Market Overview

| Study Period | 2020 - 2031 |

|---|---|

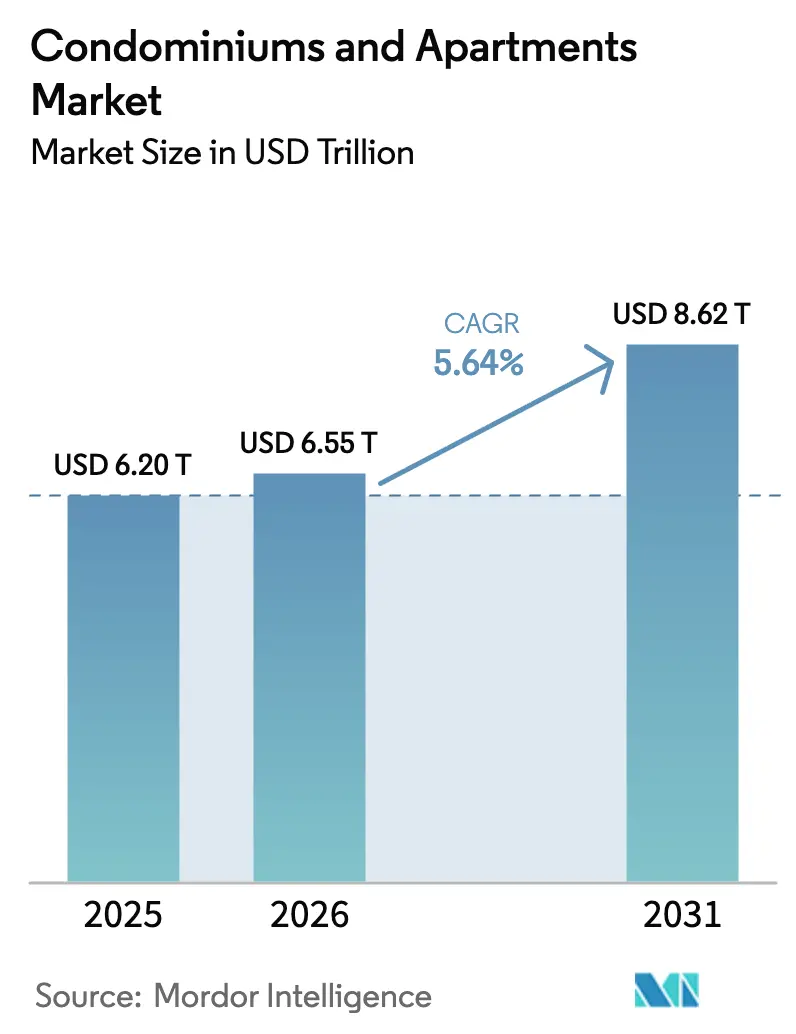

| Market Size (2026) | USD 6.55 Trillion |

| Market Size (2031) | USD 8.62 Trillion |

| Growth Rate (2026 - 2031) | 5.64% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Condominiums And Apartments Market Analysis by Mordor Intelligence

The Condominiums And Apartments Market size is projected to be USD 6.20 trillion in 2025, USD 6.55 trillion in 2026, and reach USD 8.62 trillion by 2031, growing at a CAGR of 5.64% from 2026 to 2031.

Rising urbanization, persistent housing-affordability gaps, and expanding institutional appetite for income-generating residential assets are the main forces shaping the global landscape. Asia-Pacific retained clear leadership in 2025, capturing 38.4% of revenue as China, India, and Southeast Asia added record urban households. Luxury high-rise launches in Dubai, Riyadh, and Tokyo underline the importance of amenity-rich towers, while sovereign megaprojects in the Gulf push frontier growth. Developers face tighter financing and elevated input costs, yet investor demand for resilient rental cash flows continues to back new multifamily supply.

Key Report Takeaways

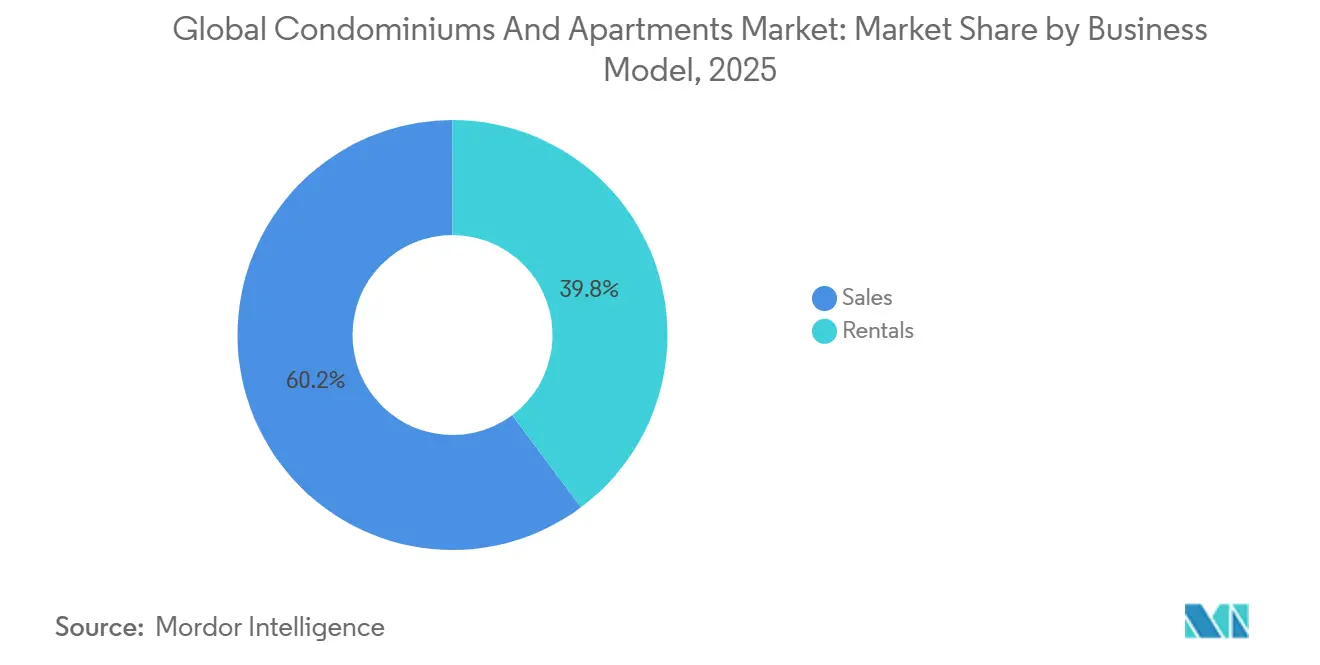

- By business model, the sales segment led with a 60.2% share of the condominiums and apartments market in 2025, whereas the rental segment is set to expand at a 6.05% CAGR through 2031.

- By price band, mid-market units held 42.7% of the condominiums and apartments market share in 2025; luxury properties are forecast to post the fastest 6.15% CAGR to 2031.

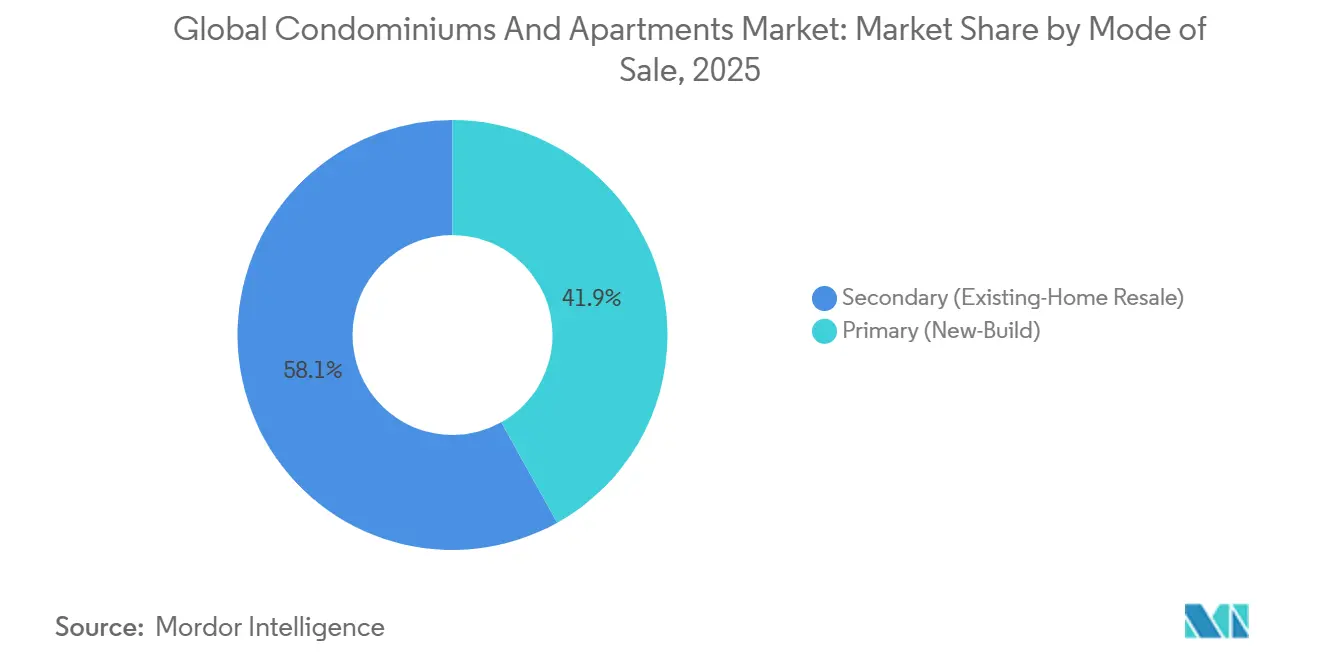

- By mode of sale, secondary transactions accounted for 58.1% of the condominiums and apartments market size in 2025, while primary new builds are projected to grow 6.24% annually to 2031.

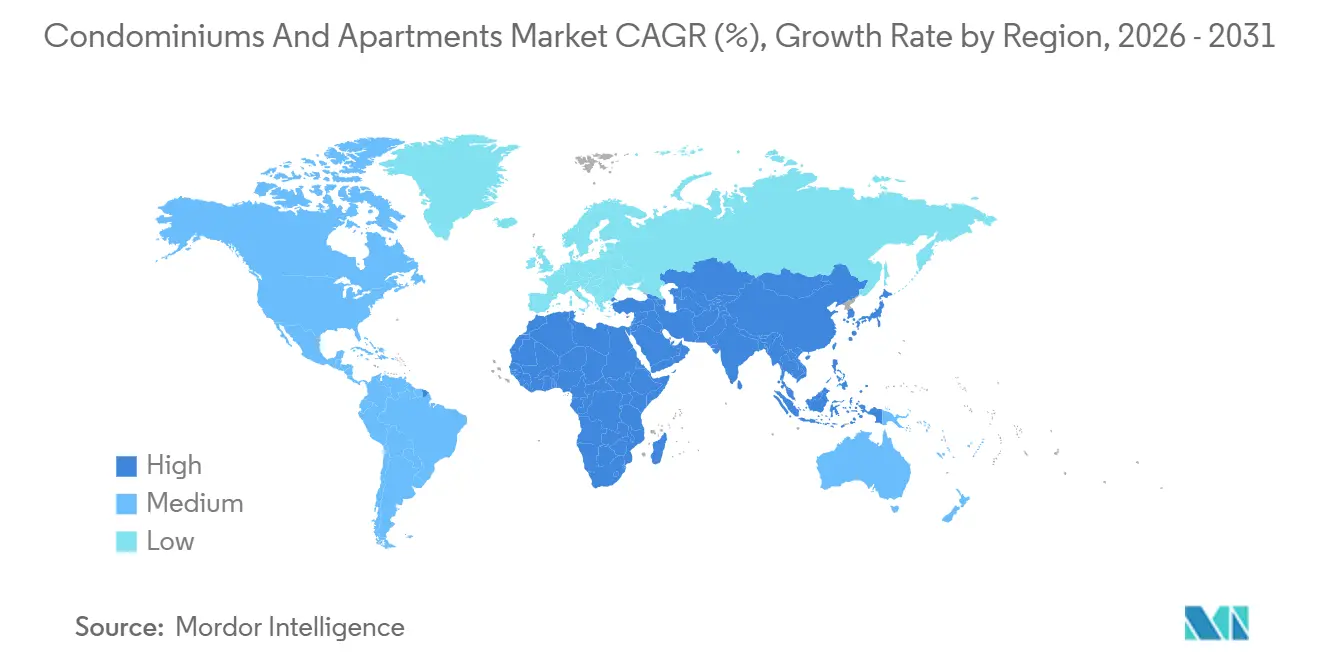

- Asia-Pacific captured 38.4% of global revenue in 2025; the Middle East & Africa region is expected to be the quickest-growing geography at a 6.53% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Condominiums And Apartments Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Housing affordability constraints are increasing the preference for multi-family living | +1.2% | Global (acute in North America, Europe, tier-1 Asia-Pacific cities) | Medium term (2-4 years) |

| Limited land availability in prime urban zones supports vertical residential projects | +1.0% | Tokyo, Shanghai, Mumbai, London, Paris, New York | Long term (≥ 4 years) |

| Expansion of build-to-rent and professionally managed rental portfolios | +0.9% | North America, Europe, Australia, emerging Middle East | Medium term (2-4 years) |

| Rising investor interest in income-generating residential assets | +0.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Demand for lifestyle amenities and community living is boosting apartment absorption | +0.7% | Global (the strongest luxury tiers in Asia-Pacific and the Middle East) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Housing Affordability Constraints Increasing Preference for Multi-Family Living

Soaring home prices vis-à-vis stagnant median wages are redirecting urban households toward condominium and apartment market offerings. In 2025, median single-family prices in multiple U.S. gateway metros surpassed eight times the median income, mirroring Tokyo’s pivot, where the share of new units priced above USD 680,000 rose markedly. Developers counter by shrinking average floorplates and experimenting with co-living designs, yet these adjustments only partially bridge the affordability gap. Consequently, multi-family formats remain the de facto entry point for new city dwellers, a trend likely to underpin steady absorption through 2031. Policymakers are responding with subsidized mortgage programs and VAT exemptions to widen access without derailing prices[1]Ministry of Finance of the People’s Republic of China, “Monthly Property Market Data,” Ministry of Finance, mof.gov.cn.

Limited Land Availability in Prime Urban Zones Supporting Vertical Residential Projects

Core districts across Asia-Pacific and leading European capitals have almost exhausted developable land, compelling developers to build upward rather than outward. Tokyo developers trimmed land acquisitions for condominiums to less than half of 2023 levels in 2025, focusing capital on scarce, transit-rich parcels where vertical towers can command price premiums. The pattern repeats in Shanghai, London, and New York, where zoning favors high-rise density to maximize scarce footprints. Vertical construction boosts project complexity and cost, tilting competitive advantage toward firms with engineering scale and balance-sheet strength. Heightened demand for skyline properties should preserve premium pricing even during cyclical slowdowns[2]Tokyo Metropolitan Government, “Tokyo Condominium Market Statistics 2025,” Tokyo Metropolitan Government, toukei.metro.tokyo.jp.

Expansion of Build-to-Rent and Professionally Managed Rental Portfolios

Institutional investors have discovered the stable yield profile of multifamily rentals, accelerating the shift from mom-and-pop landlords to branded operators. China Vanke’s Boyu platform managed more than 270,000 units at 93% occupancy in 2025, while U.S. pension funds funneled billions into Sunbelt build-to-rent subdivisions. Mexico City validated the model by clearing USD 1.1 billion of rental-heavy projects via its new single-window approval in 2025. Professionalization enhances tenant experience, introduces smart-building tech, and diversifies developer income beyond one-off sales. Rent-backed cash flows also hedge inflation, a key attraction for long-horizon capital such as sovereign wealth funds[3]National Council of Real Estate Investment Fiduciaries, “Institutional Investment in Global Multifamily,” NCREIF, ncreif.org.

Rising Investor Interest in Income-Generating Residential Assets

Persistently low bond yields and volatile equities have rerouted global capital toward the condominium and apartment markets. In 2025, China Vanke’s operating-services revenue reached USD 6.0 billion, signaling resilience even as for-sale momentum softened. European and North American real-estate investment trusts accumulated multifamily pipelines exceeding USD 120 billion, betting on structural renter growth. The inflow forces developers to raise build quality, embed green features, and adopt data-driven asset management to meet institutional diligence. As more pension and insurance pools chase durable yields, multifamily cap rates are expected to remain compressed, supporting asset values.

Restraint Impact Analysis

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High interest rates and restrictive mortgage conditions are impacting buyer demand | -0.9% | North America, Europe, Australia | Short term (≤ 2 years) |

| Escalating construction and land costs are delaying new project launches | -0.7% | Global (acute in tier-1 Asia-Pacific and Europe) | Medium term (2-4 years) |

| Lengthy planning approvals and regulatory hurdles are slowing development cycles | -0.5% | Europe, North America, Japan, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Interest Rates and Restrictive Mortgage Conditions Impacting Buyer Demand

Policy-rate hikes maintained through 2025 lifted average 30-year fixed U.S. mortgage coupons near 7%, shrinking eligible borrower pools. Shanghai eased provident-fund loan rates to as low as 2.1% in 2026, but the cut only partly offsets earlier tightening. Across Canada and the U.K., higher debt-service ratios prolong decision times and force developers to sweeten incentives, eroding margins. Weaker credit uptake benefits rentals yet constrains pre-sale cash flows, increasing balance-sheet risk for highly levered builders. Rate relief expected from 2027 may revive sentiment, though recovery will trail monetary easing by several quarters.

Escalating Construction and Land Costs Delaying New Project Launches

Steel, cement, and labor prices remained 15%-20% above pre-pandemic levels in 2025, pushing turnkey costs higher. Record land premiums in Chengdu, where two central plots fetched USD 3,900 per square foot, illustrate pressure across prime Asian nodes. Developers deploy modular assemblies and value engineering to claw back margins, but mid-market affordability still narrows. Investors shift toward brownfield conversions and asset-light management contracts to sidestep cap-ex spikes. If material inflation persists into 2027, project pipelines could rebalance toward luxury and rental formats where cost pass-through is more feasible.

Segment Analysis

By Business Model: Sales Remains Dominant, Rentals Race Ahead

The sales segment commanded 60.2% of the condominiums and apartments market share in 2025, reaffirming embedded incentives in many tax codes. Developers capitalized on pent-up demand by completing 117,000 China Vanke units in 2025, delivering 16,000 ahead of schedule. Yet rentals are forecast to accelerate at a 6.05% CAGR, the fastest among all models, as Boyu, Greystar, and Europe-based Vonovia deploy scale playbooks. Rental income diversifies cash flows and smooths cyclicality, attracting pension and sovereign capital seeking steady coupons. Mexico City alone expects nearly USD 15 billion of rental-centric investment in 2026, highlighting rapid institutionalization.

Rental growth is strongest where affordability gaps and lifestyle flexibility heighten renter appeal. Younger cohorts delay ownership to prioritize career mobility, while retirees downsize to amenity-rich managed communities. Developers adapt by offering lease-to-own pathways and integrated property-management arms, embedding data analytics to refine occupant experience. Although sales will keep the headline share through 2031, recurring-revenue models are redefining valuation metrics and pushing listed developers to highlight net-operating-income multiples alongside traditional EBITDA.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Price Band: Mid-Market Anchors Volume, Luxury Unlocks Growth

Mid-market properties accounted for 42.7% of the condominiums and apartments market in 2025, providing the broadest appeal among dual-income households. This tranche balances livable unit sizes with moderate price points, underpinned by mortgage accessibility programs in India, Indonesia, and Brazil. Developers deploy modular layouts and standardized finishes to defend margins without diluting quality, while incorporating shared amenities to strengthen community feel.

Luxury units, however, are slated to record the swiftest 6.15% CAGR to 2031, buoyed by high-net-worth buyers chasing branded residences in Dubai, Riyadh, and Tokyo. Tokyo’s share of units priced above USD 680,000 rose sharply in 2025 as land scarcity favored premium vertical redevelopment. Gulf projects bundle concierge, wellness spas, and private marinas, commanding global investor interest and premium pre-sales. Rising wealth concentration and investment diversification motives ensure that luxury will continue to punch above its volumetric weight in profit contribution.

By Mode of Sale: Secondary Dominates Today, Primary Pipeline Builds

Secondary resales formed 58.1% of the condominiums and apartments market size in 2025, thanks to deep existing stock in mature cities such as Shenzhen, Tokyo, and New York. China’s 2026 VAT exemption for homes held over two years aims to unlock further liquidity, encouraging faster turnover. Resale buyers appreciate immediate move-in certainty and known building performance.

Primary sales are projected to expand at a 6.24% CAGR as urban cores crave new, tech-enabled stock. Vanke’s Sanya Bay scheme hit a 72.3% subscription rate upon its December 2024 launch, demonstrating appetite for “walk-in ready” completion models that remove construction-risk ambiguity. Infill redevelopments throughout Europe and suburban transit-oriented nodes across North America are supplying revitalized inventory, often embedded with energy-efficient envelopes and smart-home integrations that differentiate from aging secondary options.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Asia-Pacific commanded 38.4% of global revenue in 2025 on the back of sustained urban in-migration across China, India, and Southeast Asia. China Vanke alone delivered 117,000 units, emphasizing the region’s unmatched scale, while Tokyo’s pivot toward USD 680,000-plus inventory spotlights premiumization in land-starved locales. Indian tier-1 metros recorded double-digit absorption as IT employment and metro-rail extensions widened commuter belts. Though tightening credit weighs on presales in mainland China, policymakers are easing financing and unlocking secondary stock to stabilize demand, preserving a mid-single-digit trajectory.

The Middle East & Africa bloc is projected to post the fastest 6.53% CAGR to 2031, anchored by Saudi Arabia’s Vision 2030 mixed-use corridors and the ongoing influx of foreign capital into Dubai condominiums. Luxury high-rises with branded-residence components set record benchmarks, attracting global investors seeking trophy assets and offshore diversification. Sub-Saharan African metros such as Lagos are in early condominium cycles, yet structural housing deficits and improving mortgage penetration suggest long-run potential. Infrastructure gaps and currency risk temper near-term roll-outs, but incremental reforms in land-title systems could unleash a future wave of institutional capital.

North America and Europe together supply steady cash-flow avenues for institutional buyers, despite pronounced affordability pressures. Canada’s purpose-built rentals proliferate in Toronto and Vancouver as younger households defer ownership amid 7% mortgage coupons. Europe navigates lengthy permitting and strict tenant rules, yet Berlin, Paris, and London retain magnet status for global wealth. Latin America is opening faster approval pathways, evidenced by Mexico City’s one-stop hub, improving transparency and shortening start-to-finish timelines for international sponsors. Across these regions, proactive regulatory tweaks and transit-oriented development catalyze incremental supply against a backdrop of secular urban demand.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The condominiums and apartments market remains moderately fragmented, with regional champions dominating local share while a limited set of globally active developers cherry-pick high-growth corridors. China’s top ten still surpassed USD 138 billion of aggregate sales in 2025, yet their combined stake dipped as city-focused specialists exploited local relationships and policy niches. Competitive positioning revolves around delivery reliability, cost control, and the introduction of lifestyle-oriented amenities that command price premiums without over-stretching affordability thresholds.

Strategic pivots in 2025-2026 show incumbents hedging cyclicality through recurring-revenue businesses. China Vanke’s expansion into property services and rental operations boosted USD 6.0 billion in operating income, while Mitsui Fudosan accelerated data-center and senior-housing pipelines to diversify beyond core residential. Gulf-based Emaar ramped branded-residence licensing, fusing hospitality heritage with condominium sales to fortify brand equity. Developers also leverage proptech—Vanke’s in-house drawing a large-language model improved design validation more than fifteenfold—lowering rework and enhancing quality perception among buyers and regulators alike.

Joint ventures and public-private partnerships are increasingly common as land prices soar and entitlement risks grow. Shenzhen Metro backed Vanke with USD 4.1 billion of shareholder loans, exchanging liquidity for integrated station-area projects. In Europe, listed REITs collaborate with municipal housing bodies to deliver mixed-tenure schemes that satisfy affordable-housing quotas while preserving developer returns. Market participants unable to access patient capital or adopt tech-driven efficiencies are likely to exit or consolidate, yet the sector’s geographic dispersion suggests it will remain competitively balanced through 2031.

Condominiums And Apartments Industry Leaders

Emaar Properties

Lennar Corporation

China Vanke Co., Ltd.

Christie’s International Real Estate

Coldwell Banker Real Estate LLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- January 2026: China’s Ministry of Finance waived value-added tax on homes held more than two years to spur secondary-market liquidity.

- January 2026: Shanghai cut provident-fund mortgage rates to as low as 2.1%, easing buyer burden amid elevated benchmark rates.

- January 2026: China Vanke confirmed delivery of 117,000 units, 70% of its near-term backlog, supported by USD 4.1 billion in shareholder loans from Shenzhen Metro.

- August 2025: Vanke’s first-half 2025 revenue reached USD 14.5 billion; operating services generated USD 3.9 billion with 270,000 rental units at 93% occupancy.

Global Condominiums And Apartments Market Report Scope

By Business Model

| Sales |

| Rental |

| By Business Model | Sales |

| Rental |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What was the global value of the condominiums and apartments market in 2025?

The sector reached USD 6.20 trillion in 2025.

Which geographic region is forecast to grow the fastest through 2031?

The Middle East & Africa region is projected to expand at a 6.53% CAGR.

How large is the rental segment’s share and growth outlook?

Rentals held 39.8% of 2025 revenue and are expected to post a 6.05% CAGR to 2031.

What factors drive investor interest in multifamily assets?

Stable rental yields, inflation protection, and diversified cash flows make multifamily attractive to institutions.

Why are vertical projects becoming more common in major cities?

Limited land availability and zoning that favors high-rise density encourage developers to build upward.

How are high interest rates affecting homebuyers?

Elevated mortgage costs reduce purchasing power, lengthening sales cycles and pushing many households toward rental options.