Europe Mortgage/Loan Broker Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

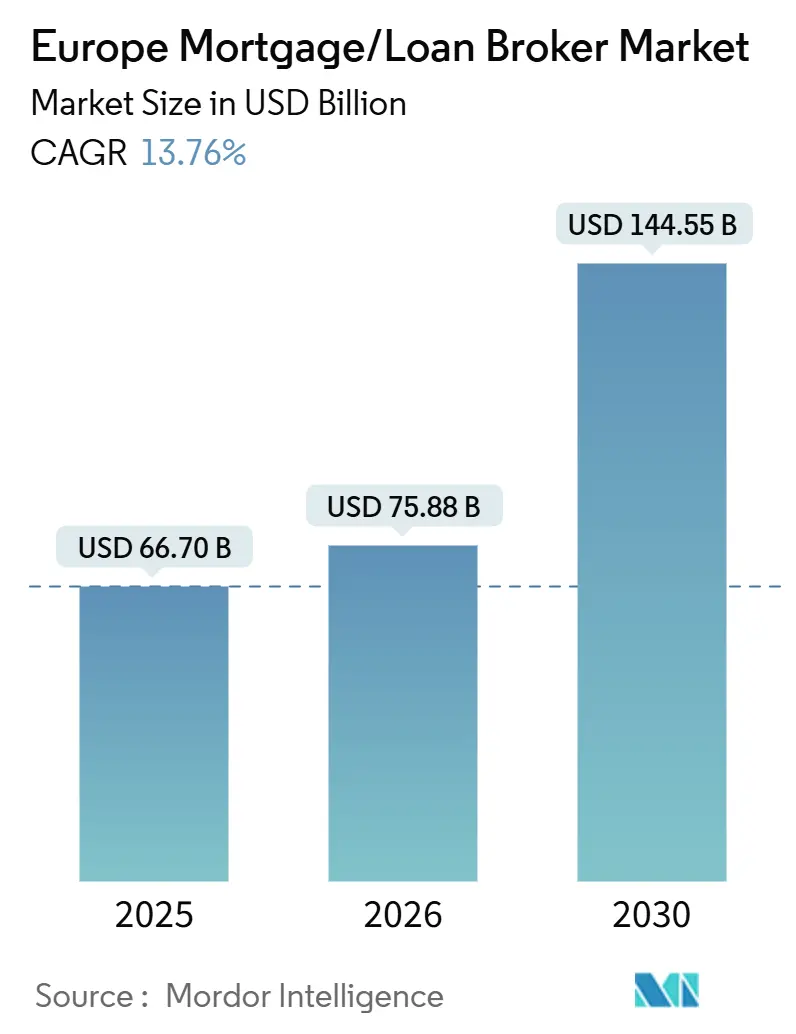

| Base Year Market Size (2025) | USD 66.70 Billion |

| Market Size (2026) | USD 75.88 Billion |

| Market Size (2031) | USD 144.55 Billion |

| Growth Rate (2026 - 2030) | 13.76% CAGR |

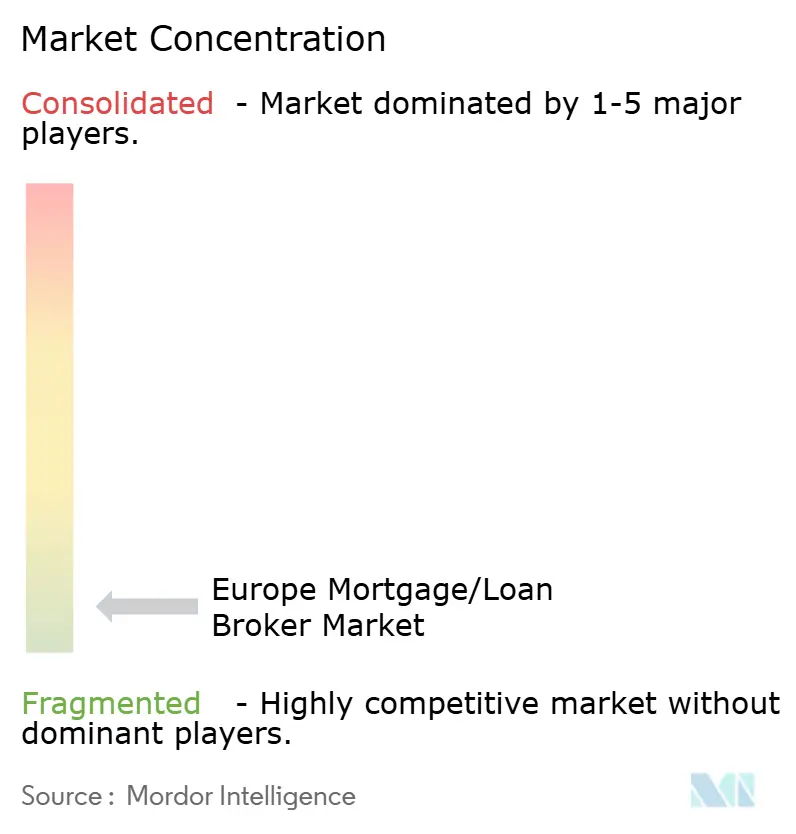

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Mortgage/Loan Broker Market Analysis by Mordor Intelligence

The Europe Mortgage/Loan Broker Market size is projected to expand from USD 66.70 billion in 2025 and USD 75.88 billion in 2026 to USD 144.55 billion by 2031, registering a CAGR of 13.76% between 2026 to 2031.

Recovery in mortgage activity is tracking the easing of Europe’s rate shock as policy rates move lower, which is helping demand for advice-led origination to firm after a two-year contraction. The shift toward intermediated distribution is reinforced by banks seeking scalable, lower-cost origination while they maintain credit risk on balance sheets, an operating pattern that favors broker platforms with strong lender panels and digital onboarding capabilities. Energy performance regulation and the growth of green mortgage products are creating new advisory needs, which expand the role of brokers in structuring renovation-linked finance and in navigating eligibility and documentation. Momentum in digital identity and qualified e-signatures is set to compress application cycle times across member states, which supports higher conversion in broker pipelines as identity proof and signing become standardized.

Key Report Takeaways

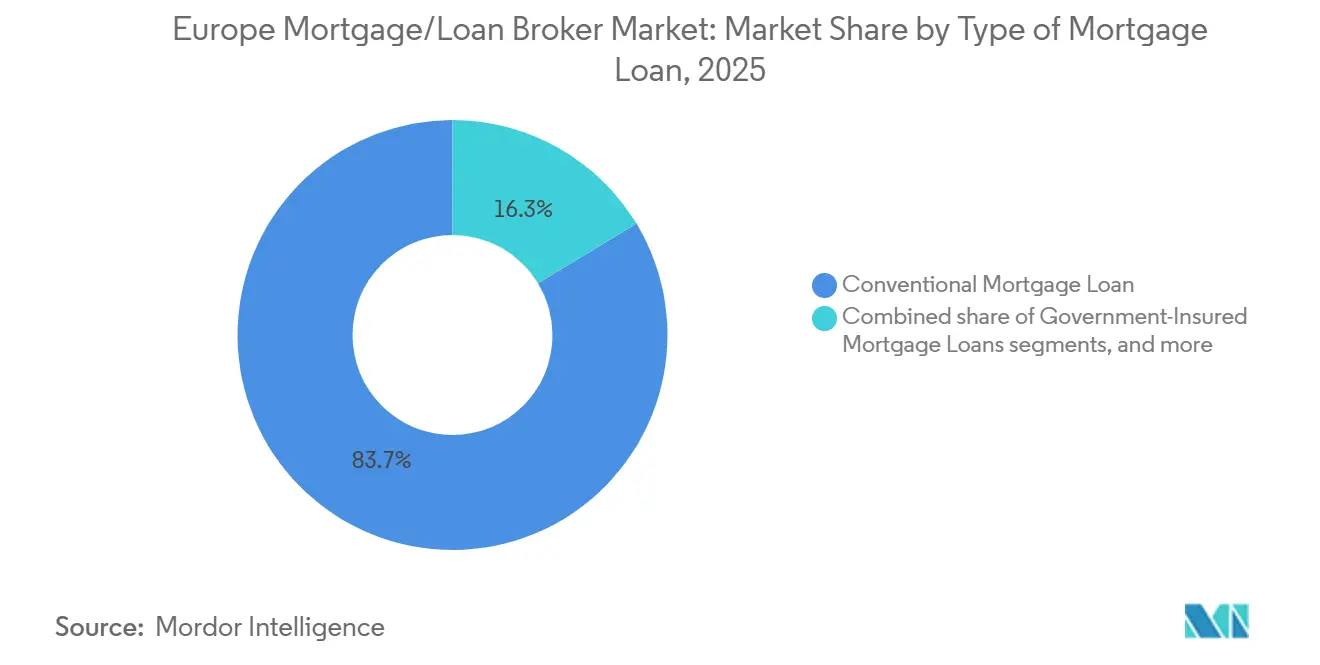

- By type of mortgage loan, conventional products led with an 83.67% revenue share of the Europe mortgage loan brokers market in 2025, while government-insured loans are projected to expand at a 9.00% CAGR through 2031.

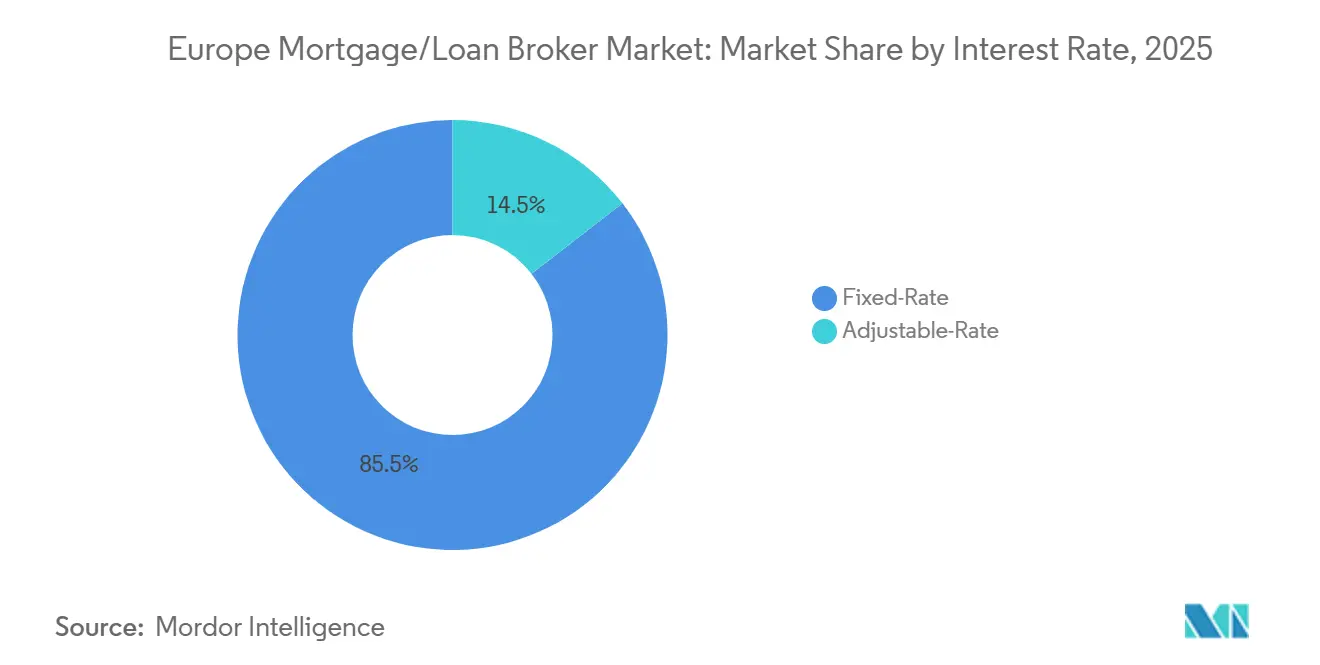

- By interest rate, fixed-rate mortgages commanded an 85.50% share of the Europe mortgage loan brokers market 2025 volumes, while adjustable-rate products are projected to grow at a 6.00% CAGR through 2031.

- By provider, primary mortgage lenders retained an 84.00% share of the Europe mortgage loan brokers market in 2025, while secondary lenders are projected to grow at an 8.00% CAGR through 2031.

- By geography, the United Kingdom held a 35.00% share of the Europe mortgage loan brokers market in 2025, while the Netherlands is projected to be the fastest-growing country at a 7.00% CAGR through 2031.

- By mortgage loan terms, 30-year products accounted for a 52.33% share of the Europe mortgage loan brokers market in 2025, while the other mortgage loan terms segment is projected to grow at a 7.00% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Mortgage/Loan Broker Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advice-led origination share rising | +1.8% | EU27, UK, EEA-wide, with the strongest uptake in the Netherlands, UK, Germany | Medium term (2-4 years) |

| Regulatory push for suitability and fair value | +1.5% | UK and EU, with Consumer Duty and MCD review | Long term (≥ 4 years) |

| Green and energy-efficient mortgages and EPBD renovation finance | +2.1% | EU27 with early gains in Germany, France, Netherlands | Long term (≥ 4 years) |

| Bank-led lending model leveraging broker distribution | +1.2% | National markets with early gains in Italy, Spain, Poland | Short term (≤ 2 years) |

| Digital identity and e-signature enablement | +0.9% | EU27 with eIDAS 2.0 rollout by November 2026 | Medium term (2-4 years) |

| Open banking and broader data access streamlining affordability | +0.3% | EU27 and UK open finance programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Advice-led Origination Share Rising (Europe-specific, 2026+)

Broker intermediation continues to entrench as the default path for many borrowers, driven by the need to navigate complex affordability rules, product eligibility, and documentation across lenders as markets emerge from the rate shock. The Europe mortgage loan brokers market benefits as borrowers prefer advice on fixed versus variable choices, early repayment options, and green-linked incentives that now require standardized disclosures under EU law [1]European Commission, “Commission Correspondence and Documents,” EUR-Lex, eur-lex.europa.eu . In the United Kingdom, large networks have scaled adviser capacity and client monitoring capabilities, which have supported higher productivity and revenue growth in 2025 and set up for elevated refinancing activity in 2026 as fixed-rate cohorts mature. In Germany, distribution platforms and national broker brands have expanded their technology stacks to speed pre-approvals and standardize lender connections, which complements banks that prefer to retain credit risk while outsourcing acquisition. In France and the Netherlands, stabilization in volumes and policy support for first-time buyers keep advice-led channels relevant as lenders seek throughput and borrowers seek certainty after recent volatility. Across major markets, this structural shift is anchored in cost and risk management needs at lenders and in the borrower’s preference for impartial product navigation, which together reinforce the Europe mortgage loan brokers market as a core origination route through 2031.

Regulatory Push for Suitability and Fair Value (EU/UK)

The UK Financial Conduct Authority’s Consumer Duty, with full rules extending to closed products in 2024, sets outcomes-based expectations for good faith, avoidance of foreseeable harm, and support for financial objectives across the mortgage lifecycle, which raises the bar on advice quality and client communications for intermediaries [2]Financial Conduct Authority, “Implementing the Consumer Duty in Mortgage Intermediaries,” Financial Conduct Authority, fca.org.uk . Enhanced oversight of appointed representatives requires principal firms to maintain robust risk management and monitoring for networks, which favors scaled brokers that can spread compliance costs and invest in systems. In the European Union, the Mortgage Credit Directive review process highlights integration of energy performance data and sustainability features in disclosures, which nudges broker advice toward standardized green product suitability and clear risk-factor explanations. The European Banking Authority’s focus on consumer trends and product fairness further codifies expectations around transparency and creditworthiness, which supports a structured advisory environment for the Europe mortgage loan brokers market. Over the forecast horizon, these regulatory dynamics are expected to raise compliance intensity while simultaneously validating the role of professional intermediation for complex cases.

Green/Energy-Efficient Mortgages and EPBD-Driven Renovation Finance

The recast Energy Performance of Buildings Directive aligns national targets for residential energy performance and makes renovation-linked lending a strategic focus area, which increases demand for brokers adept at packaging green terms with standard mortgages. The European Investment Bank and Deutsche Bank launched a program in 2024 in Germany that passes a 0.2 percentage point interest advantage for energy-efficient modernization and uses a mezzanine-guaranteed securitization to free up lending capacity, which sets a template for public-private scaling of climate-linked mortgages. Banks and brokers will increasingly need to verify and document energy improvements and eligibility, which creates new points of advice and new documentation flows that fit well with broker-led origination. The Europe mortgage loan brokers market stands to benefit as standardized green documentation, national subsidies, and portfolio standards move from pilots to mandatory frameworks, which enlarges the addressable base for renovation finance through 2031. As consumer awareness of energy cost savings rises with clear eligibility criteria, demand is likely to tilt toward products that embed incentives for verified upgrades, which further elevates the value of specialized intermediary advice.

Bank-led Lending Model Leveraging Broker Distribution

Across major EU markets, banks are leaning on brokers to scale acquisition at lower unit cost while preserving balance sheet control of credit, which aligns with risk appetite and capital planning in a moderate growth environment. In Italy and Spain, lenders have used intermediated channels to push green-linked and niche products without replicating specialized advisory teams in-house, which reflects a pragmatic approach to product breadth and origination speed. The United Kingdom shows how specialization through broker networks can unlock segments like later-life lending and new-build purchases, supported by targeted acquisitions and adviser productivity gains reported in 2025[3]London Stock Exchange, “Mortgage Advice Bureau Trading Update,” London Stock Exchange, londonstockexchange.com. The Europe mortgage loan brokers market benefits as banks emphasize throughput and customer experience, often through white-label or platform partnerships that integrate broker processes into lender workflows. Over the near term, this model helps banks pursue volume targets while brokers widen lender panels and product choice, which together support higher conversion and better borrower matching.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Affordability squeeze and transaction slowdown (rate shock hangover) | -0.9% | EU-wide, acute in France, Portugal, Sweden | Short term (≤ 2 years) |

| Compliance burden from Consumer Duty and AR oversight (UK/EU) | -0.6% | UK and EU | Medium term (2-4 years) |

| Cross-border licensing constraints under CRD VI | -0.3% | EU-wide, affects third-country institutions and cross-border models | Long term (≥ 4 years) |

| Cross-country product heterogeneity and macroprudential caps | -0.4% | EU27 with member-state LTV and DSTI caps | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Affordability Squeeze and Transaction Slowdown (Rate Shock Hangover)

Higher borrowing costs since 2022 reduced affordability and housing transactions across the euro area, and the lagged repricing of existing loans continues to weigh on household budgets even as policy rates start to ease in 2026. A large share of euro-area mortgages remains sensitive to rate movements, and cohorts that originated at very low fixed rates during 2020–2021 are scheduled to reset at higher rates over the next few years, which creates budgeting stress for many households. Lower-income borrowers have higher exposure to adjustable-rate products and are therefore more affected by changes in interest rates, which depresses purchase intent and extends sales cycles for brokers serving first-time buyers. Household consumption shifted under the pressure of higher mortgage payments in 2024 and 2025, which dampened demand for home buying and slowed the pace of property-related spending. This environment requires brokers to manage longer lead times and to differentiate approaches between refinancing clients and stretched first-time purchasers, with advice on product structure and stress testing playing a central role.

Compliance Burden from Consumer Duty and AR Oversight (UK/EU)

The UK Consumer Duty imposes outcomes-focused standards for product design, fair value, consumer understanding, and support, which has increased the cost and complexity of compliance for intermediaries that supervise appointed representatives. Principal firms need to maintain stronger oversight and reporting on their networks, which requires investments in systems, data, and staff to ensure continuous adherence to the Duty’s expectations. In parallel, EU mortgage credit rules standardize key elements of disclosure and creditworthiness, while leaving national caps on loan-to-value and debt-service-to-income, which creates complexity for cross-border brokers that must tailor advice and compliance processes to each jurisdiction. The Europe mortgage loan brokers market must therefore balance growth with elevated governance requirements, especially for networks that operate across markets with different supervisory traditions and caps. Over the medium term, compliance intensity is likely to contribute to consolidation as firms seek scale efficiencies in governance, training, and quality assurance.

Segment Analysis

By Type of Mortgage Loan: Conventional Products Anchor, But Sovereign-Backed Schemes Accelerate

Conventional mortgage loans accounted for an 83.67% share in 2025, reflecting their status as the core offering across major European geographies for borrowers with stable credit and deposit buffers, and this proportion underscores how lenders and brokers continue to place standard home purchase and refinance products at the center of origination. The Europe mortgage loan brokers market share for conventional loans is supported by broad lender panels and consistent underwriting rules, which simplify comparison and speed for borrowers seeking predictable terms. Country-level macroprudential settings, including loan-to-value and debt-service-to-income caps, shape the loan mix that brokers can arrange and influence how much borrowers must contribute toward deposits, which in turn guides advice around product type and tenor. Jumbo loans remain a niche for complex borrower profiles and are distributed through a combination of private banks and specialist lenders, where brokers add value by coordinating documentation and negotiating bespoke terms across multiple counterparties. In this environment, technology-enabled brokers aggregate lender responses faster and present structured options to clients, which helps maintain the centrality of conventional products even as policy and green incentives broaden choices.

Government-insured mortgages are projected to grow at a 9.00% CAGR over 2026–2031 as national schemes in several member states support first-time buyers and energy upgrades, which expand eligibility for clients with thinner deposits or non-standard income. The Europe mortgage loan brokers market benefits from these programs because intermediaries are well placed to help borrowers navigate eligibility criteria, assemble required documents, and coordinate with lenders that participate in subsidy or guarantee frameworks. As more banks introduce green mortgage variants that reward verified energy performance improvements, brokers are adding renovation-linked loan options to their panels, which often pair state-backed guarantees with rate incentives. Over the forecast period, this mix is likely to diversify the Europe mortgage loan brokers industry product set while keeping conventional loans the volume anchor in most markets.

Note: Segment shares of all individual segments available upon report purchase

By Mortgage Loan Terms: 30-Year Dominance Persists, Yet Ultra-Long Tenors Emerge

Thirty-year mortgages held a 52.33% share in 2025, a reflection of borrower preference for lower monthly payments and lender comfort with amortization that aligns with retirement planning horizons in many EU markets. The Europe mortgage loan brokers market size for longer tenors remains supported by affordability considerations and by the need to offset higher nominal rates with extended terms, which many lenders have accommodated under local macroprudential limits. In France, company data show best-profile mortgage rates near 2.81% for 15 years and 2.92% for 20 years as of mid-2025, which demonstrates how term selection and pricing interact as rates normalize from their 2023 peaks [4]Capifrance, “French Real Estate Mortgage Rates in August 2025,” Capifrance, capifrance.fr . Markets with amortization requirements that increase required repayments at higher loan-to-value or debt-to-income levels also shape the real effective term for borrowers, which brokers must factor into suitability advice. Taken together, tenor selection has become a central part of the advice process, with brokers helping clients balance payment stability, total interest cost, and future refinancing options.

At the same time, very long terms in the 35–40-year range are gaining interest as affordability constraints persist for younger buyers and as lenders innovate within regulatory boundaries, which raises the need for clear advice on long-run costs and refinancing checkpoints. The Europe mortgage loan brokers market benefits when advisers can present comparable total cost projections and stress scenarios across 15, 20, 30, and longer terms, which supports informed decisions amid evolving rate expectations. Over 2026–2031, this segment is expected to grow as rules permit and as green-linked incentives are integrated into longer amortization plans, which can align energy savings with loan servicing capacity for certain borrowers.

By Interest Rate: Fixed Products Reign Post-Volatility, But Variable Revival Looms

Fixed-rate mortgages commanded an 85.50% share in 2025, reflecting a strong borrower preference for payment certainty after recent volatility and the widespread availability of fixed terms across lenders and geographies. In Spain, company-reported data show a marked upswing in fixed-rate selection during 2025, accompanied by a reduction in average fixed rates by March, which illustrates how rate normalization steered choices throughout the year. In Germany, the stabilization of longer fixed terms supported brokered volumes in 2025 as large platforms and lender partnerships emphasized speed and certainty in approvals, particularly for 10-year fixes. The Europe mortgage loan brokers market size for fixed-rate placements accounted for a large part of 2025 activity as consumers prioritized budgeting stability while expecting further policy easing ahead. This pattern is aligned with supervisory emphasis on affordability stress testing, which brokers apply to guide clients toward structures that can withstand near-term and medium-term shocks.

Adjustable-rate mortgages are projected to grow at a 6.00% CAGR during 2026–2031 as spreads to fixed terms narrow and as borrowers with higher risk tolerance seek to benefit from potential future cuts, a dynamic that brokers will manage through careful suitability analysis. In Sweden, variable rates held a dominant share of new lending in early 2025 according to industry data, which highlights how national preferences and rate structures drive different product mixes that brokers must navigate. Research also shows higher default risk for variable-rate mortgages originated at very low rates that then reset materially higher, which makes the broker’s role in stress testing and term selection even more important through the cycle. The Europe mortgage loan brokers market size for adjustable-rate placements is projected to expand at 6.00% CAGR from 2026 to 2031 as rate normalization continues and as consumers weigh short-term costs against long-term flexibility.

Note: Segment shares of all individual segments available upon report purchase

By Provider: Banks Dominate Direct Issuance, Yet Specialist Lenders Gain Share in Niches

Primary mortgage lenders, principally banks that originate to their own balance sheets, retained an 84.00% share in 2025 as the banking sector remains central to mortgage funding in Europe and continues to work through broker panels to scale distribution efficiently. Many lenders find value in outsourcing origination while retaining underwriting standards and credit risk, which allows them to focus on balance sheet optimization while brokers handle acquisition and client preparation. Platform integrations between lenders and broker networks have expanded, with identity and e-signature standardization expected to reduce duplication of steps and improve straight-through processing in the coming years. The Europe mortgage loan brokers market share for bank-originated loans reflects this division of labor, where lenders seek throughput and brokers manage multi-lender comparisons, documentation, and client support.

Secondary mortgage lenders, including non-bank mortgage credit institutions and investment-backed originators, are projected to grow at an 8.00% CAGR through 2031 by serving non-standard borrower profiles and by competing in refinancing and switching segments that some banks prioritize less during volume recovery. These players often partner with brokers to target niches based on employment type, residency, or collateral condition, which requires tailored underwriting but can deliver competitive terms when balance sheet capacity is available. As open finance and identity frameworks reduce friction in onboarding, secondary lenders can integrate with broker systems more deeply, which supports scale without large branch footprints. Over 2026–2031, this mix is expected to remain dynamic as banks and non-banks adjust to demand, regulation, and funding conditions, all of which sustain the centrality of broker distribution.

Geography Analysis

The United Kingdom held a 35.00% share of the Europe mortgage loan brokers market in 2025, reflecting a deeply embedded intermediation culture and the scale of national networks that reported revenue growth and adviser expansion in 2025. UK Finance projects a rise in gross lending in 2026, supported by a refinancing wave as fixed-rate cohorts mature, which underscores the importance of broker monitoring and retention programs. The Europe mortgage loan brokers market size attributed to the United Kingdom reflects stable penetration and the ability of large networks to operate specialist units that serve later-life borrowers and new-build segments, which helps sustain throughput even when transaction counts fluctuate. Over the forecast period, growth in the UK is likely to be below the overall market rate due to maturity, although segment-led expansion should provide steady opportunities for intermediation.

Germany anchors the continental broker landscape through national platforms and strong bank partnerships, where fixed-rate stabilization in 2025 aided approvals and workflow improvements that cut decision times for qualified borrowers. Green-linked programs supported by public banks and EU institutions have created additional demand in renovation finance, which is often brokered alongside standard mortgages to ensure documentation and eligibility are correctly framed at application. France remains a large market with strong competition among mutualist banks and active broker networks, where company data points to mid-2025 rates near 2.92% for 20-year terms for top profiles, which illustrates the recovery in affordability since early 2024. In these core markets, brokers differentiate on speed, lender breadth, and advisory scope, factors that will continue to determine share within the Europe mortgage loan brokers market.

The Netherlands is projected to be the fastest-growing country at a 7.00% CAGR through 2031, supported by policy frameworks that reduce entry barriers for first-time buyers and by high broker usage in a complex mortgage environment. Company initiatives show Dutch brokers investing in client-facing applications that streamline status updates and action prompts, which can improve transparency and completion rates for borrowers navigating multiple steps. Italy and Spain have seen expanding digital distribution through comparison sites and broker platforms, while Spanish company-reported data reflect increased fixed-rate adoption as 2025 progressed and as pricing moved lower from 2024 levels. Nordic markets continue to exhibit high variable-rate usage, which brokers manage through stress testing and product selection in line with supervisory expectations. Across these geographies, broker penetration correlates with product complexity and the breadth of lender choice, both of which sustain the Europe mortgage loan brokers market through the forecast horizon.

Competitive Landscape

The Europe mortgage loan brokers market is fragmented at a pan-European level due to language, regulation, and bank partnership structures, with national champions and large networks competing alongside digital-first platforms that emphasize speed and monitoring. In the UK, one large network reported 2025 revenue of GBP 318 million with adviser growth to 2,135, and outlined acquisition-driven specialization in areas like later-life lending and new-build segments, which demonstrates the role of scale in compliance and productivity. Continental markets show similar patterns where technology investments streamline underwriting and client engagement, and where platform partnerships with banks emphasize throughput while maintaining risk standards. Over time, identity wallets and broader data access are expected to compress onboarding times and improve straight-through processing, which advantages firms that can invest in integrations and client monitoring systems.

Strategic moves since 2024 include acquisitions that deepen specialisms, CRM-enhancing technology integrations, and green mortgage capabilities tied to renovation finance, with several firms disclosing plans to scale segments where advice intensity is higher and lender appetite is strong. Company initiatives in the Netherlands show investment in consumer apps that clarify the mortgage journey through dashboards and prompts, which helps maintain customer engagement from application to completion. In Spain, broker-led platforms reported higher fixed-rate selection as pricing improved, underscoring how real-time rate monitoring within adviser tooling can influence product choice on client calls and digital flows. In Italy, long-standing comparison services continue to widen product access, which supports competitive tension among lenders that collaborate with brokers for distribution.

Regulatory compliance is a competitive variable as the UK Consumer Duty and EU disclosure standards require robust monitoring and clear communications throughout the advice process, which favors larger networks with systems that can scale quality assurance. The Europe mortgage loan brokers market is therefore likely to see continued consolidation among smaller firms that seek cost-sharing within networks, while larger players pursue selective acquisitions and partnerships to enhance segment reach. At the same time, public-private initiatives in green finance and continued innovation in identity and data access create scope for digital leaders to differentiate, provided they can align with evolving supervisory expectations around suitability, fairness, and transparency.

Europe Mortgage/Loan Broker Industry Leaders

Interhyp AG

London & Country Mortgages

Mortgage Advice Bureau

Dr. Klein

Connells Group – Countrywide Mortgage Services (UK)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Mortgage Advice Bureau announced FY2025 revenue of GBP 318 million with adviser growth to 2,135, reported adjusted profit before tax of GBP 35.8 million, and outlined multiple acquisitions and investments supporting specialization and expansion.

- October 2025: Mortgage Advice Bureau made a majority investment in UK Moneyman, integrating it as an appointed representative to support growth in specialist areas, including later-life lending.

- May 2024: The European Investment Bank and Deutsche Bank launched a discounted mortgage program in Germany for climate-friendly housing and energy-efficient modernization with a 0.2 percentage point rate advantage and a mezzanine-guaranteed securitization structure.

- May 2024: Deutsche Bank detailed program mechanics for the climate-friendly housing initiative, including eligibility based on primary energy demand reduction and distribution through Deutsche Bank, DSL Bank, and BHW Bausparkasse.

Europe Mortgage/Loan Broker Market Report Scope

A mortgage broker acts as a middleman for people or businesses and manages the mortgage loan application process. In essence, they set up relationships between mortgage lenders and borrowers without making any financial commitments of their own.

The Europe Mortgage/Loans Broker Market is segmented by enterprise, application, end-user, and geography. By enterprise, the market is sub-segmented into large, small, and medium-sized by application, the market is sub-segmented into home loans, commercial and industrial loans, vehicle loans, loans to governments, and others. By end-user, the market is sub-segmented into businesses and individuals. By geography, the market is sub-segmented into the United Kingdom, Germany, France, and the Rest of Europe.

The report offers market size and forecasts for the Europe Mortgage and Loan Broker Market in terms of dollar value (USD) for all the above segments.

| Conventional Mortgage Loan |

| Jumbo Loans |

| Government-Insured Mortgage Loans |

| Other Types of Mortgage Loan |

| 30-Year Mortgage |

| 20-Year Mortgage |

| 15-Year Mortgage |

| Other Mortgage Loan Terms |

| Fixed-Rate |

| Adjustable-Rate |

| Primary Mortgage Lender |

| Secondary Mortgage Lender |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Denmark |

| Rest of Europe |

| By Type of Mortgage Loan | Conventional Mortgage Loan |

| Jumbo Loans | |

| Government-Insured Mortgage Loans | |

| Other Types of Mortgage Loan | |

| By Mortgage Loan Terms | 30-Year Mortgage |

| 20-Year Mortgage | |

| 15-Year Mortgage | |

| Other Mortgage Loan Terms | |

| By Interest Rate | Fixed-Rate |

| Adjustable-Rate | |

| By Provider | Primary Mortgage Lender |

| Secondary Mortgage Lender | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Denmark | |

| Rest of Europe |

Key Questions Answered in the Report

What is the Europe mortgage loan brokers market growth outlook to 2031?

The Europe mortgage loan brokers market size is projected to reach USD 8.07 billion by 2031, reflecting a 7.76% CAGR from 2026 to 2031 as demand recovers with lower policy rates and advice-led origination expands.

Which product types are leading and which are growing fastest in Europe?

Conventional mortgages led with an 83.67% share in 2025 while government-insured products are projected to grow at a 9.00% CAGR through 2031 as sovereign programs support first-time buyers and green-linked upgrades.

Are fixed or variable mortgages preferred in the region now?

Fixed-rate products dominated at 85.50% of 2025 volumes as borrowers prioritized payment certainty, while adjustable-rate mortgages are projected to grow at 6.00% CAGR through 2031 as spreads narrow.

Which providers are gaining share in brokered originations?

Primary bank lenders retained an 84.00% share in 2025, while secondary lenders are projected to expand at 8.00% CAGR by focusing on non-standard profiles and refinancing niches through broker channels.

Which European markets are most important for broker distribution?

The United Kingdom led with a 35.00% share in 2025 due to deep broker penetration, while the Netherlands is projected to be the fastest-growing at a 7.00% CAGR through 2031 under supportive policies and high broker usage.

How will green regulation and digital identity change broker operations by 2031?

The EPBD recast and public-private green programs are increasing renovation-linked lending needs, while eIDAS 2.0 identity wallets and qualified e-signatures are expected to compress onboarding times and support higher completion rates in broker channels.