Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

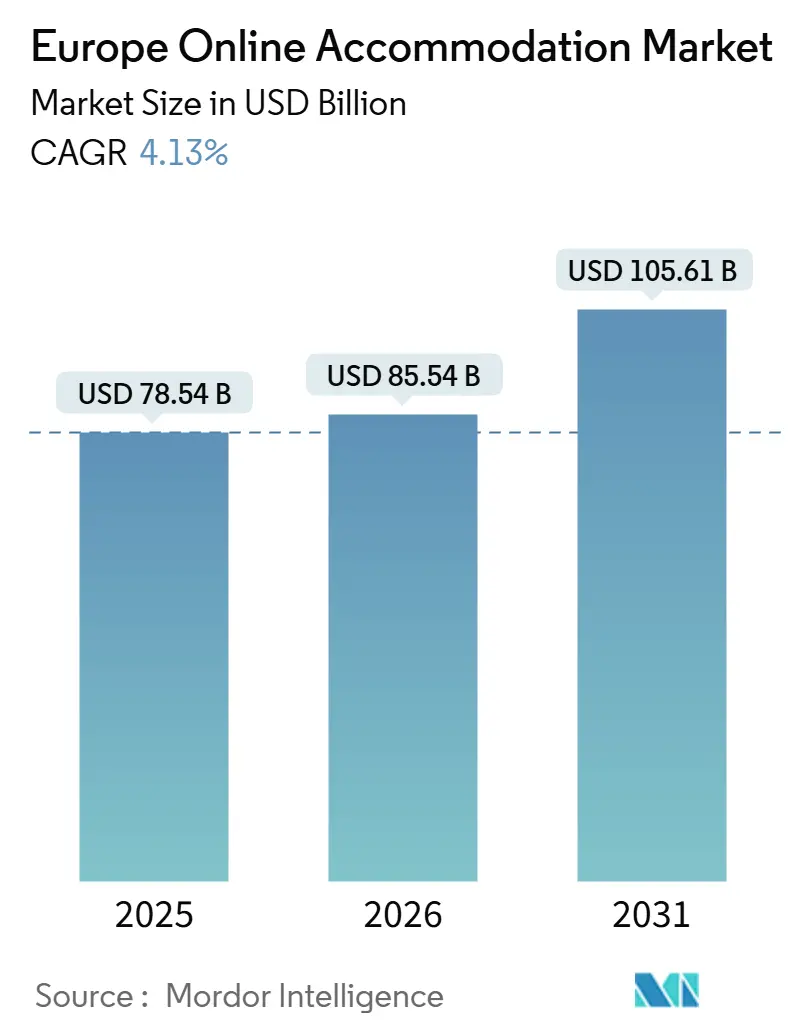

| Base Year Market Size (2025) | USD 78.54 Billion |

| Market Size (2026) | USD 85.54 Billion |

| Market Size (2031) | USD 105.61 Billion |

| Growth Rate (2026 - 2031) | 4.13% CAGR |

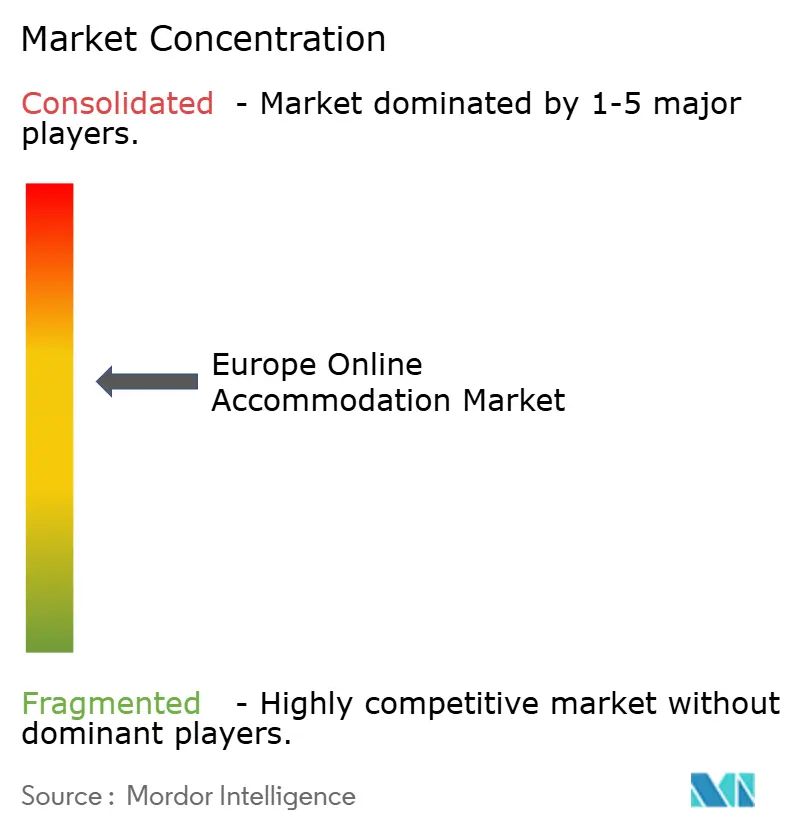

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Online Accommodation Market Analysis by Mordor Intelligence

The Europe online accommodation market size is expected to grow from USD 78.54 billion in 2025 to USD 85.54 billion in 2026 and is forecast to reach USD 105.61 billion by 2031, reflecting a 4.13% CAGR through the forecast period. As travel demand normalizes across the region, growth is increasingly driven by sustained digital adoption, high smartphone penetration, and strong cross-border mobility within Europe. The widespread use of mobile booking apps, price comparison tools, and digital payment systems continues to strengthen online channels, while the expansion of short-term rentals, serviced apartments, and hybrid lodging formats broadens the available inventory and attracts diverse traveler segments, including digital nomads and experience-focused tourists. Regulatory developments are also reshaping competitive dynamics within the market. Additionally, the Payment Services Regulation and PSD3, finalized in November 2025, introduce stronger authentication measures, IBAN and name verification requirements, and clearer liability frameworks to reduce fraud and harmonize cross-border digital payments. At the same time, platforms and hotel chains are increasingly integrating artificial intelligence into search algorithms, dynamic pricing, merchandising, and customer service operations, improving conversion rates and operational efficiency.

Key Report Takeaways

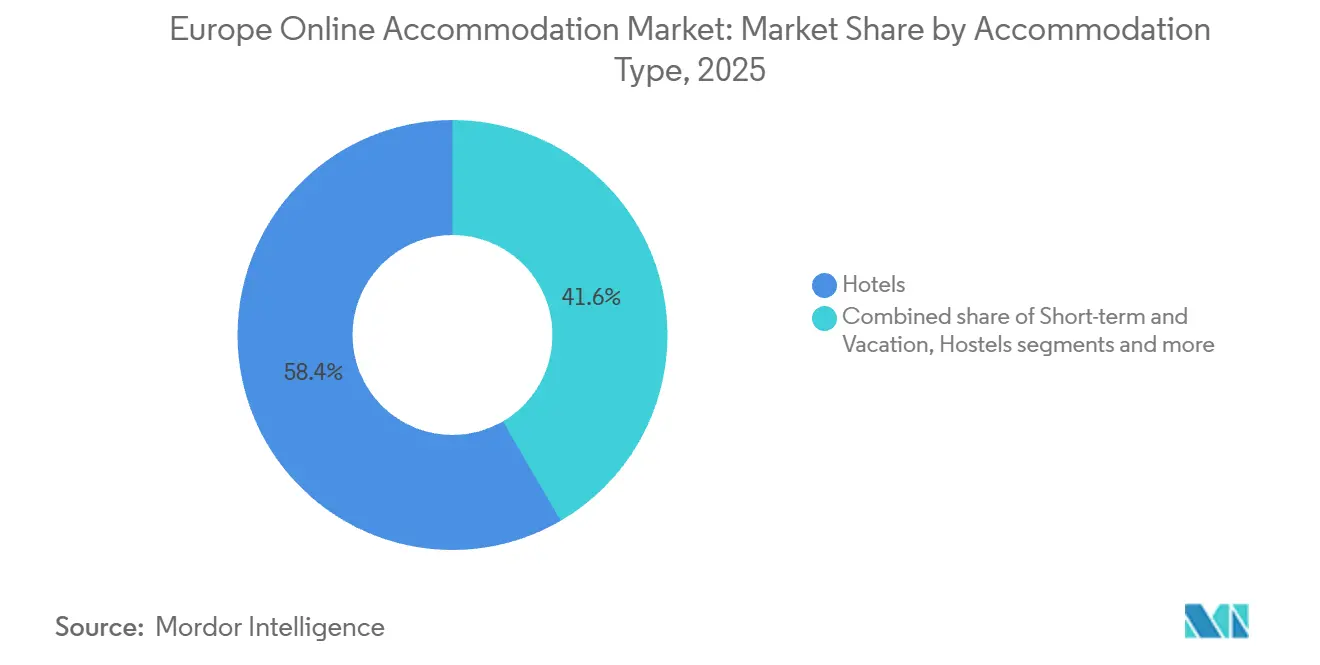

- By accommodation type, hotels accounted for 58.40% of the Europe online accommodation market size in 2025, while short-term and vacation rentals are forecast to expand at a 6.81% CAGR through 203.

- By booking channel, Online Travel Agencies held 62.10% of the Europe online accommodation market size in 2025 and are projected to grow at a 7.34% CAGR through 2031.

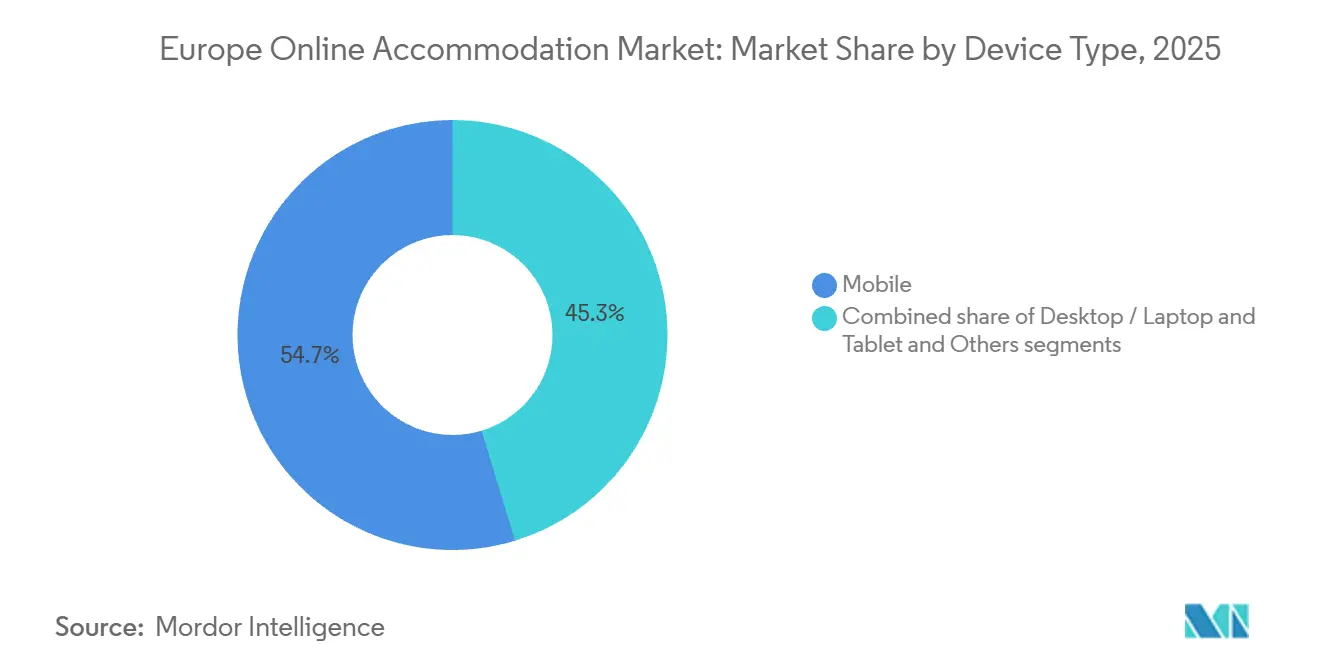

- By device type, mobile captured 54.7% of the Europe online accommodation market size in 2025 and is advancing at an 8.11% CAGR through 2031.

- By traveler type, leisure accounted for 70.2% of the Europe online accommodation market size in 2025, while bleisure is projected to post a 5.90% CAGR through 2031.

- By country, Germany held 11.90% of the Europe online accommodation market size in 2025, while France is forecast to record the fastest growth at a 7.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Online Accommodation Market Trends and Insights

Drivers Impact Analysis

| Driver | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in smartphone-led mobile bookings | +1.8% | Global, strongest in Nordic markets and the UK | Short term (≤ 2 years) |

| Pent-up leisure demand and intra-Europe travel rebound | +1.2% | Southern and Mediterranean Europe, Central and Eastern Europe | Medium term (2-4 years) |

| OTA dominance is creating transparent, price-competitive inventory | +0.7% | EU-wide, strongest in mature Western markets | Long term (≥ 4 years) |

| EU Digital Markets Act unlocking data-driven direct-booking innovation | +1.1% | EU27 and EEA, spillover to candidate countries | Medium term (2-4 years) |

| AI-powered dynamic packaging and personalized offers lift conversion | +1.0% | Advanced markets including the UK, Germany, the Netherlands, Nordics | Medium term (2-4 years) |

| Secondary-city tourism boom expands STR supply | +0.9% | Central and Eastern Europe, Iberian Peninsula secondary markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Smartphone-Led Mobile Bookings

Mobile devices captured 54.7% of booking volume in 2025 and led growth with platforms reporting higher in-app engagement, as evidenced by Airbnb’s disclosure that 64% of Q4 2025 nights were booked via its app, up 400 basis points year over year.[1]Source: Airbnb, “Q4 2025 Shareholder Letter,” Investor Materials, airbnb.com. As of September 2025, Booking.com had 32 million listings, including 4.4 million active properties and 3.9 million alternative stays. The platform facilitated about 1.2 billion room nights over the year, with direct bookings around 65% of total nights. Alternative accommodations grew from 35% to 36%, highlighting rising demand for non-traditional stays and strong digital engagement in online accommodation.[2]Source: Booking Holdings, “Investor Presentation October 2025,” Corporate Presentation, s201.q4cdn.com. Data, privacy, and transparency baselines required by EU digital laws have prompted cleaner onboarding and consent flows that in turn support smoother mobile conversion journeys in the Europe online accommodation market. Product innovation in mobile checkout, including “Reserve Now, Pay Later,” which Airbnb piloted in August 2025 and completed global rollout in February 2026, reinforces mobile’s primacy by addressing liquidity constraints without disrupting host payouts.

Pent-Up Leisure Demand and Intra-Europe Travel Rebound

In 2025, the total number of nights spent in tourist accommodation establishments across the European Union reached a record high of approximately 3.08 billion, an increase of 61.5 million nights (+2%) compared with 2024. This growth reflects continued expansion in tourism activity across most EU Member States.[3]Source: Eurostat, “EU tourism nights at record 3.08 billion in 2025,” Eurostat News, ec.europa.eu. European Travel Commission tracking showed that 77% of Europeans planned trips in the second half of 2025 despite economic headwinds, with a rising share seeking less crowded destinations, which expanded addressable demand across secondary and Central and Eastern European locations. Intra-regional travel remained a mainstay due to Schengen mobility and rail expansions, which together reduce friction and encourage shorter, more frequent trips that favor digital channels for accommodation search and booking.[4]Source: European Travel Commission, “Monitoring Sentiment for Intra-European Travel Summer/Autumn 2025,” ETC Report, etc-corporate.org. Southern and Mediterranean destinations absorbed a large share of peak-season activity in 2025 even as travelers diversified into Central and Eastern Europe, a pattern that sustains broad distribution of demand across the Europe online accommodation market. Aviation and maritime decarbonization policies entering into force in 2025 are raising operator compliance costs, which can redirect some demand to rail-accessible destinations and keep intra-Europe trips at the core of segment growth.

EU Digital Markets Act: Unlocking Data-Driven Direct-Booking Innovation

The EU Digital Markets Act designated Booking.com as a gatekeeper in May 2024 and triggered obligations that include eliminating EU-wide parity clauses, increasing transparency, and offering data access for business users, which together open room for hotels and alternative accommodation operators to strengthen direct channels. As parity rules unwind and anti-steering provisions are enforced, suppliers gain scope to differentiate offers and pricing on their websites and apps, which can reclaim a portion of demand over the medium term in the Europe online accommodation market.[5]Source: European Commission, “Booking must now comply with the Digital Markets Act,” Press Corner, ec.europa.eu. Large chains are responding by improving loyalty programs and integrating AI-enabled pricing and merchandising that match or exceed OTA presentation standards, a trend that tightens economics for repeat customers and high-value stays. The DMA’s prohibition on self-preferencing also reduces algorithmic ranking advantages that previously favored OTA merchant models and encourages more transparent comparisons across direct and indirect channels. These shifts incentivize both sides of the ecosystem to invest in cleaner data pipelines and collaborative analytics, improving yield and conversion across the Europe online accommodation market.

AI-Powered Dynamic Packaging and Personalized Offers Lift Conversion

Connected trip concepts are scaling in 2026 as Booking Holdings and peers extend AI across itinerary building, dynamic bundling, and context-aware recommendations, with Booking reporting mid-20s % growth in connected transactions in late 2025 that supports higher attachment rates.[6]Source: Booking Holdings, “Investor Presentation October 2025,” Corporate Presentation, s201.q4cdn.com. Hoteliers adopting AI revenue management tools report meaningful RevPAR lifts and time savings, which improve the viability of direct distribution that competes more evenly with OTA merchandising in the Europe online accommodation market. Platform AI copilots are reshaping discovery as conversational search reduces friction for complex trip patterns and tailors accommodation suggestions to intent signals that were previously hard to capture with traditional filters. These capabilities also help suppliers surface extended-stay and work-friendly options that align with bleisure behavior, expanding addressable demand without diluting brand standards. As personalization deepens, suppliers can refine offer sequencing and price ladders, capturing incremental value while sustaining conversion quality within the Europe online accommodation market.

Restraints Impact Analysis

| Restraint | (~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High OTA commission pressure on supplier margins | -0.9% | EU-wide, acute in the Southern Europe hospitality sectors | Medium term (2-4 years) |

| City-level clamp-downs on short-term rentals | -1.4% | Major urban centers, including Amsterdam, Barcelona, Berlin, Paris, and Vienna | Short term (≤ 2 years) |

| Multi-scheme Payments & PSD-3 Compliance Complexity | -0.7% | EU-wide, especially affecting cross-border operators | Medium term (2-4 years) |

| Revenue-tech Talent Shortages Slow Digital Roll-outs | -0.6% | Europe-wide, more acute in technology hubs | Short to medium term (1-3 years) |

| Source: Mordor Intelligence | |||

High OTA Commission Pressure on Supplier Margins

Commission structures in the OTA channel continue to weigh on supplier margins, and the merchant model’s prominence has historically supported take rates that are difficult for smaller properties to offset via direct channels without scale in digital marketing or loyalty. As DMA enforcement curbs self-preferencing and parity provisions, some rate dispersion is emerging, but rebalancing remains gradual and uneven across markets in the Europe online accommodation market. Expedia’s 2025 filings highlighted a notable divergence between its B2B business, which grew 24% year over year in Q4 2025, and B2C, which grew 5%, indicating a shift toward white-label partnerships that can alter distribution economics for suppliers and intermediaries. Tax and compliance headwinds also persist, as evidenced by Expedia’s finalized USD 183 million settlement with Italian authorities for withholding tax obligations covering 2017-2023, which has implications for commission pass-through and visibility terms in several EU jurisdictions.[7]Source: Expedia Group, “Form 10-K for FY2025,” SEC Filings, sec.gov. Over the medium term, suppliers that scale AI-enabled revenue management and loyalty activation are better positioned to dilute commission exposure without sacrificing demand coverage within the Europe online accommodation market.

City-Level Clamp-Downs on Short-Term Rentals

Municipal enforcement across major European cities has tightened, with policies such as Amsterdam’s 30-night annual cap, Barcelona’s announced phase-out of tourist apartment licenses by November 2028, and Vienna’s high penalties per unit curbing available inventory on platforms during 2025. The cumulative effect removed tens of thousands of listings from regulated supply, changing pricing dynamics and shifting some demand toward compliant professional operators and licensed alternatives within the Europe online accommodation market. Regulation (EU) 2024/1028, effective May 2026, standardizes host registration and platform data-sharing responsibilities, including displaying unique registration numbers and enabling public authority access to activity data, which raises compliance clarity but adds process complexity for smaller hosts. Platform strategies in 2026 reflect these constraints, with EMEA growth patterns showing localized deceleration where restrictions are strict and more resilient trends where frameworks remain stable. Over time, standardized rules are expected to consolidate the segment around compliant professional operators and brands, altering supply composition while preserving consumer choice in the Europe online accommodation market.

Segment Analysis

By Accommodation Type: Hotels Defend Share as Alternative Inventory Professionalizes

Hotels held 58.40% of the Europe online accommodation market in 2025, supported by ongoing additions from global chains and steady growth in loyalty programs that enhance both direct and indirect distribution across the region. Short-term and vacation rentals remain the fastest-growing accommodation type with a 6.81% CAGR projected through 2031, which reflects continued traveler appetite for residential space, flexible layouts, and neighborhood locations that complement traditional hotel use cases in the Europe online accommodation market. Regulatory changes are playing a crucial role, with new standardized registration requirements simplifying compliance for platforms and professional operators across EU member states. Leading platforms report a deep inventory of alternative accommodations, which adds variety and complements hotel options for mixed travel itineraries. Hotel chains are increasingly focusing on upscale and luxury segments to maintain their market share even as alternative accommodations continue to expand.

The growth of short-term rentals is balanced by increased compliance demands and operational complexity, encouraging greater professionalization and technology adoption among property managers and hosts. There is a noticeable shift toward leveraging AI-enhanced direct booking websites and revenue management tools, signaling a move from purely occupancy-driven growth to value creation through better operations and merchandising. Hotel brands are also gaining momentum, particularly in the luxury and lifestyle sectors, aligning with the preferences of premium travelers in major European cities. The dynamic between hotels and alternative stays remains positive, with each serving distinct customer needs while overlapping in areas like extended stays, family travel, and work-friendly accommodations. Overall, hotel loyalty programs, branded service quality, and mobile app conversions continue to sustain hotel market share even as alternative accommodations broaden consumer choice.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Booking Channel: OTAs Plateau as Direct Channels Reclaim Margin

Online Travel Agencies held a 62.10% share in 2025 and are expected to post a 7.34% CAGR through 2031, as evolving regulations and the rise of direct distribution reshape booking patterns. The removal of parity clauses and increased transparency requirements under new regulations have allowed hotels and professional hosts greater flexibility to offer differentiated packages, loyalty rewards, and exclusive rates on their own platforms. OTAs are also adapting by expanding business-to-business partnerships and corporate travel solutions, complementing their consumer-facing channels. Mobile apps continue to be a key driver of bookings, with many travelers preferring the convenience and personalized experiences they provide. Moving forward, distribution strategies are expected to rely increasingly on AI-driven visibility and integrated travel solutions rather than traditional search rankings alone.

Direct booking channels are improving both customer experience and cost efficiency, supported by AI-powered revenue management tools that enhance pricing strategies and save operational time. New payment regulations introduce additional verification steps, which can complicate some intermediary processes but allow direct sites to offer smoother authentication and preferred payment options. Corporate and managed travel segments are becoming important sources of inventory as platforms strengthen business partnerships that extend reach beyond public search visibility. Metasearch engines are evolving to use AI personalization to improve the quality of traffic and bidding efficiency for both suppliers and OTAs. Overall, the market is moving toward a more balanced distribution environment where OTAs continue to play a critical role in reach and merchandising, while direct channels and corporate partnerships focus on improving margins and building customer loyalty.

By Device Type: Mobile Dominates as AI Interfaces Reshape Discovery

Mobile captured 54.7% of bookings in 2025 and is advancing at an 8.11% CAGR through 2031, driven by product developments that focus on conversational interfaces, simplified consent processes, and flexible payment options. Platforms like Airbnb demonstrate the power of native app experiences by integrating trip planning and post-booking support, which enhance user engagement. Booking Holdings has invested heavily in AI to improve search relevance, service interactions, and merchandising, further strengthening mobile’s competitive advantage. While desktop remains important for more complex itineraries and group planning, product teams are adding AI-powered assistants to streamline these tasks across devices. Payment regulations introduced recently have made mobile checkouts more secure and reliable, benefiting both consumers and suppliers across the region.

Innovations such as “Reserve Now, Pay Later” have supported mobile-first booking behavior by aligning payment timing with consumer cash flow while ensuring host payment security. User interface improvements under EU digital rules have also streamlined onboarding and accelerated mobile booking flows. As a result, mobile continues to outperform desktop for quick, single-property bookings, whereas desktop still plays a role in detailed comparisons and negotiated stays. With the rise of AI booking assistants, more discovery and purchase interactions are shifting into chat-based interfaces that then finalize transactions within mobile apps. Suppliers are adapting by tailoring content, pricing, and upsell opportunities to mobile-first journeys, further concentrating booking activity within native app environments.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Traveler Type: Leisure Dominance Masks Business Recovery

Leisure accounted for 70.2% of bookings in 2025, reflecting strong consumer demand for diverse travel experiences and the extensive connectivity that supports year-round trips across a variety of budgets and interests. Despite macroeconomic uncertainty, European travelers continue to plan trips, with increasing interest in less crowded and off-the-beaten-path destinations. Business travel is stabilizing below pre-2020 peaks as hybrid work reshapes trip patterns, while bleisure is the fastest-growing traveler type with a 5.90% CAGR projected through 2031 as travelers extend weekday trips into weekends and seek work-friendly amenities. Platforms and hotels are responding by enhancing search filters and merchandising for workspace, connectivity, and extended-stay features to better meet evolving traveler needs. Over the forecast period, leisure will continue to anchor booking volume, while bleisure growth increases the importance of flexible inventory and integrated itinerary planning tools.

Traveler behavior is shifting, with conversational AI enabling more personalized booking requests that blend leisure, work, and family considerations. Hotels are expanding extended-stay and branded residence offerings to accommodate longer stays without compromising service quality. The accommodation mix is evolving toward inventory that can flex by length of stay, sleeping capacity, workspace quality, and location, broadening appeal across both hotels and alternative accommodations. Loyalty programs and subscription-style benefits are becoming more important as platforms and suppliers aim to secure repeat bookings across multiple trip purposes. These trends collectively create a richer merchandising and packaging environment, supporting upselling opportunities while maintaining strong base conversion rates.

Geography Analysis

Germany held 11.90% share in 2025 and remains a cornerstone for regional demand as one of Europe’s largest source markets, serving as one of Europe’s largest source markets and supporting both inbound and intra-regional travel to neighboring destinations. France is projected as the fastest-growing country at a 7.43% CAGR through 2031, driven by post-Olympics infrastructure improvements, strong destination marketing, and capacity investments by leading hotel chains. Major destinations such as Spain and Italy continue to attract substantial tourism activity, reinforcing baseline demand across a wide range of accommodation types. City-level short-term rental regulations, including license restrictions in key urban areas, are reshaping booking patterns and directing demand toward compliant supply within these countries.

Northern European markets, including the Netherlands and Austria, are also adapting to tighter municipal restrictions, which can redirect short-term stays to nearby compliant locations. Central and Eastern Europe is showing steady growth, supported by improved air connectivity and infrastructure that enhance regional competitiveness. Meanwhile, Greece and Portugal continue to attract diversified demand as high-end resorts expand, strengthening the premium positioning of both new and established destinations. France’s ongoing momentum extends beyond Paris, benefiting summer and shoulder-season travel as capacity and connectivity upgrades boost accessibility to regional hubs. Germany’s strong outbound travel behavior further supports occupancy dynamics across neighboring markets, adding resilience to cross-border corridors.

Regulatory harmonization under EU frameworks is expected to reduce fragmentation for platforms and hosts by standardizing data-sharing and registration practices, enabling better planning for professional operators. However, local regulations and enforcement intensity will continue to influence short-term availability trends in major cities. Overall, the regional landscape balances scale and premium demand in Southern and Western Europe with value-driven growth and diversification in Central and Eastern Europe. This distribution supports steady expansion at the regional level while supply dynamics and regulatory frameworks shape local market outcomes throughout the forecast period.

Competitive Landscape

The European online accommodation market reflects moderate concentration, characterized by split competitive dynamics between dominant digital platforms and established hotel groups. Major OTAs such as Booking.com, Expedia, and Airbnb retain strong distribution power through network effects and AI-enabled personalization, though regulatory intervention has begun reshaping this dominance. The EU Digital Markets Act’s designation of Booking.com as a gatekeeper in May 2024 forced the removal of rate parity clauses and mandated greater data transparency. At the same time, large hotel chains including Marriott, Accor, and Hilton are regaining margin control by strengthening direct booking ecosystems and loyalty infrastructure. While Booking Holdings’ room-night growth slowed in late 2025 and Expedia pivoted toward B2B expansion, these shifts suggest a maturing Western European market alongside strategic repositioning rather than outright contraction.

Competitive strategy across the sector increasingly centers on AI-driven optimization, digital integration, and selective regulatory navigation. Airbnb expanded AI-based customer support and conversational search capabilities, while Booking.com advanced similar tools through generative AI integrations designed to process vast travel data inputs. Hotel operators are simultaneously enhancing direct channels through automated upgrades, mobile key technologies, and fulfillment-layer acquisitions to reduce reliance on OTAs. Accor’s targeted acquisitions and Hilton’s digital feature rollouts illustrate a broader push to internalize customer relationships and data ownership. Emerging AI-native providers are also enabling independent hotels to deploy advanced personalization tools, narrowing the historical technology gap between standalone properties and platform-scale operators.

Opportunities are emerging in regulatory technology, dynamic packaging, and alternative travel segments. New EU short-term rental regulations requiring standardized registration disclosures from May 2026 are increasing operational complexity for hosts and property managers, creating demand for automated compliance solutions. Growth in bleisure travel presents another underdeveloped segment, particularly in integrated coworking and connected-trip functionality that remains fragmented across incumbents. Blockchain-based rate verification systems also represent an untapped mechanism for transparent pricing compliance under evolving DMA rules. Fiscal scrutiny and tax settlements across the OTA landscape further reinforce the importance of structural resilience and regulatory alignment. Recent mergers, minority stake acquisitions, and technology investments indicate that capital allocation is increasingly directed toward proprietary systems, AI capabilities, and fulfillment infrastructure rather than pure geographic expansion.

Europe Online Accommodation Industry Leaders

Booking Holdings (Booking.com, Agoda)

Expedia Group (Expedia, Hotels.com, Vrbo)

Airbnb Inc.

HRS Group

eDreams ODIGEO (Opodo, GoVoyages)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2026: Airbnb completed the global rollout of “Reserve Now, Pay Later,” enabling USD 0 upfront for eligible stays after a successful U.S. pilot in August 2025 that achieved 70% adoption among eligible bookings, supporting higher booking momentum into early 2026.

- January 2026: Marriott announced outstanding global growth for 2025, adding over 700 properties and nearly 100,000 rooms, including record luxury signings in EMEA and a strengthened European pipeline into 2026.

- January 2026: Hilton launched Apartment Collection by Hilton to add up to 3,000 apartment-style units with bookings commencing in the first half of 2026, targeting extended-stay and bleisure demand segments across Europe and other regions.

- November 2025: The European Parliament and Council reached a final agreement on the Payment Services Regulation and PSD-3, enhancing fraud protection, clarifying liability for social engineering scams, and mandating verification controls such as IBAN and name matching with implementation steps targeting 2027.

- October 2025: Booking Holdings began migrating API-connected hosts to a single-service fee configuration to simplify economics and align with transparency requirements, a step it extended to most non-PMS hosts by December 2025.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe online accommodation market as the gross value of room and unit bookings that are reserved and paid for through digital channels located in Europe, including websites and mobile apps of online travel agencies, sharing-economy platforms, and branded hotel or rental sites. Revenue captures only lodging fees and service commissions that are directly tied to the act of booking.

We exclude ancillary services such as flights, car hire, on-property food, and any offline or walk-in transactions that never touch an online interface.

Segmentation Overview

- Segmentation by Accommodation Type

- Hotels

- Short-term & Vacation Rentals

- Hostels & Budget Stays

- Campgrounds & Holiday Parks

- Other Accommodation Types

- Segmentation by Booking Channel

- Online Travel Agencies (OTAs)

- Direct Supplier Websites & Apps

- Metasearch & Aggregators

- Sharing-Economy Platforms

- Corporate Travel Platforms

- Segmentation by Device Type

- Mobile

- Desktop / Laptop

- Tablet & Others

- Segmentation by Traveler Type

- Leisure

- Business

- Bleisure

- Group & MICE

- Segmentation by Country

- United Kingdom

- Germany

- France

- Spain

- Italy

- Netherlands

- Nordics

- Central & Eastern Europe

- Benelux

- Austria & Switzerland

- Portugal

- Greece

- Rest of Europe

Detailed Research Methodology and Data Validation

Desk Research

We begin by assembling evidence from high-quality public datasets such as Eurostat guest-night statistics, the European Commission hotel-distribution study, and digital economy scoreboards, which outline booking volumes, channel splits, and device adoption. Trade bodies like HOTREC, the European Travel Commission, and UNWTO supply occupancy and average daily rate trends that help shape pricing curves. Company filings, investor decks, tourism board dashboards, and respected press articles let us verify platform throughput and seasonality. Paid databases, for example, D&B Hoovers and Dow Jones Factiva, add company-level revenue signals. These sources are illustrative; many additional publications were consulted during data gathering and validation.

Primary Research

Mordor analysts hold structured conversations with revenue managers at chain and independent hotels, finance heads at leading OTAs, hosts of short-term rentals, and digital travel start-ups across the United Kingdom, Germany, Spain, Italy, and the Nordics. Insights on commission spreads, mobile share, and parity-clause impacts refine assumptions and bridge information gaps.

Market-Sizing & Forecasting

The model starts with a top-down reconstruction of paid guest nights using Eurostat records and then applies online penetration rates drawn from primary interviews to estimate booking volumes. Average booking value, informed by disclosed ADRs and nightly rental rates, converts volumes to revenue. Supplier roll-ups and sampled price-times-volume checks provide a bottom-up sense check that flags anomalies for adjustment. Key driver variables include smartphone share of bookings, cross-border travel recovery, OTA commission trajectories, short-term rental regulatory caps, and corporate travel rebound. A multivariate regression generates the five-year forecast, while scenario analysis tests sensitivity to macro shocks.

Data Validation & Update Cycle

Outputs pass variance checks against independent tourism receipts, currency effects, and platform gross-booking disclosures. Senior reviewers sign off after anomalies are resolved. Reports refresh every twelve months, with interim updates triggered by major regulatory or demand shifts. Just before delivery, an analyst performs a fresh pass so clients receive the latest view.

Why Mordor's Europe Online Accommodation Baseline Commands Reliability

Published estimates often differ because firms choose unequal scopes, convert currencies differently, and refresh at varied cadences.

Key gap drivers include whether ancillary travel spend is folded into accommodation, how aggressively mobile growth is projected, and the frequency of expert validation that tempers extrapolation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 85.54 B (2025) | Mordor Intelligence | |

| USD 89.13 B (2024) | Regional Consultancy A | Bundles package holidays and uses platform gross merchandise rather than lodging revenue only |

| USD 54.41 B (2024) | Trade Journal B | Relies on limited public filings, sparse primary checks, and a conservative online-penetration assumption |

This comparison shows that Mordor Intelligence offers a balanced, transparent baseline that traces every figure back to visible variables and repeatable steps, giving decision-makers numbers they can trust.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the Europe online accommodation market size and projected growth to 2031?

The Europe online accommodation market size is expected to grow from USD 78.54 billion in 2025 to USD 85.54 billion in 2026 and is forecast to reach USD 105.61 billion by 2031, reflecting a 4.13% CAGR through the forecast period.

Which accommodation types are growing fastest in Europe through 2031?

Short-term and vacation rentals are the fastest-growing accommodation type, with a projected 6.81% CAGR through 2031 as platforms and professional managers expand compliant supply and services.

How are EU regulations affecting European online accommodation distribution in 2026?

The DMA’s gatekeeper obligations for Booking.com and payments reforms under PSR and PSD-3 are reshaping ranking transparency, parity practices, and checkout authentication, which support more balanced direct and OTA booking flows in 2026.

What devices dominate booking behavior in the Europe online accommodation market?

Mobile leads with a 54.7% share in 2025 and is advancing at an 8.11% CAGR as platforms embed conversational AI, simplify consent, and expand flexible payments that increase in-app conversion.

Which countries are positioned for the strongest growth in European online accommodation?

France is forecast to be the fastest-growing through 2031 at a 7.43% CAGR, while Germany remains a core demand anchor with 11.90% share in 2025 amid robust intra-European travel foundations.

How are leading companies competing in the Europe online accommodation market in 2026?

Booking Holdings scales AI-enabled search and connected trips, Airbnb extends mobile-led features and flexible payments, Expedia grows B2B partnerships, and hotel chains such as Marriott, Accor, and Hilton invest in premium supply and direct channel capabilities.