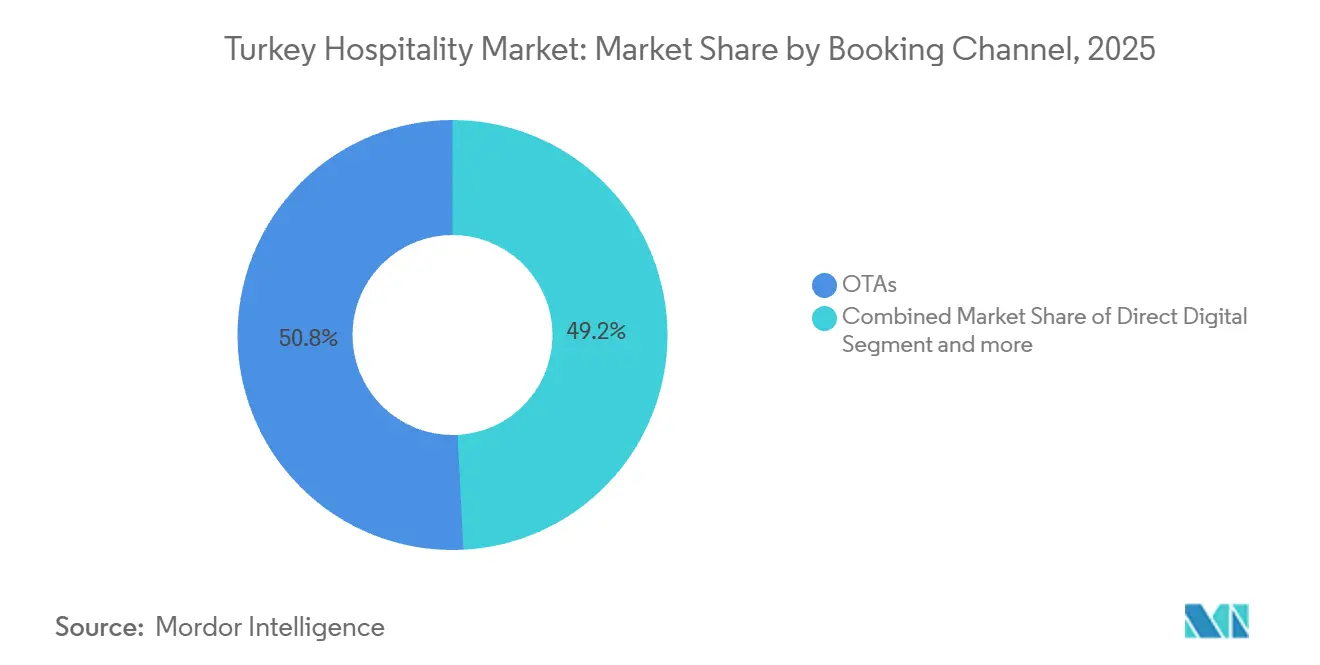

- By booking channel, OTAs commanded 50.81% of Turkey hospitality market size in 2025, while direct digital channels are expected to grow at a 9.66% CAGR through 2031.

- By geography, Marmara, including Istanbul, held 38.07% of Turkey's hospitality market size in 2025, while Central Anatolia is poised for a 6.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Turkey Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diversification of inbound source markets | +1.2% | Global, with early gains in Spain, Italy, Ireland, the USA, Canada, China, Japan, South Korea | Medium term (2-4 years) |

| Government investment and VAT-rebate incentives for new builds | +1.5% | National, concentrated in the underserved Eastern and Southeastern Anatolia, Black Sea. | Long term (≥ 4 years) |

| Expanded international air-route connectivity via Istanbul Airport | +1.8% | Global, with the strongest pull in Europe, the Middle East, and Asia | Short term (≤ 2 years) |

| Advanced revenue-management and dynamic-pricing adoption | +0.9% | Urban hubs such as Istanbul, Ankara, Antalya, Izmir, and chain properties | Short term (≤ 2 years) |

| Medical and wellness tourism are filling shoulder seasons | +1.3% | National hotspots such as Istanbul, Antalya, Izmir, Bursa, Afyon, and Yalova, are drawing GCC and European demand | Medium term (2-4 years) |

| Halal-certified hotel demand from GCC travellers | +0.7% | Mediterranean coast, including Antalya and Alanya, Marmara, Aegean, and heritage destinations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Diversification of Inbound Source Markets

A key growth driver for the Turkey hospitality market is the diversification of its inbound source markets, which reduces reliance on any single region and strengthens sector resilience. In 2025, Russia, Germany, and the United Kingdom remained the top contributors, while increasing arrivals from other European, Middle Eastern, and Asian markets broadened the visitor base. Combined with Turkey’s mix of coastal, cultural, and heritage destinations, this geographic diversity has supported stable tourism revenues, higher hotel occupancy, and sustained growth in the hospitality sector. [2]Source: Investment Office of the Presidency of the Republic of Türkiye, “Tourism - Invest in Türkiye,” Invest in Türkiye, invest.gov.tr. Istanbul Airport’s network scale, with 309 non-stop destinations and a 59% increase in hub connectivity since 2019, enabled more direct itineraries and time-efficient transfers, raising short-stay propensity and broadening origin markets. Enhanced airport service quality signaled alignment with premium traveler expectations through internationally recognized accreditation and environmental standards. [3]Source: Press Office, “iGA Istanbul Airport: The world’s leading hub for global connectivity,” iGA Istanbul Airport, igairport. aero. This mix shift supported average spend and improved resilience to volatility across individual source countries, helping sustain the growth momentum of the Turkey hospitality market in 2025.

Government Investment & VAT-Rebate Incentives for New Builds

Government investment and incentive programs are a key driver of Turkey’s hospitality market growth. Extended VAT exemptions on construction goods and services have improved returns for new hotel developments. Subsidies for machinery and equipment, along with social-security support in targeted regions, further encourage investment in greenfield projects. Adaptive reuse of heritage assets benefits from favorable tax treatment, thereby promoting boutique hotels in underdeveloped areas. Streamlined incentives, land allocations, and infrastructure support increase investor confidence and expand development beyond traditional coastal hubs. Together, these measures create new demand nodes and strengthen the long-term growth prospects of the hospitality sector.

Expanded International Air-Route Connectivity via Istanbul Airport

Expanded international air route connectivity through Istanbul Airport has become a major driver of Turkey’s hospitality market. The airport now ranks first in Europe for connectivity, offering a growing number of non-stop global routes. Investments in runway infrastructure and operational capacity have increased hourly movements and improved airline scheduling flexibility. Both seasonal and year-round services by European and North American carriers reflect rising long-haul demand. These enhancements have converted more transit passengers into two- to three-night city breaks, boosting urban hotel occupancy. Strong network depth and reliable on-time performance reinforce Istanbul’s appeal as a gateway between Europe, the Middle East, and Asia. Overall, the airport’s expanded connectivity supports incremental demand across both leisure and business travel segments, strengthening the broader hospitality market.

Advanced Revenue-Management & Dynamic-Pricing Adoption

Chain operators accelerated the deployment of AI-enhanced revenue-management systems that ingest rate and demand signals to refine pricing in near real time. Properties leveraged integrations with booking engines and loyalty platforms to cycle higher-value bookings through direct channels while retaining visibility on third-party platforms. Hotels combined IoT-based energy control and touchless check-in with dynamic pricing rules to protect margins in a high-inflation environment. These tools compressed response times to currency fluctuations and event-driven demand surges, while enabling targeted offers that improved conversion and Net Promoter Scores. The net effect reinforced pricing power and channel-mix optimization across urban hubs, supporting the Turkey hospitality market in 2025 and into 2026.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Turkish-lira volatility compressing RevPAR | -1.1% | National, particularly debt-exposed chain operators and importers of F&B and linen | Short term (≤ 2 years) |

| Rising labour and energy costs outpacing ADR growth | -0.9% | National, most acute in Istanbul, Antalya, and Izmir, with high labour density | Short term (≤ 2 years) |

| Elevated insurance premiums after the 2023 Kahramanmaraş quakes | -0.5% | Eastern Anatolia with spill-over to Central Anatolia | Medium term (2-4 years) |

| The EU Digital Markets Act is raising OTA distribution costs | -0.4% | Urban properties with high OTA reliance in Istanbul, Bodrum, and coastal resorts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Turkish-Lira Volatility Compressing RevPAR

Currency volatility in early 2025 posed a significant restraint on the Turkey hospitality market. While lira depreciation temporarily boosted nominal average daily rates (ADRs), real revenue per available room (RevPAR) growth lagged due to reduced domestic purchasing power, lower leisure travel frequency, and increased corporate cancellations. Rising costs for import-dependent inputs such as food and beverages, linens, and technology further squeezed operators with Turkish lira revenue streams and foreign currency liabilities.[4]Source: Turkish Statistical Institute, “Tourism Statistics,” TUIK, tuik.gov.tr. Limited currency-hedging options put additional pressure on independent hotels, forcing many to prioritize liquidity over planned capital investments. Lenders also imposed stricter risk premiums on financing for new builds and conversions amid macroeconomic uncertainty. Collectively, these factors constrained pricing flexibility and RevPAR growth, dampening overall market performance in 2025.

Rising Labour & Energy Costs Outpacing ADR Growth

Rising labor and energy costs continue to constrain the hospitality market in Turkey. The net minimum wage increased significantly in 2026, raising total employer payroll expenses when social security and unemployment contributions are included. Persistent price inflation in hotels, restaurants, and cafes, combined with competitive pressures and currency fluctuations, has limited operators’ ability to pass costs onto room rates. Energy-cost volatility, particularly in electricity and gas, remains a concern for multi-site hotel operators. Additionally, shortages of skilled labor in IT, culinary, and front-office roles in key markets such as Istanbul, Antalya, and Izmir have intensified wage pressures. While larger hotel chains have partially mitigated these challenges through automation and AI-enabled tools, smaller independent operators without similar capital flexibility have faced margin compression, limiting profitability and growth in the sector.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Independent Hotels Yield Ground to Chain Efficiency

Independent hotels held 67.92% in 2025, reflecting the enduring pull of locally rooted experiences and owner-operator agility across coastal and heritage destinations. Chain hotels are projected to grow at a 5.71% CAGR through 2031 as loyalty ecosystems, direct-booking engines, and centralized tools support conversion and pricing consistency across multi-asset portfolios, which contributes to the Turkey hospitality market’s operating discipline. Global brands expanded outside tier-one cities, with Marriott, Hilton, IHG, Accor, and Radisson deepening their reach through conversions, management contracts, and franchises tied to new and adaptive reuse projects. Chain penetration into secondary markets clustered around heritage circuits, infrastructure links, and mixed-use nodes, which created brand presence in locations previously dominated by independents. ISO-aligned reporting and sustainability frameworks strengthened investor confidence for chains, while independents accelerated adoption of SaaS-based RMS and white-label loyalty tools to narrow capability gaps in the Turkey hospitality market.

Independent portfolios leveraged local culinary and design narratives to defend rate premiums in destinations like Cappadocia and Bodrum, while chains optimized channel mix and RevPAR through scale advantages. Adaptive-reuse incentives under the national framework aided both models, with boutique conversions and soft brands enabling differentiation within standardized group distribution. Integration of data-protection and ESG protocols became more formalized under chain programs, while independents relied on third-party certifications to meet buyer expectations. As corporate and leisure demand evolve, both formats continue to play roles in customer segmentation and product diversity in the Turkish hospitality market. The interplay of brand reach and independent authenticity supports a balanced pipeline aligned to region-specific opportunities across 2026 and beyond.

Note: Segment shares of all individual segments available upon report purchase

By Accommodation Class: Mid & Upper-Mid-Scale Anchor, Service Apartments Surge

Mid and upper-mid-scale properties captured 46.88% in 2025 and continued to anchor demand from business travelers, MICE groups, and value-seeking leisure guests who prioritize quality and predictability. Luxury remains supply-constrained and focused on Istanbul’s Bosphorus corridor and Bodrum’s marina precincts, while budget and economy brands expand in secondary cities to serve domestic and regional travel. Service apartments are forecast to grow at a 7.82% CAGR through 2031, driven by rising digital nomad stays, medical travel recovery, and corporate long-stay assignments. Extended-stay formats integrated kitchens, laundry, and flexible leases to meet remote work preferences and family needs, adding resilience to occupancy in off-peak cycles in the Turkey hospitality market. Operators benefited from incentives that support efficient asset classes in targeted locations, thereby improving the feasibility of conversions and mixed-use developments.

New developments from global brands enhanced product variety, including executive apartments and upscale lifestyle hotels in mixed-use districts. Co-working options and business services near innovation corridors supported demand for mid- and upper-mid-scale and serviced-apartment formats. Operators aligned with Sustainable Tourism Program guidance and embedded halal-friendly amenities where relevant to capture GCC and Southeast Asian demand. As asset-light brands scale into new submarkets, the Turkey hospitality market gains more diverse stay options, improving capture rates across traveler cohorts. This balanced supply strategy supports rate integrity by matching format to travel purpose while maintaining coverage across price points through 2031.

By Booking Channel: OTAs Dominate, Direct Digital Accelerates

OTAs accounted for 50.81% of 2025 revenue, reflecting high trust in aggregation, broad visibility, and convenience for international comparison shopping. Direct digital channels are projected to grow at a 9.66% CAGR through 2031 as operators leverage parity-free pricing, loyalty benefits, and differentiated content to steer traffic to owned platforms. Chains used customer-data platforms, email marketing, and app-based engagement to deepen relationships and expand primary demand without intermediary commissions. Corporate and MICE bookings stabilized mid-week occupancy in major cities, while wholesale and traditional agents continued to serve package-tour segments in key source markets. Data protection processes supported consent-based personalization and safeguarded cross-border data flows, thereby maintaining credibility for automated decision-making in the Turkish hospitality market.

Hotels invested in metasearch participation and SEO to offset organic search shifts, pairing performance media with loyalty program value to raise direct conversion. AI chatbots stepped up multilingual support and streamlined queries, reducing response time and boosting service satisfaction scores. Facial recognition and mobile key solutions reduced front-desk staffing requirements during peak flows and late arrivals. Dynamic-pricing engines coordinated rate changes with events, flight data, and competitive moves to elevate RevPAR on owned channels. This channel evolution is expected to narrow the gap with OTAs by 2031 while enhancing the Turkey hospitality market’s profit mix.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Marmara generated 38.07% of Turkey hospitality market size in 2025, anchored by Istanbul’s finance clusters, global events, and transit tourism buoyed by Istanbul Airport’s network breadth. The metro extension to Gayrettepe slashes transfer times, stimulating revenge-spending layovers where passengers opt for Bosphorus cruises and designer shopping, thereby lengthening stays. Luxury supply intensifies with Fairmont, Raffles, and Mandarin Oriental openings that emphasize experiential positioning—Ottoman hammams, Michelin-star gastronomy, and curated art tours—that support premium ADR resilience even amid currency swings. Emerging sub-markets such as Galataport’s cruise terminal spawn micro-clusters of lifestyle boutique hotels that harvest demand from art fairs and tech conferences, sustaining room-rate integrity through diversified segment mix. Despite supply additions, occupancy remains buoyant thanks to city-wide marketing alliances that bundle museums passes and hop-on buses into easy-book packages targeting millennial travellers.

Central Anatolia posts the nation’s fastest 6.62% CAGR through 2031, powered by Cappadocia’s balloon safaris, underground cities, and UNESCO-listed rock chapels that magnetize high-spend experiential tourists seeking Instagram-worthy landscapes. Adaptive-reuse incentives spur entrepreneurs to carve cave suites equipped with radiant-heat floors and panoramic terraces, commanding ADR premiums north of USD 350 during peak fall foliage. Government promotion of cultural routes, such as the Hittite Heritage Trail, redirects traffic from oversaturated coastal resorts, distributing economic benefits inland. New charter flights and high-speed rail links compress travel times, unblocking latent demand from Asian tour groups that seek multi-city itineraries. This centrifugal force lifts regional RevPAR and diversifies the Turkey hospitality market’s geographic revenue footprint.

The Aegean and Mediterranean maintain resort appeal, with Didim’s EUR 150 million (USD 163.5 million) Anda Barut Collection uplifting local land values and catalysing luxury-brand scouting in previously mid-market zones. Antalya anticipates 17 million visitor arrivals in 2024, spurring Konyaaltı’s five-star pipeline that blends international brands with Turkish-owned lifestyle concepts. The Black Sea, Eastern, and Southeastern Anatolia regions focus on eco-tourism, tea plantations, hazelnut orchards, and mountaineering, though limited airlift and post-earthquake reconstruction constrain immediate scalability. Nonetheless, progressive infrastructure expansions, such as Rize-Artvin Airport and the Trans-Anatolian Railway, will open fresh corridors for domestic weekend explorers, incrementally enriching the Turkey hospitality market’s regional tapestry.

Competitive Landscape

The Turkey hospitality market remains moderately concentrated, with independent operators holding a strong position while global chains continue to expand room capacity, brand presence, and operational capabilities. International groups are pursuing growth through both conversions and new-build projects across gateway cities and secondary markets, often blending soft brands and lifestyle concepts to adapt to local preferences. Marriott has deepened its footprint in Istanbul and Cappadocia, while Hilton has expanded its lifestyle offerings and signed new properties in Antalya and Kocaeli. IHG has diversified its brand mix with voco, Garner, and resort concepts, and Radisson is steadily advancing toward its long-term expansion goals through targeted openings. Domestic hotel groups continue to leverage localized service, halal certification, and cost-control efficiencies to maintain competitiveness in regional markets.

Strategic development in secondary cities and heritage property conversions is increasingly supported by government incentives, thereby improving investment returns and encouraging portfolio diversification. Hilton’s lifestyle strategy includes Canopy openings and adaptive-reuse projects under the Tapestry Collection, while IHG has strengthened its leisure presence with a major Holiday Inn Resort signing in Bodrum. Marriott has scaled its experiential offerings in Cappadocia through the Autograph Collection to capture cultural tourism peaks, and Radisson is expanding into city-center and wellness-adjacent properties that serve both corporate and leisure travelers. These moves demonstrate a strategic balance between premium urban hotels, lifestyle-oriented properties, and family-focused resorts. Together, these developments reflect a market where chains grow through diversified portfolios while independents continue to compete in niche and heritage-driven segments.

Technology, operational standards, and sustainability practices have become key differentiators in Turkey’s hospitality market. Large chains are increasingly integrating AI-enabled service tools, dynamic pricing systems, and energy-management technologies to enhance efficiency and improve guest experiences. Service automation, from digital check-in to chatbot support, complements labor-productivity initiatives and operational consistency across multiple properties. Enhanced data governance, ESG reporting, and sustainability compliance have improved access to corporate contracts and institutional capital. This combination of scale, brand equity, and advanced operating systems supports continued share growth for chains, while independents maintain premium positioning through design-led and heritage-focused offerings.

Turkey Hospitality Industry Leaders

Accor S.A.

Marriott International Inc.

Hilton Worldwide Holdings Inc.

InterContinental Hotels Group PLC (IHG)

Wyndham Hotels & Resorts Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Hilton launched Elika Cave Suites Cappadocia, Curio Collection by Hilton, a 36-room property in Ortahisar featuring a bar, roof terrace, restaurant, spa, one outdoor and three indoor pools, and a gym, marking Hilton's first cave hotel and reinforcing Cappadocia's heritage-tourism appeal following UNESCO-site designations.

- March 2026: Hilton opened Hilton Istanbul Airport, a 485-room property within Istanbul Airport featuring OXBO Restaurant, OXBO Café, OXBO Bar, a spa, an indoor pool, and an executive lounge, capitalizing on the airport's status as the world's most connected hub (309 non-stop destinations) to capture transit-passenger conversions into short city stays.

- January 2026: Hilton Istanbul Bosphorus completed a landmark renovation, unveiling 475 guest rooms (including 39 suites) with balconies, a new lobby lounge and terrace, a jazz bar, dining venues, an executive lounge, a large outdoor pool, and a health club and spa, after a two-year project that preserved the 1955 property's architectural heritage while integrating modern amenities.

- January 2026: Marriott International opened Fortuna of Cappadocia, Autograph Collection, a 153-villa and suite property in Cappadocia, drawing design inspiration from the Roman Goddess of Fortune, blending authentic textures with contemporary elegance, panoramic views, and proximity to landmarks like fairy chimneys and hot-air balloon launch sites.

Turkey Hospitality Market Report Scope

Hospitality encompasses the warm and generous reception and the entertainment of guests, visitors, or strangers. This practice involves serving guests across diverse sectors, including hotels, restaurants, bars, and the broader hospitality industry. The hospitality in Turkey market forecast is segmented by type and segmentation. By type, the market is segmented into chain hotels and independent hotels. By segment, the market is segmented into service apartments, budget and economy hotels, mid and upper-mid-scale hotels, and luxury hotels. The report offers the market size of hospitality in Turkey in value terms in USD for all the abovementioned segments.

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region

| Marmara (incl. Istanbul) |

| Aegean |

| Mediterranean |

| Central Anatolia |

| Black Sea |

| Eastern Anatolia |

| Southeastern Anatolia |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | Marmara (incl. Istanbul) |

| Aegean | |

| Mediterranean | |

| Central Anatolia | |

| Black Sea | |

| Eastern Anatolia | |

| Southeastern Anatolia |

Key Questions Answered in the Report

What is the current size and growth outlook for the Turkey hospitality market?

The Turkey hospitality market size was USD 79.89 billion in 2025 and is projected to reach USD 114.45 billion by 2031 at a 6.18% CAGR.

Which segments lead by type, and how will growth vary by 2031?

Independent hotels held 67.92% in 2025, while chain hotels are projected to grow at a 5.71% CAGR through 2031 as brand systems scale.

How are booking channels evolving in Türkiye’s accommodation sector?

OTAs held 50.81% in 2025, while direct digital channels are expected to expand at a 9.66% CAGR through 2031 as parity-free pricing and loyalty benefits gain traction.

Which regions currently anchor performance and which will grow fastest?

Marmara, including Istanbul, held 38.07% of 2025 revenue, while Central Anatolia is forecast to see a 6.62% CAGR to 2031 as heritage and infrastructure projects scale.

What factors are most supportive of demand in 2026?

Expanded air-route connectivity, medical and wellness tourism, inbound diversification, and incentives for hotel investments are supporting demand in 2026.

What are the key operating headwinds for hotels in Türkiye?

Lira volatility, wage and energy cost pressures, seismic insurance costs, and higher-paid media needs after DMA-related search changes are the main headwinds.

Page last updated on: