Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

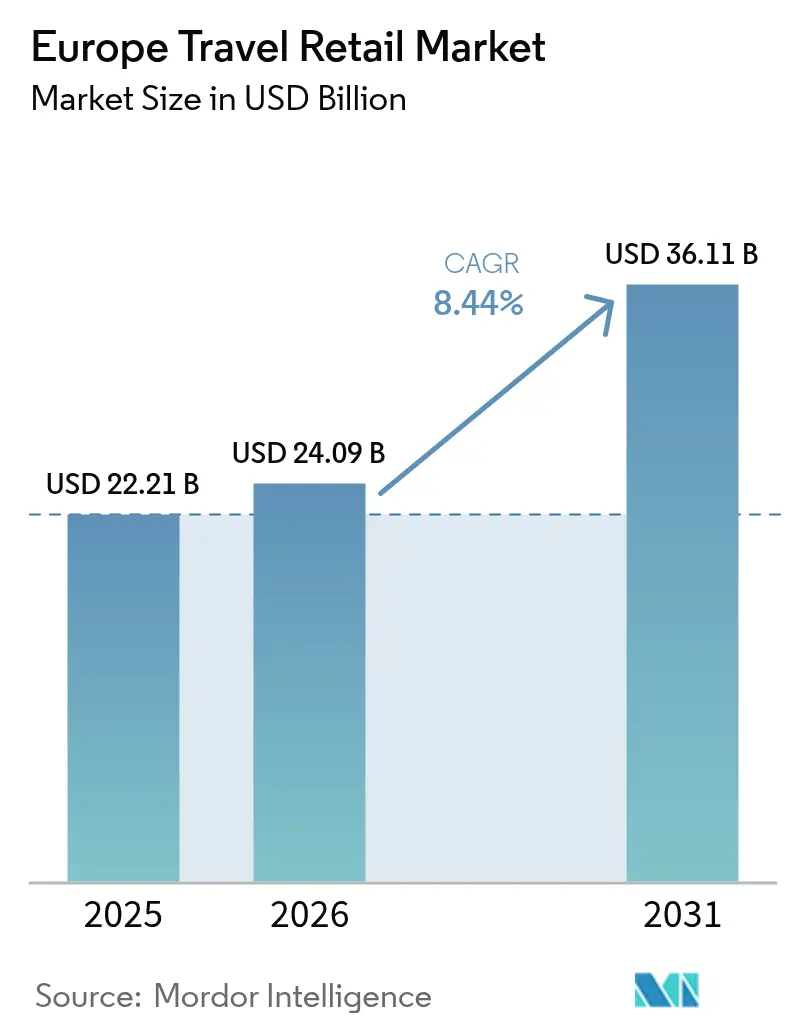

| Base Year Market Size (2025) | USD 22.21 Billion |

| Market Size (2026) | USD 24.09 Billion |

| Market Size (2031) | USD 36.11 Billion |

| Growth Rate (2026 - 2031) | 8.44% CAGR |

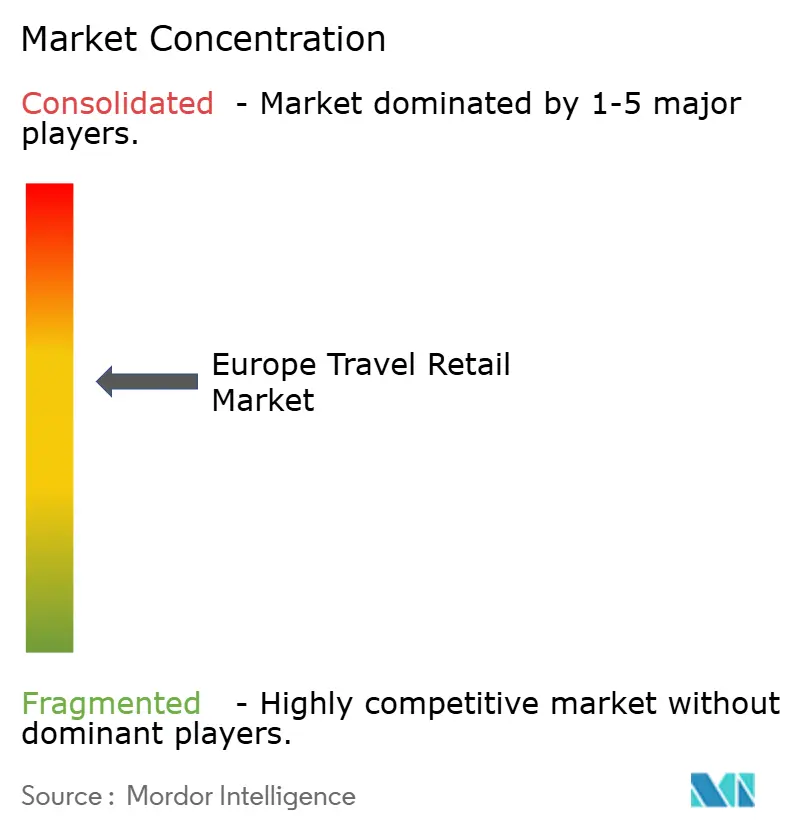

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Travel Retail Market Analysis by Mordor Intelligence

The Europe travel retail market is expected to grow from USD 22.21 billion in 2025 to USD 24.09 billion in 2026 and is forecast to reach USD 36.11 billion by 2031 at an 8.44% CAGR over 2026-2031. This growth surpasses the region's expected 4.4% air passenger increase in 2025, indicating stronger conversion rates and higher spending per passenger in key channels. Airport expansions and terminal upgrades are increasing commercial space and improving passenger flow, which extends dwell time and supports merchandising across categories. Global brands are refining retail formats and exclusive offerings at major hubs, enhancing pricing strategies and margins for the Europe travel retail market. Resilient high-yield travel segments are driving momentum, ensuring continued growth for the market into 2026.

Key Report Takeaways

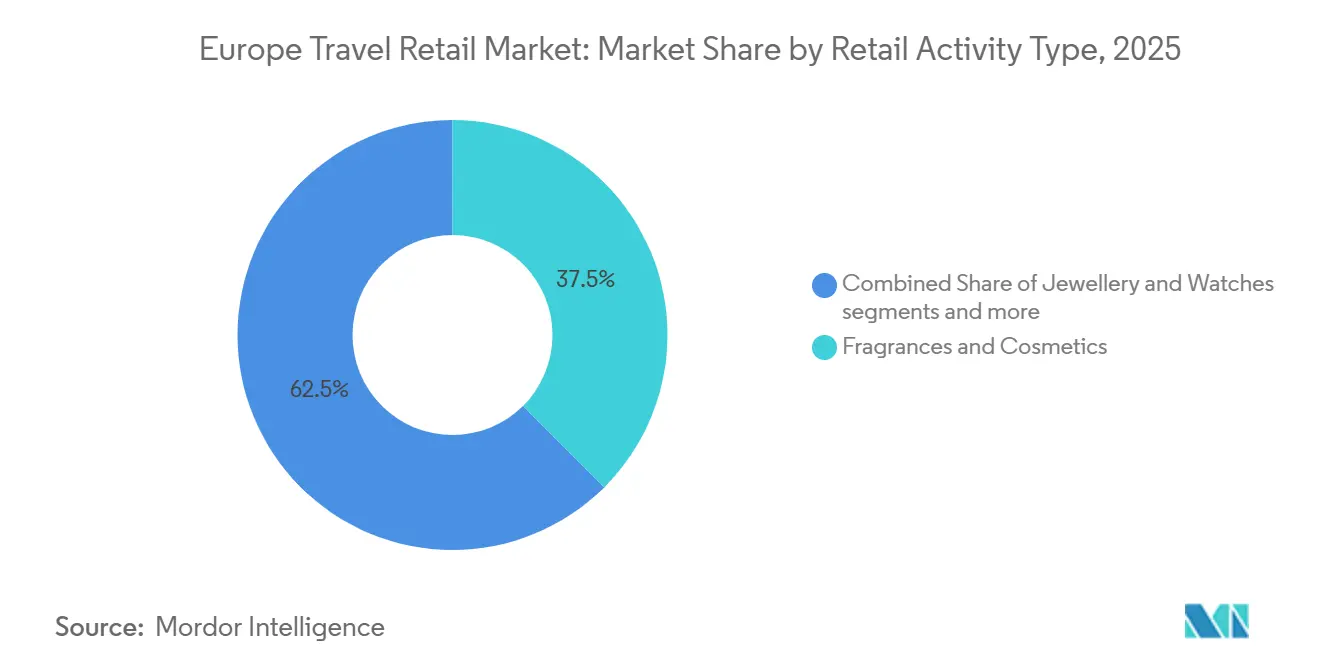

- By retail activity type, Fragrances and Cosmetics accounted for a 37.54% share of the Europe Travel Retail Industry in 2025, while Jewelry and Watches are projected to grow at a 12.29% CAGR through 2031.

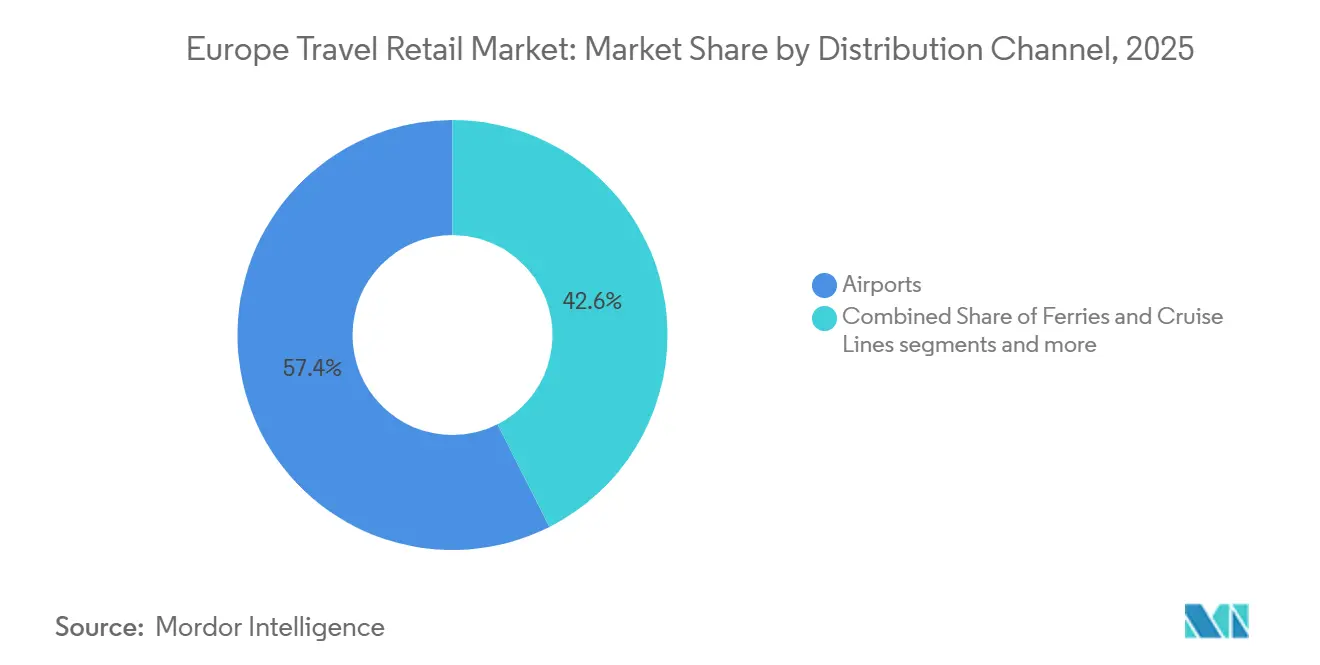

- By distribution channel, Airports led with 57.44% of the Europe Travel Retail Industry in 2025, while Ferries and Cruise Lines are forecast to expand at a 13.42% CAGR through 2031.

- By geography, the United Kingdom held 21.05% of the Europe Travel Retail Industry in 2025, while France is expected to post the fastest growth at a 13.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Travel Retail Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| International tourism growth is fueling demand across the Europe Travel Retail Industry | +2.1% | Global, spill-over benefits to the United Kingdom, France, Spain, Italy, and Greece | Medium term (2-4 years) |

| Rising air passenger traffic is expanding the customer base for travel retail | +2.3% | European Union, EFTA, Candidate countries, major hubs including London, Paris, Frankfurt, Madrid, Istanbul | Short term (≤ 2 years) |

| The ongoing expansion of airports and travel hubs is strengthening retail accessibility | +1.8% | Western Europe, the Middle East, with concentrations in Frankfurt, Athens, and Istanbul | Long term (≥ 4 years) |

| Greater availability of premium and luxury brands is enhancing traveler spending | +1.5% | Western Europe, including the United Kingdom, France, Italy, and major Middle East hubs | Medium term (2-4 years) |

| Supportive regulatory frameworks and duty‑free policies are boosting market attractiveness | +0.4% | European Union 27 and EFTA, with arrivals duty-free advocacy in the United Kingdom, the Netherlands, and France | Long term (≥ 4 years) |

| A consumer shift toward gifting and experiential purchases is reshaping retail preferences | +0.3% | Global, with resonance in the Asia-Pacific and spillover demand to Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

International tourism growth is fueling demand across the Europe Travel Retail Industry

Europe recorded 793 million international tourists in 2025, a 4% year-on-year rise, exceeding 2019 levels by 6%. Western Europe grew by 5%, Southern Mediterranean Europe by 3%, and Central and Eastern Europe by 6%, though the latter remained 9% below 2019 benchmarks. Travel spending increased by 9.7%, reflecting a shift toward higher-value trips. France and the United Kingdom saw receipts rise by 9% in the first ten months of 2025, while Spain posted a 7% gain, indicating strong retail demand. Projections for 2026 suggest improved visa facilitation and expanded networks could boost long-haul arrivals from China and India, supporting growth in Europe’s Travel Retail Market through sustained traffic and spending[1]Economic Times Travel, “Global Tourist Arrivals Rise 4% in 2025 as Travel Demand Returns to Pre Pandemic Growth Path – UN Tourism,” Economic Times Travel, economictimes.indiatimes.com.

Rising air passenger traffic is expanding the customer base for travel retail

European airports handled 2.6 billion passengers in 2025, a year-on-year increase of 100 million, indicating a return to normalized growth. The European Union aviation system processed 1.1 billion passengers in 2024, an 8.3% rise, with all 27 Member States showing gains, including several with double-digit growth. Extra-European Union international traffic accounted for 49.3% of movements, while intra-European Union and domestic flows supported retail opportunities in the Europe Travel Retail Market. Daily flight movements in Summer 2025 reached 35,122, setting a weekly record and ensuring stable operations across airports. In 2024, higher-end travel outperformed economy classes, reflecting a resilient corporate and leisure mix. High volumes, stable operations, and diverse traffic supported the market’s performance in 2026.

The ongoing expansion of airports and travel hubs is strengthening retail accessibility

European hubs are expanding capacity and modernizing passenger processing, enhancing commercial zones in the Europe Travel Retail Market. Munich Airport’s EUR 665 million (USD 782.25 million) Terminal 1 pier expansion, set for completion in 2026, will serve non-Schengen traffic with upgraded security and retail options. Heathrow’s expansion plan includes a new runway and Terminal 5X, targeting 150 million passengers to support route development and retail growth. Malta International Airport’s EUR 345 million program, to be completed by 2029, doubles terminal size and increases clean energy use. Vilnius Airport’s new arrivals terminal, designed by Zaha Hadid Architects, improves capacity and customer experience. These projects collectively create opportunities for retail operators in the Europe Travel Retail Market[2]Munich Airport, “Press: Grand Opening of Terminal 1 Pier on April 13,” Munich Airport, munich-airport.com.

Greater availability of premium and luxury brands is enhancing traveler spending

LVMH's DFS Group and Sephora reported EUR 18.3 billion (USD 21.53 billion) in revenue in 2025, with a 28% rise in profits from recurring operations. Sephora expanded by opening approximately 100 new stores. Brand portfolios, featuring exclusive labels and curated concepts, drove customer engagement in the Europe Travel Retail Market. Niche fragrance concepts gained traction after a 29% year-on-year sales increase at Istanbul Airport in 2024, leading to rollouts in Vienna and Copenhagen in 2025. A major transaction at Amsterdam Airport Schiphol consolidated concessions, enhancing luxury and duty-free retail access. Expanding assortments in luxury, beauty, and specialty categories supported price stability and value creation in the Europe Travel Retail Market.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macro‑economic and geopolitical volatility is disrupting travel demand across the Europe Travel Retail Industry | -1.2% | Global, with acute effects in the Russia–Ukraine corridor, Eastern Mediterranean, and parts of Scandinavia | Short term (≤ 2 years) |

| Stringent regulations and customs policies are constraining duty‑free and cross‑border retail operations | -0.8% | European Union 27, EFTA, United Kingdom, with national enforcement by customs authorities | Medium term (2-4 years) |

| High operational costs in airport retail spaces are eroding profitability for operators | -0.5% | Western Europe, including the United Kingdom, France, and Germany, at major hubs | Medium term (2-4 years) |

| Intensifying competition from e‑commerce and domestic retail channels is diverting consumer spending | -0.7% | Global, with intensity in the United Kingdom, Germany, and France | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Macro economic and geopolitical volatility is disrupting travel demand across the Europe Travel Retail Industry

Geopolitical tensions and restricted airspace are altering East–West routes, reducing flight frequency and retail footfall in affected city pairs. Currency weakness in Northern Europe in 2025 pressured discretionary spending, leading to trade-down behavior in airport stores and lower transaction values at key hubs. Confidence indicators for 2026 suggest caution due to economic concerns and rising trip costs, potentially reducing passenger spending. Air traffic remains stable, but demand is vulnerable to regional tensions and inflation-driven budget adjustments. Energy prices may ease slightly, but high tourism service costs could limit impulse purchases in the Europe Travel Retail Market. Transatlantic demand is sensitive to macroeconomic factors, including economic growth downgrades and trade frictions, impacting revenue from key segments[3]Airiane, “The Impact of Global Events on Air Travel Demand in 2025,” Airiane, airiane.com.

Stringent regulations and customs policies are constraining duty free and cross border retail operations

The European Union's removal of the EUR 150 (USD 176.45) de minimis exemption in July 2026 will impact cross-border e-commerce and highlight the value of duty-free purchases in regulated channels. Since 2024, Member States have adjusted VAT rates, affecting domestic price comparisons in the Europe Travel Retail Market. France aligned tobacco import thresholds with European Union directives in 2025, while enforcement remains at customs officers' discretion. Finland documented European Union-imposed customs duties on certain United States imports, reflecting evolving tariff dynamics. These changes complicate compliance for retailers and partners, but Duty-Free’s transparent framework fosters shopper trust. Clear policy communication supports sales conversions, helping travelers assess the value of purchases in the Europe Travel Retail Market[4]Avalara, “EU to End €150 Customs Duty Exemption in 2026,” Avalara, avalara.com.

Segment Analysis

By Retail Activity Type: Fragrances and Cosmetics Anchor Premium Growth

Fragrances and Cosmetics accounted for 37.54% of the category mix in 2025, driven by strong demand for beauty products and limited-edition exclusives in the Europe Travel Retail Market. Dior sustained its position in men’s fragrances through new launches, supporting growth in beauty segments that attract airport shoppers. Jewelry and Watches, with a 12.29% CAGR from 2026 to 2031, reflected the continued appeal of luxury among affluent travelers. Leading brands enhanced retail concepts with personalized service and storytelling, increasing conversions and transaction values in key locations. These factors kept beauty and luxury goods central to the Europe Travel Retail Market's growth.

Niche fragrance formats expanded after strong 2024 results at Istanbul Airport, leading to new offerings in Vienna and Copenhagen and broader artisanal assortments in high-traffic terminals. Fashion and Accessories contributed 8% to a major European operator’s 2024 revenues, supported by curated selections in sunglasses and leather goods for time-conscious shoppers. Tobacco, under regulatory pressure, is gradually being replaced by Reduced-Risk Products in some regions, reshaping product displays to align with consumer preferences. Food and Confectionery remained popular impulse purchases, with brands using travel-exclusive packaging and regional flavors to enhance value. Electronics and Gadgets maintained demand for accessories and chargers, while retailers focused on key concessions to drive growth investments in 2026 across the Europe Travel Retail Market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Airports Dominate, Ferries Accelerate

Airports accounted for 57.44% of the Europe Travel Retail Market in 2025, serving as the main point for shopper engagement and conversion across international passenger flows. In 2023, airport commercial activities significantly contributed to non-aeronautical revenue, emphasizing the importance of retail and food services in airport business models. Operators used data-driven merchandising and hybrid retail concepts to enhance dwell-time monetization, increasing average ticket values. Large concessions with portfolio operators provided procurement and brand access advantages, reinforcing the airport channel’s role in the market. These factors supported airport retail during steady traffic recovery and demand stability.

Ferries and cruise lines are projected to grow at a 13.42% CAGR from 2026 to 2031, driven by increased maritime connectivity, updated onboard formats, and rising tourism on key routes. Operators expanded store footprints and modernized offerings, improving duty-free selections and shopper flow. Tallink Grupp generated notable revenue from onboard restaurants and shops, highlighting the role of retail in maritime passenger economics. In-flight retail complemented the market with curated offers and pre-order services aligned with carrier models and IATA standards. Railway stations, land-border, and downtown formats offer additional opportunities linked to urban regeneration and shifts in transportation modes, enhancing the reach of the Europe Travel Retail Market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The United Kingdom held a 21.05% share of the Europe Travel Retail Market in 2025, driven by the London system and Heathrow's role as a global hub. Heathrow managed high passenger volumes and initiated plans to increase capacity, adding routes and improving connectivity. The removal of tax-free shopping schemes post-Brexit made continental hubs more attractive to some international shoppers, prompting discussions on arrivals duty-free policies. Despite these challenges, strong long-haul demand, established brands, and airport investments supported the market. In 2026, operators with diverse channels utilized airport, ferry, and cruise networks to maintain resilience.

France is projected to grow at a 13.08% CAGR from 2026 to 2031, supported by Paris Charles de Gaulle's hub dynamics and increased tourism. In 2025, Charles de Gaulle handled significant passenger volumes and maintained a strong long-haul network, attracting travelers with high conversion rates in beauty and luxury categories. By 2024, France surpassed 2019 arrival levels, and tourism receipts rose 9% in the first ten months of 2025, strengthening duty-free and travel retail opportunities. In 2026, discussions on arrivals duty-free policies continued, balancing competitiveness with compliance, positioning France as a key market contributor.

BENELUX and the Nordics showed mixed but supportive trends for the Europe Travel Retail Market. In 2025, the Netherlands saw a major operator begin duty-free operations at Amsterdam Airport Schiphol after acquiring a 70% stake in its retail entity, enhancing brand access and scale. Finland recorded a 14.1% rise in international arrivals, aiding Nordic demand, while currency challenges in Northern and Baltic regions reduced discretionary spending and average tickets. Athens expanded its airport and introduced incentive schemes, strengthening its position for route development and retail growth. Turkey's main hub remained a significant revenue contributor, reflecting the importance of East–West gateways in the region.

Competitive Landscape

The Europe Travel Retail Market is moderately concentrated, with the top four operators holding a combined 60–65% share due to their diverse presence across airports, ferries, and cruise lines. Avolta reported CHF 7,180 million (USD 9,088.9 million) in EMEA turnover for 2024, with 72% of sales from airports and 6.3% organic growth, driven by steady passenger numbers and increased spending per passenger. Autogrill's integration added CHF 85 million in benefits, enhancing food service capabilities and hybrid offerings in airport terminals. Avolta secured long-term Spanish concessions covering 21 airports and over 120 outlets, strengthening procurement scale and brand access, which supports operating leverage in a sector favoring diversified portfolios.

Lagardère Travel Retail recorded EUR 5,812 million (USD 6,836.7 million) in revenue in 2024 and EUR 305 million (USD 358.8 million) in recurring EBIT, reflecting gains across EMEA and an expanded presence in key hubs. In May 2025, Lagardère began duty-free operations at Amsterdam Airport Schiphol after acquiring a 70% stake in Schiphol Consumer Services Holding BV, making it the group’s second-largest airport operation after Paris. The operator also secured travel essentials concessions in German airports for 2026 openings, broadening terminal exposure and improving route-to-basket capture. Gebr. Heinemann reported EUR 4.3 billion in turnover in 2024, with Beauty leading sales and Fashion and Accessories growing at a double-digit rate. The company expanded its footprint in Vienna and secured tenders in Iceland and the Baltics, increasing regional coverage.

LVMH’s Selective Retailing division, including DFS and Sephora, generated EUR 18.3 billion (USD 21.53 billion) in revenue in 2025, with a 28% rise in profit from recurring operations. In January 2026, LVMH agreed to acquire DFS’s Greater China business from China Tourism Group Duty Free, streamlining operations and focusing on profitability. Sephora opened approximately 100 stores in 2025, maintaining a high share of exclusive brands. Operators are adopting technology, such as AI tools and cashier-less stores, to enhance productivity and customer experience. Airport expansions in Western Europe are expected to reshape commercial contracting, requiring strategic alignment of concession economics and capital planning.

Europe Travel Retail Industry Leaders

Dufry AG

Lagardere Travel Retail

Gebr. Heinemann SE & Co. KG

Autogrill S.p.A. / World Duty Free

LVMH (Moet Hennessy Louis Vuitton)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2026: Avolta expanded in Italy with new food and beverage contracts at Verona Valerio Catullo Airport (ten-year contract with five F&B concepts) and Florence Amerigo Vespucci Airport (six-year contract introducing two airside concepts with Tuscan-inspired cuisine). These developments highlight Avolta's focus on enhancing traveler experiences and strengthening airport partnerships.

- February 2026: JD Wetherspoon, in partnership with Lagardère Travel Retail, opened its first continental Europe location at Alicante–Elche Miguel Hernández Airport, Spain. The 93-square-meter pub, "Castell de Santa Bàrbera," is airside in departures and serves a menu blending Wetherspoon staples (breakfast, burgers, pizzas) with Spanish dishes (garlic prawns, Spanish omelette). It operates daily from 6 am to 9 pm.

- February 2026: WHSmith opened three new stores at Manchester and Liverpool airports. At Manchester Airport Terminal 2, it launched its first artisan coffee shop, Grindsmith, and a travel essentials store. Liverpool John Lennon Airport now features a larger store offering health & beauty products, food & drink, tech, books, magazines, and city-specific gifts. These openings highlight WHSmith's focus on Northern travel hubs and modern travel spaces with local design elements.

- January 2026: Gebr. Heinemann signed a ten-year concession agreement with Scandlines, starting January 27, 2026, to manage "Travel Shops" on six ferries and two "BorderShops" in Puttgarden and Rostock, Germany. Previously a product supplier, Heinemann now assumes direct operational control, strengthening the partnership and enhancing the shopping experience while supporting Scandlines' business growth.

Europe Travel Retail Market Report Scope

The Europe Travel Retail Industry report examines duty-free and travel-related retail activities across airports, airlines, ferries, cruise lines, railway stations, land-border shops, and downtown duty-free outlets. The market is segmented by retail activity type (fragrances & cosmetics, fashion, jewelry & watches, wine & spirits, food & confectionery, tobacco, electronics, travel essentials & gifts), distribution channel, and country (UK, Germany, France, Spain, Italy, BENELUX, Nordics, and Rest of Europe). It analyzes drivers like international tourism growth, rising passenger traffic, airport expansion, luxury brand availability, regulatory frameworks, and changing consumer preferences. Restraints include macro-economic volatility, customs policies, high operational costs, and e-commerce competition. The study evaluates the regulatory landscape, technological outlook, supply-chain dynamics, and competitive intensity using Porter’s Five Forces framework. The report provides market size and growth forecasts, company profiles, strategic developments, and future opportunities, including white-space assessments and unmet needs. The report offers market size and forecasts for the Europe Travel Retail Market in value (USD) for all the above segments.

By Retail Activity Type

| Fragrances and Cosmetics |

| Fashion and Accessories |

| Jewellery and Watches |

| Wine and Spirits |

| Food and Confectionery |

| Tobacco |

| Electronics and Gadgets |

| Travel Essentials and Gifts |

By Distribution Channel

| Airlines (In-flight) |

| Ferries and Cruise Lines |

| Railway Stations |

| Land-Border Shops |

| Downtown Duty-Free |

By Country

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Retail Activity Type | Fragrances and Cosmetics |

| Fashion and Accessories | |

| Jewellery and Watches | |

| Wine and Spirits | |

| Food and Confectionery | |

| Tobacco | |

| Electronics and Gadgets | |

| Travel Essentials and Gifts | |

| By Distribution Channel | Airlines (In-flight) |

| Ferries and Cruise Lines | |

| Railway Stations | |

| Land-Border Shops | |

| Downtown Duty-Free | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the Europe travel retail market size and growth outlook to 2031?

The Europe travel retail market is expected to grow from USD 22.21 billion in 2025 to USD 24.09 billion in 2026 and is forecast to reach USD 36.11 billion by 2031 at an 8.44% CAGR over 2026-2031.

Which categories lead and grow fastest in European travel retail?

Fragrances and Cosmetics led with 37.54% share in 2025, while Jewelry and Watches are projected to grow fastest at a 12.29% CAGR through 2031 within the Europe Travel Retail Market.

Which channels are most important for European travel retail sales?

Airports held a 57.44% share in 2025, while Ferries and Cruise Lines are forecast to expand at a 13.42% CAGR through 2031 for the Europe Travel Retail Market.

Which countries lead and accelerate in European travel retail?

The United Kingdom led with a 21.05% share in 2025, while France showed the fastest trajectory with a 13.08% CAGR to 2031 in the Europe Travel Retail Market.

What macro and regulatory risks could weigh on European travel retail?

Volatile geopolitics and evolving European Union customs and VAT changes, including the removal of the EUR 150 de minimis threshold in 2026, can affect consumer spending and compliance burdens in the Europe Travel Retail Market.

How are leading operators strengthening positions in European travel retail?

Operators are expanding flagship concessions, deploying technology, and scaling brand partnerships, with major transactions at key hubs and steady EMEA revenue growth that support the Europe Travel Retail Market.